Radio Shack 2004 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2004 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

Recently Issued Accounting Pronouncements

In December 2003, the Financial Accounting Standards Board

(the “FASB”) issued revised FIN 46, “Consolidation of Variable

Interest Entities, an Interpretation of Accounting Research

Bulletin No. 51” (“FIN 46R”). FIN 46R requires the consolida-

tion of an entity in which an enterprise absorbs a majority of

the entity’s expected losses, receives a majority of the entity's

expected residual returns, or both, as a result of ownership,

contractual or other financial interests in the entity (variable

interest entities or “VIEs”). FIN 46R is applicable for financial

statements of public entities that have interests in VIEs or

potential VIEs referred to as special-purpose entities for peri-

ods ending after December 31, 2003. Applications by public

entities for all other types of entities are required in financial

statements for periods ending after March 15, 2004. The

application of FIN 46R did not have a material impact on our

results of operations, financial position or liquidity, and does

not apply to our dealer outlets.

In December 2004, the FASB issued Statement of Financial

Accounting Standards (“SFAS”) No. 123R “Share-Based

Payment.” SFAS No. 123R establishes standards for the

accounting for transactions in which an entity exchanges its

equity instruments for goods or services. This Statement

focuses primarily on accounting for transactions in which an

entity obtains employee services in share-based payment

transactions. SFAS No. 123R requires that the fair value of

such equity instruments be recognized as an expense in the

historical financial statements as services are performed. Prior

to SFAS 123R, only certain pro forma disclosures of fair value

were required. We will adopt the provisions of SFAS No.

123R beginning with the third quarter of 2005. We intend to

elect the modified prospective transition method, which will

require that we recognize compensation expense for all new

and unvested share-based payment awards from the effective

date. Based on our preliminary analysis of SFAS No. 123R, we

anticipate the after-tax impact of adoption on our results of

operations for the six months ending December 31, 2005, will

be an expense of approximately $6.8 million.

During fiscal year 2004, we adopted Emerging Issues Task

Force (“EITF”) Issue No. 03-10, “Application of Issue No. 02-

16 by Resellers to Sales Incentives Offered to Consumers by

Manufacturers,” which amends EITF No. 02-16. According to

the amended guidance, if certain criteria are met, considera-

tion received by a reseller in the form of reimbursement from

a vendor for honoring the vendor’s sales incentives offered

directly to consumers (i.e., manufacturers’ coupons) should

not be recorded as a reduction of the cost of the reseller’s

purchases from the vendor. The adoption of EITF No. 03-10

did not materially impact our results of operations, financial

position or liquidity in fiscal year 2004.

In November 2004, the FASB issued SFAS No. 151,

“Inventory Costs.” The new Statement amends Accounting

Research Bulletin No. 43, Chapter 4, “Inventory Pricing,” to

clarify the accounting for abnormal amounts of idle facility

expense, freight, handling costs, and wasted material. SFAS

151 requires that these items be recognized as current-period

charges and requires that allocation of fixed production over-

head to the cost of conversion be based on the normal

capacity of the production facilities. This statement is effec-

tive for fiscal years beginning after June 15, 2005. We do

not expect adoption of this statement to have a material

impact on our financial condition or results of operations.

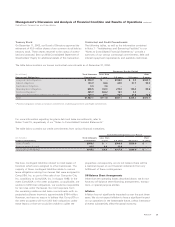

Cash Flow and Liquidity

A summary of cash flows from operating, investing and

financing activities is outlined in the table below.

Year Ended December 31,

(In millions) 2004 2003 2002

Operating activities $ 352.5 $ 651.9 $521.6

Investing activities (290.2) (188.9) (99.0)

Financing activities (259.1) (274.8) (377.5)

Cash Flow – Operating Activities

In 2004, cash flows provided by operating activities were

$352.5 million, compared to $651.9 million and $521.6

million in 2003 and 2002, respectively.

During the year ended December 31, 2004, increases in

accounts receivable, consisting primarily of amounts due

from our various vendors and third-party service providers,

used $53.0 million in cash, compared to $17.2 million provid-

ed in the prior year. An increase in vendor and service

provider receivables due to an increase in sales of wireless

services resulted in a cash usage by accounts receivable in

2004, while cash provided in 2003 was the result of reduc-

tions of vendor and service provider receivables and dealer

receivables from increased collections and lower sales of

satellite television hardware.

During the year ended December 31, 2004, increases in

inventory used $234.2 million in cash, compared to $202.3

million provided during 2003. The increase in inventory since

December 31, 2003, was primarily the result of abnormally

low inventory levels during the holiday selling season of 2003

and additional inventory purchased to stock the new kiosk

locations during the fourth quarter of 2004.

Typically, our annual cash requirements for pre-seasonal inven-

tory build-up range between $200 million and $400 million.

The funding required for this build-up comes primarily from

cash on hand and cash generated from net sales and operat-

Management’s Discussion and Analysis of Financial Condition and Results of Operations continued

RadioShack Corporation and Subsidiaries

25

AR2004