UPS 2006 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2006 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

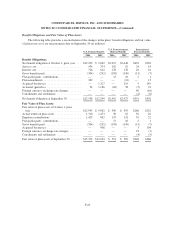

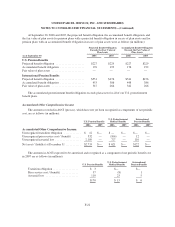

|

|

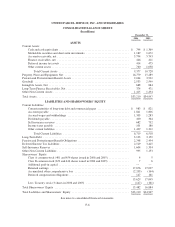

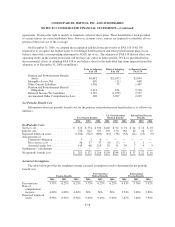

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

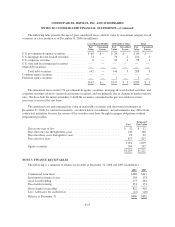

Derivative Instruments

Derivative instruments are accounted for in accordance with FASB Statement No. 133, “Accounting for

Derivative Instruments and Hedging Activities” (“FAS 133”), as amended, which requires all financial derivative

instruments to be recorded on our balance sheet at fair value. Derivatives not designated as hedges must be

adjusted to fair value through income. If a derivative is designated as a hedge, depending on the nature of the

hedge, changes in its fair value that are considered to be effective, as defined, either offset the change in fair

value of the hedged assets, liabilities, or firm commitments through income, or are recorded in OCI until the

hedged item is recorded in income. Any portion of a change in a derivative’s fair value that is considered to be

ineffective, or is excluded from the measurement of effectiveness, is recorded immediately in income.

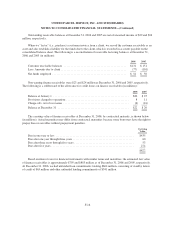

New Accounting Pronouncements

In September 2006, the FASB issued Statement No. 158 “Employers’ Accounting for Defined Benefit

Pension and Other Postretirement Plans (an amendment of FASB Statements No. 87, 88, 106, and 132(R))”

(“FAS 158”). This statement requires the recognition of the funded status of defined benefit pension and other

postretirement plans as an asset or liability in the balance sheet for fiscal years ending after December 15, 2006.

FAS 158 also requires delayed recognition terms, consisting of actuarial gains and losses and prior service costs

and credits, to be recognized in other comprehensive income and subsequently amortized to the income

statement. On December 31, 2006, we adopted the recognition and disclosure provisions of FAS 158. The effect

of adopting FAS 158 on our balance sheet as of December 31, 2006 has been included in Note 5 to the

consolidated financial statements, while there was no effect on our balance sheet for prior periods.

Additionally, we currently utilize the early measurement date option available under Statement No. 87

“Employers’ Accounting for Pensions”, and we measure the funded status of our plans as of September 30 each

year. Under the provisions of FAS 158, we will be required to use a December 31 measurement date for all of our

pension and postretirement benefit plans no later than 2008. We do not expect the impact of the change in

measurement date to have a material impact on our financial statements.

In June 2006, the FASB issued Interpretation No. 48 “Accounting for Uncertainty in Income Taxes (an

interpretation of FASB Statement No. 109)”. This interpretation was issued to clarify the accounting for

uncertainty in income taxes recognized in the financial statements by prescribing a recognition threshold and

measurement attribute for tax positions taken or expected to be taken in a tax return. The interpretation also

provides guidance on derecognition, financial statement classification, tax-related interest and penalties, and

additional disclosure requirements. We are required to adopt this interpretation effective January 1, 2007. We are

currently in the process of evaluating the impact of this standard on our financial statements. Any necessary

transition adjustments will not affect net income in the period of adoption and will be reported as a change in

accounting principle in our consolidated financial statements.

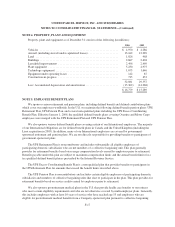

In September 2006, the FASB issued Statement No. 157 “Fair Value Measurements” (“FAS 157”), which is

effective for fiscal years beginning after November 15, 2007. FAS 157 was issued to define fair value, establish a

framework for measuring fair value, and expand disclosures about fair value measurements. FAS 157 is not

anticipated to have a material impact on our results of operations or financial condition.

The adoption of the following recent accounting pronouncements did not have a material impact on our

results of operations or financial condition:

• FSP AUG AIR-1 “Accounting for Planned Major Maintenance Activities”;

• FAS 156 “Accounting for Servicing of Financial Assets”; and

• FSP FAS 13-2 “Accounting for a Change in the Timing of Cash Flows Related to Income Taxes

Generated by a Leveraged Lease Transaction”.

Changes in Presentation

Certain prior year amounts have been reclassified to conform to the current year presentation.

F-13