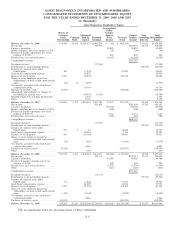

Quest Diagnostics 2009 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2009 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

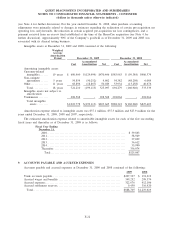

|

|

Effective June 30, 2009, the Company adopted a newly issued accounting standard related to accounting for

and disclosure of subsequent events in its consolidated financial statements. This standard provides the

authoritative guidance for subsequent events that was previously addressed only in United States auditing

standards. This standard establishes general accounting for and disclosure of events that occur after the balance

sheet date but before financial statements are issued or are available to be issued and requires the Company to

disclose the date through which it has evaluated subsequent events and whether that was the date the financial

statements were issued or available to be issued. This standard does not apply to subsequent events or

transactions that are within the scope of other applicable GAAP that provide different guidance on the accounting

treatment for subsequent events or transactions. The adoption of this standard did not have a material impact on

the Company’s consolidated financial statements.

In June 2009, the FASB issued an amendment to the accounting standards related to the consolidation of

variable interest entities (“VIE”). This standard provides a new approach for determining which entity should

consolidate a VIE, how and when to reconsider the consolidation or deconsolidation of a VIE and requires

disclosures about an entity’s significant judgments and assumptions used in its decision to consolidate or not

consolidate a VIE. Under this standard, the new consolidation model is a more qualitative assessment of power

and economics that considers which entity has the power to direct the activities that “most significantly impact”

the VIE’ s economic performance and has the obligation to absorb losses or the right to receive benefits that

could be potentially significant to the VIE. This standard is effective for the Company as of January 1, 2010 and

the Company does not expect the impact of its adoption to be material to its consolidated financial statements.

In October 2009, the FASB issued an amendment to the accounting standards related to the accounting for

revenue in arrangements with multiple deliverables including how the arrangement consideration is allocated

among delivered and undelivered items of the arrangement. Among the amendments, this standard eliminates the

use of the residual method for allocating arrangement consideration and requires an entity to allocate the overall

consideration to each deliverable based on an estimated selling price of each individual deliverable in the

arrangement in the absence of having vendor-specific objective evidence or other third party evidence of fair

value of the undelivered items. This standard also provides further guidance on how to determine a separate unit

of accounting in a multiple-deliverable revenue arrangement and expands the disclosure requirements about the

judgments made in applying the estimated selling price method and how those judgments affect the timing or

amount of revenue recognition. This standard, for which the Company is currently assessing the impact, will

become effective for the Company on January 1, 2011.

In October 2009, the FASB issued an amendment to the accounting standards related to certain revenue

arrangements that include software elements. This standard clarifies the existing accounting guidance such that

tangible products that contain both software and non-software components that function together to deliver the

product’s essential functionality, shall be excluded from the scope of the software revenue recognition accounting

standards. Accordingly, sales of these products may fall within the scope of other revenue recognition accounting

standards or may now be within the scope of this standard and may require an allocation of the arrangement

consideration for each element of the arrangement. This standard, for which the Company is currently assessing

the impact, will become effective for the Company on January 1, 2011.

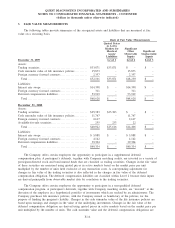

In January 2010, the FASB issued an amendment to the accounting standards related to the disclosures about

an entity’s use of fair value measurements. Among these amendments, entities will be required to provide

enhanced disclosures about transfers into and out of the Level 1(fair value determined based on quoted prices in

active markets for identical assets and liabilities) and Level 2 (fair value determined based on significant other

observable inputs) classifications, provide separate disclosures about purchases, sales, issuances and settlements

relating to the tabular reconciliation of beginning and ending balances of the Level 3 (fair value determined

based on significant unobservable inputs) classification and provide greater disaggregation for each class of assets

and liabilities that use fair value measurements. Except for the detailed Level 3 roll-forward disclosures, the new

standard is effective for the Company for interim and annual reporting periods beginning after December 31,

2009. The requirement to provide detailed disclosures about the purchases, sales, issuances and settlements in the

roll-forward activity for Level 3 fair value measurements is effective for the Company for interim and annual

reporting periods beginning after December 31, 2010. The Company does not expect that the adoption of this

new standard will have a material impact to its consolidated financial statements.

F-15

QUEST DIAGNOSTICS INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(dollars in thousands unless otherwise indicated)