Tyson Foods 2005 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2005 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

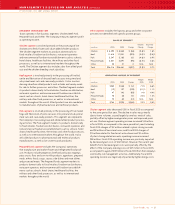

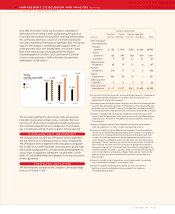

>> MANAGEMENT’S DISCUSSION AND ANALYSIS (CONTINUED)

TYSON FOODS, INC. 2005 ANNUAL REPORT

Tyson Foods, Inc. >> 20

2005 VS. 2004

Certain reclassifications have been made to prior periods to

conform to current presentations.

Sales decreased $427 million or 1.6%, with a 0.7% increase in average

sales price and a 2.3% decrease in volume. The decrease in sales

was primarily due to reduced sales in the Company’s Beef segment,

resulting from the effects of import and export restrictions. Addi-

tionally, sales were negatively impacted by decreased sales volumes

in each of the Company’s protein segments, primarily due to one

less week of sales in fiscal 2005. These declines were partially offset

by higher average sales prices in the Company’s Chicken, Pork and

Prepared Foods segments.

Cost of sales decreased $276 million or 1.1%. As a percent of sales,

cost of sales increased from 92.8% to 93.3%. The decrease in cost

of sales was primarily due to decreased grain costs of approximately

$312 million in fiscal 2005 as compared to the same period last year,

partially offset by higher live costs in the Pork segment, higher raw

material costs in the Prepared Foods segment and higher energy

costs. Additionally, the Chicken segment recorded losses of

$27 million in fiscal 2005 resulting from the Company’s commodity

risk management activities related to grain purchases as compared

to gains of $127 million in fiscal 2004. The fiscal 2004 gains were

due in part to grain commodity risk management activities that

were not designated as SFAS No. 133 hedges. Also, lower domestic

cattle supplies and restrictions on imports of Canadian cattle for

most of the year caused lower production volumes and higher

operating cost per head.

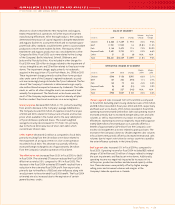

Selling, general and administrative expenses increased $48 million or

5.5%. As a percent of sales, selling, general and administrative expenses

increased from 3.3% to 3.6%. The increase was primarily due to an

increase of approximately $28 million in corporate advertising

expenses, which was primarily related to the Company’s “Powered

by Tyson” campaign. In addition, there were increases in personnel-

related costs and contributions and donations.

Other charges included $33 million related to a legal settlement

involving the Company’s live swine operations and $14 million

in plant closing costs, primarily related to the closings of the

Company’s Cleveland Street Forest, Mississippi, Portland, Maine,

and Bentonville, Arkansas, operations. In July 2005, the Company

announced it had agreed to settle a lawsuit which had resulted

from the restructuring of its live swine operations. The settlement

resulted in the Company recording an additional $33 million of

costs in the third quarter of fiscal 2005. In July 2005, the Company

announced its decision to make improvements to one of its Forest,

Mississippi, facilities, which will include more product lines,

enabling the plant to increase its production of processed and

marinated chicken. When the project is complete, the Company

will close the Cleveland Street Forest, Mississippi, poultry opera-

tion and transfer production and employees to the newly upgraded

facilities. Also in July 2005, the Company announced its decision to

close its Bentonville, Arkansas, facility. The production from this

facility was transferred to the Company’s Russellville, Arkansas,

poultry plant, where an expansion enabled the facility to absorb

the Bentonville facility’s production. In December 2004, the Company

announced its decision to close its Portland, Maine, facility. The

plant ceased operations February 4, 2005, and the production from

this facility was transferred to other locations. Other charges in

fiscal 2004 included $40 million in plant closing costs, primarily

related to the closings of the Company’s Jackson, Mississippi,

Manchester, New Hampshire, Augusta, Maine, and Berlin, Maryland,

operations. Also included in other charges for fiscal 2004 were

$25 million in charges related to intangible asset impairments

and $21 million related to fixed asset write-downs.

Interest expense decreased $48 million or 17.5%, primarily resulting

from an 8.7% decrease in the Company’s average indebtedness. In

addition, the Company incurred $13 million of expenses in fiscal 2004,

related to the buy back of bonds at attractive prices and the early

redemption of Tyson de Mexico preferred shares. Excluding these

charges, the overall weighted average borrowing rate decreased

from 7.4% to 7.1%.

Other expense decreased $5 million as compared to fiscal 2004,

primarily resulting from improvements in foreign exchange

gain/loss activity of approximately $9 million, primarily from

the Company’s Canadian operations, and an $8 million gain

recorded in fiscal 2005 from the sale of the Company’s remaining

interest in Specialty Brands, Inc. These items were partially offset

by increased losses of $13 million from the disposal of fixed assets.

The effective tax rate decreased from 36.6% in fiscal 2004 to 33.1% in

fiscal 2005. The fiscal 2005 effective rate was reduced by 4.1% due

to the release of income tax reserves that management deemed

were no longer required. In addition, the rate was increased by

4.2% relating to the repatriation of earnings of foreign subsidiaries

as allowed by the American Jobs Creation Act, offset by 2.9% relat-

ing to the reversal of certain international tax reserves that were

no longer needed due to the effects of the repatriation under

the American Jobs Creation Act. During the fourth quarter of

fiscal 2005, the Company repatriated $404 million of foreign earn-

ings invested outside the United States under the American Jobs

Creation Act. See Note 17 to the Consolidated Financial Statements

for further discussion of these issues. The estimated Extraterritorial

Income Exclusion (ETI) amount reduced the fiscal 2005 effective

tax rate by 2.6% compared to 0.5% in fiscal 2004. The increase in

the fiscal 2005 estimated ETI benefit resulted from an increase in

the estimated fiscal 2005 profit from export sales primarily due to

increased profit on export sales, along with an adjustment to the

estimated fiscal 2004 benefit.