Samsung 2013 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2013 Samsung annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

|

|

58 59

2013 SAMSUNG ELECTRONICS ANNUAL REPORT

2.10 Disposal Group Held-for-Sale

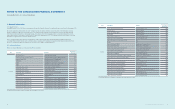

Non-current assets (or disposal group) are classied as assets held-for-

sale when their carrying amount is to be recovered principally through a

sale transaction and a sale is considered highly probable. The assets are

measured at the lower amount between their carrying amount and the fair

value less costs to sell.

2.11 Property, Plant and Equipment

Property, plant and equipment are stated at cost less accumulated

depreciation and accumulated impairment losses.

Historical cost includes expenditures that are directly attributable to

the acquisition of the items. Subsequent costs are included in the asset’s

carrying amount or recognized as a separate asset, as appropriate,

only when it is probable that future economic benets associated with

the item will ow to the Company and the cost of the item can be

measured reliably. The carrying amount of those parts that are replaced

is derecognized and repairs and maintenance expenses are recognized in

prot or loss in the period they are incurred.

Depreciation on tangible assets is calculated using the straight-line method

to allocate the difference between their cost and their residual values over

their estimated useful lives. Land is not depreciated. Costs that are directly

attributable to the acquisition, construction or production of a qualifying

asset, including capitalized interest costs, form part of the cost of that asset

and are amortized over the estimated useful lives.

The Company’s policy is that property, plant and equipment should be

depreciated over the following estimated useful lives:

Estimated useful lives

Buildings and structures 15, 30 years

Machinery and equipment 5 years

Others 5 years

The depreciation method, residual values and useful lives of property,

plant and equipment are reviewed, and adjusted if appropriate,

at the end of each reporting period. An asset’s carrying amount is written

down immediately to its recoverable amount if the asset’s carrying amount

is greater than its estimated recoverable amount. Gains and losses on

disposals are determined by comparing the proceeds with the carrying

amount and are recognized within the statement of income as part of other

non-operating income and expenses.

2.12 Intangible Assets

Goodwill represents the excess of the cost of an acquisition over the fair

value of the group’s share of the net identiable assets of the acquired

subsidiary, associates, joint ventures and businesses at the date of

acquisition.

Goodwill on acquisitions of subsidiaries and businesses is included in

intangible assets and goodwill on acquisition of associates and joint

ventures are included in the investments in associates and joint ventures.

Intangible assets, except for goodwill, are initially recognized at their

historical cost and carried at cost less accumulated amortization and

accumulated impairment losses.

Internally generated development costs are the aggregate costs recognized

after meeting the asset recognition criteria, including technical feasibility,

and determined to have future economic benets. Membership rights are

regarded as intangible assets with indenite useful life and not amortized

because there is no foreseeable limit to the period over which the assets

are expected to be utilized. Intangible assets with denite useful life such as

trademarks and licenses are amortized using the straight-line method over

their estimated useful lives.

The Company’s policy is that intangible assets should be amortized over

the following estimated useful lives:

Estimated useful lives

Development costs 2 years

Trademarks, licenses and other intangible assets 5-10 years

2.13 Impairment of Non-Financial Assets

Goodwill or intangible assets with indenite useful life are not subject to

amortization and are tested annually for impairment. Assets that are subject

to amortization are reviewed for impairment whenever events or changes

in circumstances indicate that the carrying amount may not be recoverable.

An impairment loss is recognized for the amount by which the asset’s

carrying amount exceeds its recoverable amount. The recoverable amount

is the higher of an asset’s fair value less costs to sell and value in use.

For the purposes of assessing impairment, assets are grouped at the lowest

levels for which there are separately identiable cash ows (cash-generating

units). Non-nancial assets other than goodwill that suffered impairment are

reviewed for possible reversal of the impairment at each reporting date.

2.14 Financial Liabilities

(A) Classication and measurement

Financial liabilities at fair value through prot or loss are nancial

instruments held for trading. Financial liabilities are classied in this

category if incurred principally for the purpose of repurchasing them in the

near term. Derivatives that are not designated as hedges or bifurcated from

nancial instruments containing embedded derivatives are also categorized

as held-for-trading.

The Company classies non-derivative nancial liabilities, except for

nancial liabilities at fair value through prot or loss, nancial guarantee

contracts and nancial liabilities that arise when a transfer of nancial

assets does not qualify for derecognition, as nancial liabilities carried at

amortized cost and presented as ‘trade payables’, ‘borrowings’, and ‘other

nancial liabilities’ in the statement of nancial position.

(B) Derecognition

Financial liabilities are removed from the statement of nancial position

when it is extinguished, for example, when the obligation specied in

the contract is discharged, cancelled or expired or when the terms of

an existing nancial liability are substantially modied.

2.15 Trade Payables

Trade payables are amounts due to suppliers for merchandise purchased or

services received in the ordinary course of business. If payment is expected

in one year or less (or in the normal operating cycle of the Company if

longer), they are classied as current liabilities. If not, they are presented as

non-current liabilities. Non-current trade payables are recognized initially at

fair value and subsequently measured at amortized cost using the effective

interest method.

2.16 Borrowings

Borrowings are recognized initially at fair value, net of transaction costs

and are subsequently measured at amortized cost. Any difference between

cost and the redemption value is recognized in the statement of income

over the period of the borrowings using the effective interest method. If the

Company has an indenite right to defer payment for a period longer than

12 months after the end of the reporting date, such liabilities are recorded

as non-current liabilities, otherwise, they are recorded as current liabilities.

2.17 Provisions

A provision is recognized when the Company has a present legal or

constructive obligation as a result of a past event, it is probable that

an outow of resources embodying economic benets will be required to

settle the obligation, and a reliable estimate can be made of the amount of

the obligation. Provisions are not recognized for future operating losses.

Provisions are measured at the present value of the expenditures expected

to be required to settle the obligation using a pre-tax rate that reects

current market assessments of the time value of money and the risks

specic to the obligation. The increase in the provision due to passage of

time is recognized as interest expense.

When it is probable that an outow of economic benets will occur due to

a present obligation resulting from a past event, and the amount is

reasonably estimable, a corresponding provision is recognized in

the nancial statements. However, when such outow is dependent upon

a future event, that is not certain to occur, or cannot be reliably estimated,

a disclosure regarding the contingent liability is made in the notes to

the nancial statements.

2.18 Net Dened Benet Liabilities

The Company has a variety of retirement pension plans including dened

benet or dened contribution plans. A dened contribution plan is

a pension plan under which the Company pays xed contributions into

a separate entity. The Company has no legal or constructive obligations to

pay further contributions if the fund does not hold sufcient assets to pay all

employees the benets relating to employee service in the current and prior

periods. For dened contribution plans, the Company pays contributions to

annuity plans that are managed either publicly or privately on a mandatory,

contractual or voluntary basis. The Company has no further future payment

obligations once the contributions have been paid. The contributions are

recognized as employee benet expense when they are due.

Prepaid contributions are recognized as an asset to the extent that a cash

refund or a reduction in the future payments is available.

A dened benet plan is a pension plan that is not a dened contribution

plan. Typically dened benet plans dene an amount of pension benet

that an employee will receive on retirement, usually dependent on one or

more factors such as age, years of service and compensation. The liability

recognized in the statement of nancial position in respect to dened

benet pension plans is the present value of the dened benet obligation at

the end of the reporting period less the fair value of plan assets. The dened

benet obligation is calculated annually by independent actuaries using

the projected unit credit method. The present value of the dened benet

obligation is determined by discounting the estimated future cash outows

using interest rates of high-quality corporate bonds that are denominated

in the currency in which the benets will be paid and that have terms to

maturity approximating to the terms of the related pension obligation.

Actuarial gains and losses resulting from the changes in actuarial

assumptions, and the differences between the previous actuarial

assumptions and what has actually occurred, are recognized in other

comprehensive income in the period in which they were incurred.

Past service costs are immediately recognized in prot or loss.

2.19 Financial Guarantee Contract

Financial guarantee contracts are contracts that require the issuer to make

specied payments to reimburse the holder for a loss it incurs because

a specied debtor fails to make payments when due. Financial guarantees

are initially recognized in the nancial statements at fair value on the date

the guarantee was given. If the amount measured in subsequent periods

exceeds the unamortized balance of the amount initially recognized,

the excess is classied as other nancial liability.

2.20 Current and Deferred Tax

The tax expense for the period comprises current and deferred tax.

Tax is recognized on the prot for the period in the statement of income,

except to the extent that it relates to items recognized in other

comprehensive income or directly in equity, in which case the tax is also

recognized in other comprehensive income or directly in equity, respectively.

The tax expense is calculated on the basis of the tax laws enacted or

substantively enacted at the end of the reporting period.

Deferred tax is recognized for temporary differences arising between

the tax bases of assets and liabilities and their carrying amounts as

expected tax consequences at the recovery or settlement of the carrying

amounts of the assets and liabilities. However, deferred tax assets and

liabilities are not recognized if they arise from initial recognition of an asset

or liability in a transaction other than a business combination that

at the time of the transaction affects neither accounting nor taxable prot or

loss. Deferred tax assets are recognized only to the extent that it is probable

that future taxable prot will be available against which the temporary

differences can be utilized.

A deferred tax liability is recognized for taxable temporary differences

associated with investments in subsidiaries, associates, and interests in

joint ventures, except to the extent that the Company is able to control

the timing of the reversal of the temporary differences and it is probable

that the temporary difference will not reverse in the foreseeable future.

In addition, a deferred tax asset is recognized for deductible temporary

differences arising from such investments to the extent that it is probable

the temporary difference will reverse in the foreseeable future and taxable

prot will be available against which the temporary difference can be utilized.