Tyson Foods 2005 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2005 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

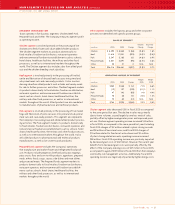

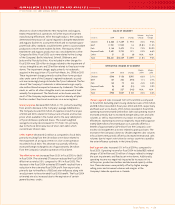

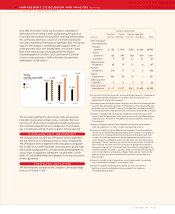

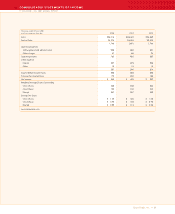

>> MANAGEMENT’S DISCUSSION AND ANALYSIS (CONTINUED)

TYSON FOODS, INC. 2005 ANNUAL REPORT

Tyson Foods, Inc. >> 26

RECENTLY ISSUED ACCOUNTING

STANDARDS AND REGULATIONS

In March 2005, the Financial Accounting Standards Board (FASB)

issued Interpretation No. 47, “Accounting for Conditional Asset

Retirement Obligations,” an interpretation of FASB Statement

No. 143 (the Interpretation). Statement of Financial Accounting

Standards No. 143, “Accounting for Asset Retirement Obligations”

(SFAS No. 143), was issued in June 2001 and requires an entity to

recognize the fair value of a liability for an asset retirement obliga-

tion in the period in which it is incurred if a reasonable estimate of

fair value can be made. SFAS No. 143 applies to legal obligations

associated with the retirement of a tangible long-lived asset that

resulted from the acquisition, construction, development and (or)

the normal operation of a long-lived asset. The associated asset

costs are capitalized as part of the carrying amount of the long-

lived asset. The Interpretation clarifies that the term “conditional

asset retirement obligation” as used in SFAS No. 143, refers to a legal

obligation to perform an asset retirement activity in which the

timing and (or) method of settlement are conditional on a future

event that may or may not be within the control of the entity. The

Interpretation requires an entity to recognize a liability for the fair

value of a conditional asset retirement obligation if the fair value

of the liability can be reasonably estimated. Uncertainty about the

timing and (or) method of settlement of a conditional asset retire-

ment obligation should be factored into the measurement of the

liability when sufficient information exists. SFAS No. 143 acknowl-

edges that in some cases, sufficient information may not be

available to reasonably estimate the fair value of an asset retire-

ment obligation. The Interpretation is effective for fiscal years

ending after December 15, 2005. The Company is currently in the

process of evaluating any potential effects of the Interpretation

but does not believe its adoption will have a material impact on

its consolidated financial statements.

In December 2004, the FASB issued Statement of Financial

Accounting Standards No. 123R, “Share-Based Payment”

(SFAS No. 123R), which is a revision of FASB Statement No. 123,

“Accounting for Stock-Based Compensation” (SFAS No. 123).

SFAS No. 123R supersedes Accounting Principles Board (APB)

Opinion No. 25, “Accounting for Stock Issued to Employees,” and

amends FASB Statement No. 95, “Statement of Cash Flows.” The

revision requires companies to measure and recognize compensa-

tion expense for all share-based payments to employees, including

grants of employee stock options, in the financial statements based

on the fair value at the date of the grant. SFAS No. 123R permits

companies to adopt its requirements using either the modified

prospective method or the modified retrospective method.

Under the modified prospective method, compensation cost is

recognized beginning with the effective date for all share-based

payments granted after the effective date and for all awards granted

to employees prior to the effective date of SFAS No. 123R that

remain unvested on the effective date. The modified retrospective

method includes the requirements of the modified prospective

method, but also permits entities to restate either all prior periods

presented or prior interim periods of the year of adoption for

the impact of adopting this standard. The Company will apply

the modified prospective method upon adoption. In April 2005,

the Securities and Exchange Commission announced it would

provide for phased-in implementation of SFAS No. 123R. As a result,

SFAS No. 123R is effective for the first interim or annual reporting

period of the registrant’s first fiscal year beginning on or after

June 15, 2005. The Company estimates that compensation expense

related to employee stock options for fiscal 2006 is expected to

be in the range of $10-$15 million. SFAS No. 123R also requires the

benefits of tax deductions in excess of recognized compensation

costs to be reported as financing cash flow, rather than as an

operating cash flow as required under current literature. This

requirement will reduce net operating cash flows and increase

net financing cash flows in periods after adoption. The Company

believes this reclass will not have a material impact on its

Consolidated Statements of Cash Flows.

In December 2004, the FASB issued Statement of Financial Account-

ing Standards No. 151, “Inventory Costs” (SFAS No. 151). SFAS No. 151

requires abnormal amounts of inventory costs related to idle facil-

ity, freight handling and wasted material expenses to be recognized

as current period charges. Additionally, SFAS No. 151 requires that

allocation of fixed production overheads to the costs of conver-

sion be based on the normal capacity of the production facilities.

The standard is effective for fiscal years beginning after June 15,

2005. The Company believes the adoption of SFAS No. 151 will not

have a material impact on its consolidated financial statements.

In October 2004, the President signed into law the American Jobs

Creation Act (the AJC Act). The AJC Act provides for the elimina-

tion of the ETI and allows for a federal income tax deduction for a

percentage of income earned from certain domestic production

activities. The Company’s domestic, or U.S., production activities

will qualify for the deduction. Based on the effective date of this

provision of the AJC Act, the Company will be eligible for this

deduction beginning in fiscal 2006. This provision will be phased in

from fiscal 2006 through fiscal 2011 and provides for a deduction of