Tyson Foods 2005 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2005 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

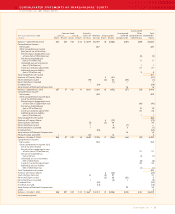

>> MANAGEMENT’S DISCUSSION AND ANALYSIS (CONTINUED)

TYSON FOODS, INC. 2005 ANNUAL REPORT

>>>>>>>>>>>>>>>>

>>>>>>>>>>>>>>>>

Tyson Foods, Inc. >> 27

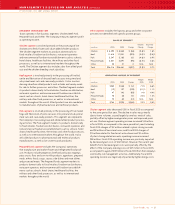

between 3% and 9% of qualifying domestic production income

over that period. Additionally, on December 21, 2004, the FASB

issued FASB Staff Position 109-1, “Application of FASB Statement

No. 109, Accounting for Income Taxes (SFAS No. 109), to the Tax

Deduction on Qualified Production Activities Provided by the

American Jobs Creation Act of 2004” (FSP 109-1). FSP 109-1, which

was effective upon issuance, states the deduction under this

provision of the AJC Act should be accounted for as a special

deduction in accordance with SFAS No. 109. The Company has

not yet quantified the impact that will be realized from these

provisions of the AJC Act.

The AJC Act also allows for an 85% dividends received deduction

on the repatriation of certain earnings of foreign subsidiaries. On

December 21, 2004, the FASB issued FASB Staff Position 109-2,

“Accounting and Disclosure Guidance for the Foreign Earnings

Repatriation Provision within the American Jobs Creation Act

of 2004” (FSP 109-2). FSP 109-2, which was effective upon issuance,

allows companies time beyond the financial reporting period of

enactment to evaluate the effect of the AJC Act on its plan for

reinvestment or repatriation of foreign earnings for purposes of

applying SFAS No. 109. Additionally, FSP 109-2 provides guidance

regarding the required disclosures surrounding a company’s

reinvestment or repatriation of foreign earnings. Additionally,

the Internal Revenue Service issued three notices relating to the

repatriation, which clarify the provisions of the Act. The latest in

the series of notices was IRS Notice 2005-64, which was issued

during the fourth quarter of fiscal 2005. During fiscal 2005, the

Company repatriated foreign earnings using the provision of

the act as discussed in Note 17, “Income Taxes” of the Notes

to Consolidated Financial Statements.

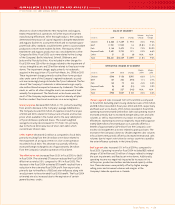

In December 2003, the Medicare Prescription Drug, Improvement

and Modernization Act of 2003 (the Act) was signed. The Act

allows a possible subsidy to retirement health plan sponsors to

help offset the costs of participant prescription drug benefits. In

March 2004, the FASB issued Staff Position No. 106-2, “Accounting

and Disclosure Requirements Related to the Act” (the Position). The

Position was effective for interim or annual periods beginning after

June 15, 2004. The Position allowed plan sponsors to recognize or

defer recognizing the effects of the Act in its financial statements

until specific accounting guidance for this federal subsidy was issued.

In the fourth quarter of fiscal 2005, the Company concluded the

prescription drug benefits included in its postretirement medical

plan is actuarially equivalent to Medicare Part D under the Act. In

accordance with FASB Staff Position 106-2, the Company decreased

its accumulated postretirement obligation and recognized an actu-

arial gain of approximately $55 million related to the present value

of all future subsidies expected to be received. This gain was more

than offset by actuarial losses primarily related to increased claims

costs, resulting in a net actuarial loss of approximately $9 million

from the Company’s postretirement health plan. It is the Company’s

policy to fully recognize experience gains and losses of its post-

retirement plans in the year in which they occur. There was no

effect on service or interest cost in the current period.

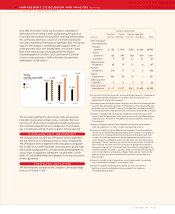

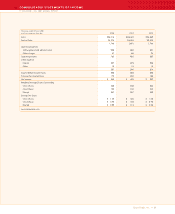

CRITICAL ACCOUNTING ESTIMATES

The preparation of consolidated financial statements requires

management to make estimates and assumptions. These estimates

and assumptions affect the reported amounts of assets and liabili-

ties and disclosure of contingent assets and liabilities at the date of

the consolidated financial statements and the reported amounts

of revenues and expenses during the reporting period. Actual results

could differ from those estimates. The following is a summary of

certain accounting estimates considered critical by the Company.

Financial instruments: The Company is a purchaser of certain

commodities, such as corn, soybeans, livestock and natural gas in

the course of normal operations. The Company uses derivative

financial instruments to reduce its exposure to various market risks.

Generally, contract terms of a hedge instrument closely mirror

those of the hedged item, providing a high degree of risk reduction

and correlation. Contracts that are designated and highly effective

at meeting the risk reduction and correlation criteria are recorded

using hedge accounting, as defined by Statement of Financial

Accounting Standards No. 133, “Accounting for Derivative

Instruments and Hedging Activities” (SFAS No. 133), as amended.

If a derivative instrument is a hedge, as defined by SFAS No. 133,

depending on the nature of the hedge, changes in the fair value of

the instrument will be either offset against the change in fair value

of the hedged assets, liabilities or firm commitments through earn-

ings or recognized in other comprehensive income (loss) until the

hedged item is recognized in earnings. The ineffective portion of an

instrument’s change in fair value will be immediately recognized in

earnings as a component of cost of sales. Instruments the Company

holds as part of its risk management activities that do not meet

the criteria for hedge accounting, as defined by SFAS No. 133, as

amended, are marked to fair value with unrealized gains or losses

reported currently in earnings. The Company generally does not

hedge anticipated transactions beyond 12 months.