Spirit Airlines 2015 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2015 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

|

|

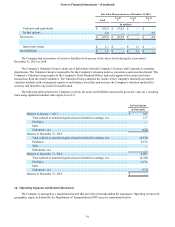

Notes to Financial Statements—(Continued)

89

15. Fair Value Measurements

Under ASC 820, Fair Value Measurements and Disclosures, disclosures relating to how fair value is determined for

assets and liabilities are required, and a hierarchy for which these assets and liabilities must be grouped is established, based on

significant levels of inputs, as follows:

Level 1—Quoted prices in active markets for identical assets or liabilities.

Level 2—Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices

in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for

substantially the full term of the assets or liabilities.

Level 3—Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of

the assets or liabilities.

Fair value is defined as the exchange price that would be received for an asset or paid to transfer a liability (an exit price)

in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on

the measurement date. The Company utilizes several valuation techniques in order to assess the fair value of the Company’s

financial assets and liabilities.

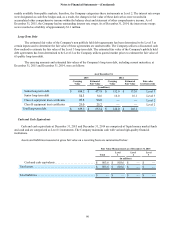

Fuel Derivative Instruments

The Company’s fuel derivative contracts generally consist of jet fuel swaps and jet fuel options. These instruments are

valued using energy and commodity market data, which is derived by combining raw inputs with quantitative models and

processes to generate forward curves and volatilities.

The Company utilizes the market approach to measure fair value for its fuel derivative instruments. The market approach

uses prices and other relevant information generated by market transactions involving identical or comparable assets or

liabilities.

The Company did not elect hedge accounting on any of the fuel derivative instruments. As a result, the Company records

the fair value adjustment of its fuel derivatives in the accompanying statement of operations within aircraft fuel and on the

balance sheet within prepaid expenses and other current assets or other current liabilities, depending on whether the net fair

value of the derivatives is on an asset or liability position as of the respective date. Fair values of the fuel derivative instruments

are determined using standard option valuation models. The Company also considers counterparty risk and its own credit risk

in its determination of all estimated fair values. The Company offsets fair value amounts recognized for derivative instruments

executed with the same counterparty under a master netting arrangement. The Company determines fair value of jet fuel

options utilizing an option pricing model based on inputs that are either readily available in public markets or can be derived

from information available in publicly quoted markets. The Company has consistently applied these valuation techniques in all

periods presented and believes it has obtained the most accurate information available for the types of derivative contracts it

holds.

The fair value of the Company's jet fuel swaps are determined based on inputs that are readily available in public markets

or can be derived from information available in publicly quoted markets; therefore, the Company categorizes these instruments

as Level 2. Due to the fact that certain inputs utilized to determine the fair value of jet fuel options are unobservable

(principally implied volatility), the Company categorizes these derivatives as Level 3. Implied volatility of a jet fuel option is

the volatility of the price of the underlying commodity that is implied by the market price of the option based on an option

pricing model. Thus, it is the volatility that when used in a particular pricing model, yields a theoretical value for the option

equal to the current market price of that option. Implied volatility, a forward-looking measure, differs from historical volatility

because the latter is calculated from known past returns. At each balance sheet date, the Company substantiates and adjusts

unobservable inputs. The Company routinely assesses the valuation model's sensitivity to changes in implied volatility. Based

on the Company's assessment of the valuation model's sensitivity to changes in implied volatility, it concluded that holding

other inputs constant, a significant increase (decrease) in implied volatility would result in significantly higher (lower)

determination of fair value measurement for the Company's aircraft fuel derivatives. As of December 31, 2015 and 2014, the

Company had no outstanding jet fuel derivatives.

Interest Rate Swaps

The fair value of the Company's interest rate swaps are based on observable inputs for active swap indications in quoted

markets for similar terms. The fair value of these instruments are determined using a market approach based on inputs that are