Spirit Airlines 2015 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2015 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

42

adjacent to the Gulf of Mexico. Gulf Coast fuel is subject to volatility and supply disruptions, particularly in hurricane season

when refinery shutdowns have occurred, or when the threat of weather-related disruptions has caused Gulf Coast fuel prices to

spike above other regional sources. Our derivatives, from time to time, generally may consist of United States Gulf Coast jet

fuel swaps (jet fuel swaps) and United States Gulf Coast jet fuel options (jet fuel options). Both jet fuel swaps and jet fuel

options can be used at times to protect the refining price risk between the price of crude oil and the price of refined jet fuel, and

to manage the risk of increasing fuel prices. Our fuel hedging practices are dependent upon many factors, including our

assessment of market conditions for fuel, our access to the capital necessary to support margin requirements, the pricing of

hedges and other derivative products in the market, our overall appetite for risk and applicable regulatory policies. As of

December 31, 2015, we had no outstanding jet fuel derivatives. As of December 31, 2015, we purchased all of our aircraft fuel

under a single fuel service contract. The cost and future availability of jet fuel cannot be predicted with any degree of certainty.

Labor. The airline industry is heavily unionized. The wages, benefits and work rules of unionized airline industry

employees are determined by collective bargaining agreements, or CBAs. Relations between air carriers and labor unions in the

United States are governed by the RLA. Under the RLA, CBAs generally contain “amendable dates” rather than expiration

dates, and the RLA requires that a carrier maintain the existing terms and conditions of employment following the amendable

date through a multi-stage and usually lengthy series of bargaining processes overseen by the NMB. This process continues

until either the parties have reached agreement on a new CBA, or the parties have been released to “self-help” by the NMB. In

most circumstances, the RLA prohibits strikes; however, after release by the NMB, carriers and unions are free to engage in

self-help measures such as strikes and lockouts.

We have four union-represented employee groups comprising approximately 73% of our employees at December 31,

2015. Our pilots are represented by the Airline Pilots Association, International, or ALPA, our flight attendants are represented

by the Association of Flight Attendants, or AFA-CWA, our flight dispatchers are represented by the Transport Workers Union

of America, or TWU, and our ramp service agents are represented by the International Association of Machinists and Aerospace

Workers, or IAMAW. Conflicts between airlines and their unions can lead to work slowdowns or stoppages. In June 2010, we

experienced a five-day strike by our pilots, which caused us to shut down our flight operations. The strike ended as a result of

our reaching a tentative agreement under a Return to Work Agreement and a full flight schedule was resumed on June 18, 2010.

On August 1, 2010, we entered into a five-year collective bargaining agreement with our pilots. In August 2015, our CBA with

our pilots became amendable and we are currently in discussions with ALPA regarding a new contract. In August 2013, we

entered into a five-year agreement with our flight dispatchers. In August 2014, with the help of the NMB, we reached a

tentative agreement for a five-year contract with our flight attendants. The tentative agreement was subject to ratification by the

flight attendant membership. On October 1, 2014, we were notified that the flight attendants voted to not ratify the tentative

agreement. We will continue to work together with the AFA-CWA and the NMB with a goal of reaching a mutually beneficial

agreement. On July 8, 2014, certain ramp service agents directly employed by us voted to be represented by the IAMAW. In

May 2015, we entered into a five-year interim collective bargaining agreement with the IAMAW, including material economic

terms, and we are in the process of negotiating a final collective bargaining agreement with the IAMAW. We believe the five-

year term of our CBAs is valuable in providing stability to our labor costs and provide us with competitive labor costs

compared to other U.S.-based low-cost carriers. If we are unable to reach agreement with any of our unionized work groups in

current or future negotiations regarding the terms of their CBAs, we may be subject to work interruptions or stoppages, such as

the strike by our pilots in June 2010. A strike or other significant labor dispute with our unionized employees is likely to

adversely affect our ability to conduct business. Any agreement we do reach could increase our labor and related expenses.

In 2010, the Patient Protection and Affordable Care Act was passed into law. While much of the cost of the healthcare

legislation enacted will occur after 2015 due to provisions of the legislation being delayed and phased in over time, we expect

changes to our healthcare cost structure could potentially increase our operating costs, with healthcare costs increasing at a

higher rate than our employee headcount.

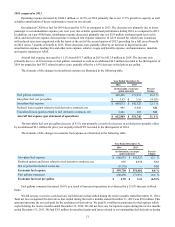

Maintenance Expense. Maintenance expense grew through 2015, 2014 and 2013 mainly as a result of a growing fleet and

the gradual increase of required maintenance for the older aircraft in our fleet. As the fleet ages, we expect that maintenance

costs will increase in absolute terms. The amount of total maintenance costs and related amortization of heavy maintenance

(included in depreciation and amortization expense) is subject to many variables such as future utilization rates, average stage

length, the interval between heavy maintenance events, the size and makeup of the fleet in future periods and the level of

unscheduled maintenance events and their actual costs. Accordingly, we cannot reliably quantify future maintenance expenses

for any significant period of time. However, we believe, based on our scheduled maintenance events, maintenance expense and

maintenance-related amortization expense in 2016 will be approximately $164 million. In addition, we expect to capitalize $92

million of costs for heavy maintenance during 2016.

As a result of a significant portion of our fleet being acquired over a relatively short period of time, heavy

maintenance scheduled on each of our planes will occur at roughly the same time, meaning we will incur our most expensive