Toyota 2008 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2008 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

105

•Annual Report 2008 • TOYOTA

Performance Messages from the Management &

•Overview •Management •Special Feature •Business Overview •Corporate Information •Financial Section •Investor Information •

These hypothetical scenarios do not reflect expected market

conditions and should not be used as a prediction of future per-

formance. As the figures indicate, changes in the fair value may

not be linear. Also, in this table, the effect of a variation in a par-

ticular assumption on the fair value of the retained interest is

calculated without changing any other assumption. Actual

changes in one factor may result in changes in another, which

might magnify or counteract the sensitivities. Actual cash flows

may differ from the above analysis.

fair values at the date of the sale. The key economic assump-

tions initially and subsequently measuring the fair value of

retained interests include the market interest rate environment,

severity and rate of credit losses, and the prepayment speed of

the receivables. All key economic assumptions used in the valu-

ation of the retained interests are reviewed periodically and are

revised as considered necessary.

At March 31, 2007 and 2008, Toyota’s retained interests relating

to these securitizations include interest in trusts, interest-only

strips, and other receivables, amounting to ¥16,033 million and

¥23,876 million ($238 million), respectively.

Toyota recorded no impairments on retained interests for the

years ended March 31, 2006, 2007 and 2008. Impairments are

calculated, if any, by discounting cash flows using manage-

ment’s estimates and other key economic assumptions.

Expected cumulative static pool losses over the life of the

securitizations are calculated by taking actual life to date losses

plus projected losses and dividing the sum by the original bal-

ance of each pool of assets. Expected cumulative static pool

credit losses for finance receivables securitized for the years

ended March 31, 2006, 2007 and 2008 were 0.19%, 0.16% and

0.26%, respectively.

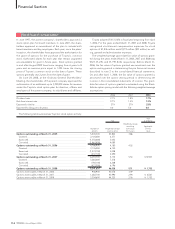

Key economic assumptions used in measuring the fair value of retained interests at the sale date of securitization transactions com-

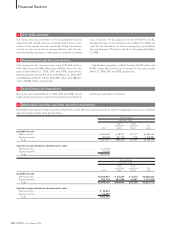

pleted during the years ended March 31, 2006, 2007 and 2008 were as follows:

For the years ended March 31,

2006 2007 2008

Prepayment speed related to securitizations ......................................................................... 0.7%–1.4% 0.7%–1.4% 6.0%

Weighted-average life (in years) .............................................................................................. 1.72–2.06 1.90–2.57 9.00

Expected annual credit losses.................................................................................................. 0.05%–0.18% 0.05%–0.12% 0.05%

Discount rate used on the retained interests.......................................................................... 5.0% 5.0% 3.8%

The key economic assumptions and the sensitivity of the current fair value of the retained interest to an immediate 10 and 20 percent

adverse change in those economic assumptions are presented below.

U.S. dollars

Yen in millions in millions

March 31, March 31,

2008 2008

Prepayment speed assumption (annual rate)..................................................................................................... 0.5%–6.0%

Impact on fair value of 10% adverse change.................................................................................................. ¥(302) $ (3)

Impact on fair value of 20% adverse change.................................................................................................. (514) (5)

Residual cash flows discount rate (annual rate).................................................................................................. 3.3%–6.0%

Impact on fair value of 10% adverse change.................................................................................................. ¥(708) $ (7)

Impact on fair value of 20% adverse change.................................................................................................. (1,376) (14)

Expected credit losses (annual rate).................................................................................................................... 0.05%–0.18%

Impact on fair value of 10% adverse change.................................................................................................. ¥(14) $ (0)

Impact on fair value of 20% adverse change.................................................................................................. (29) (0)

Outstanding receivable balances and delinquency amounts for managed retail and lease receivables, which include both owned and

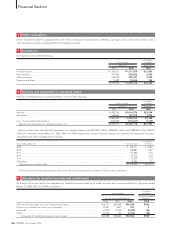

securitized receivables, as of March 31, 2007 and 2008 are as follows:

U.S. dollars

Yen in millions in millions

March 31, March 31,

2007 2008 2008

Principal amount outstanding........................................................................................................... ¥7,839,445 ¥7,867,964 $78,530

Delinquent amounts over 60 days or more ..................................................................................... 58,662 79,313 792

Comprised of:

Receivables owned........................................................................................................................ ¥7,664,178 ¥7,682,515 $76,679

Receivables securitized ................................................................................................................. 175,267 185,449 1,851

Credit losses, net of recoveries attributed to managed retail and lease receivables for the years ended March 31, 2006, 2007 and 2008

totaled ¥46,427 million, ¥63,428 million and ¥93,036 million ($929 million), respectively.