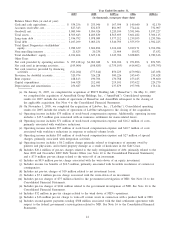

Quest Diagnostics 2009 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2009 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Healthcare insurers, which typically negotiate directly or indirectly on behalf of their members, represent

approximately one-half of our clinical testing volumes and one-half of our net revenues from our clinical testing

business. Larger healthcare insurers typically prefer to use large commercial clinical laboratories because they can

provide services to their members on a national or regional basis. In addition, larger commercial clinical

laboratories are better able to achieve the low-cost structures necessary to profitably service the members of large

healthcare insurers and can provide test utilization data across various products in a consistent format. In certain

markets, such as California, healthcare insurers may delegate their covered members to independent physician

associations, which in turn negotiate with laboratories for clinical testing services on behalf of their members.

The trend of consolidation among physicians, hospitals, employers, healthcare insurers, pharmaceutical

companies and other intermediaries has continued, resulting in fewer but larger customers and payers with

significant bargaining power to negotiate fee arrangements with healthcare providers, including clinical

laboratories. Healthcare insurers often require that clinical testing service providers accept discounted fee

structures or assume all or a portion of the utilization risk associated with providing testing services to their

members enrolled in highly-restricted plans through capitated payment arrangements. Under these capitated

payment arrangements, we and the healthcare insurers agree to a predetermined monthly reimbursement rate for

each member enrolled in the healthcare plan’s restricted plan, generally regardless of the number or cost of

services provided by us. Our cost to perform testing services reimbursed under capitated payment arrangements is

not materially different from our cost to perform testing services reimbursed under other arrangements with

healthcare insurers. Since average reimbursement rates under capitated payment arrangements are typically less

than our overall average reimbursement rate, the testing services reimbursed under capitated payment

arrangements are generally less profitable. In 2009, we derived approximately 14% of our testing volume and 5%

of our clinical testing net revenues from capitated payment arrangements.

Most healthcare insurers also offer programs such as preferred provider organizations (“PPOs”) and

consumer driven health plans that offer a greater choice of healthcare providers. Pricing for these programs is

typically negotiated on a fee-for-service basis, which generally results in higher revenue per requisition than

under capitation arrangements. Most of our agreements with major healthcare insurers are non-exclusive

arrangements. As a result, under these non-exclusive arrangements, physicians and patients have more freedom of

choice in selecting laboratories, and laboratories are likely to compete more on the basis of service and quality

than they may otherwise. It is increasingly important for healthcare providers to differentiate themselves based on

quality, service and convenience to avoid competing on price alone.

Despite the general trend of increased choice for patients in selecting a healthcare provider, recent

experience indicates that some healthcare insurers may actively seek to limit the choice of patients and physicians

if they feel it will give them increased leverage to negotiate lower fees, by consolidating services with a single

or limited network of contracted providers. Historically, healthcare insurers, which had limited their network of

laboratory service providers, encouraged their members, and sometimes offered incentives, to utilize only

contracted providers. Patients who use a non-contracted provider may have a higher co-insurance responsibility,

which may result in physicians referring testing to contracted providers to minimize the expense to their patients.

In cases where members choose to use a non-contracted provider due to service, quality or convenience, the non-

contracted provider would be reimbursed at rates considered “reasonable and customary.” Contracted rates are

generally lower than “reasonable and customary” rates.

We also may be a member of a “complementary network.” A complementary network is generally a set of

contractual arrangements that a third party will maintain with various providers which provide discounted fees for

the benefit of its customers. A member of a health plan may choose to access a non-contracted provider that is a

member of a complementary network; if so, the provider will be reimbursed at a rate negotiated by the

complementary network.

We expect that reimbursements for the diagnostic testing industry will continue to remain under pressure.

Today, the federal and many state governments face serious budget deficits and healthcare spending is subject to

reductions, and efforts to reduce reimbursements and stringent cost controls by government and other payers for

existing tests may continue. However, we believe that as new tests are developed which either improve on the

effectiveness of existing tests or provide new diagnostic capabilities, the government and other payers will add

these tests as covered services, because of the importance of laboratory testing in assessing and managing the

health of patients. We continue to emphasize the importance and the high value of laboratory testing with

healthcare insurers and government payers at the federal and state level.

43