Oracle 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

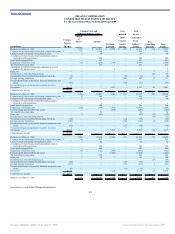

Table of Contents

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2010

based upon the accounting guidance contained in ASC 605, Revenue Recognition, and we exercise judgment and use estimates in connection with the

determination of the amount of hardware systems products and hardware systems related services revenues to be recognized in each accounting period.

Revenues from the sales of hardware products are recognized when: (1) persuasive evidence of an arrangement exists; (2) we deliver the products and passage of

the title to the buyer occurs; (3) the sale price is fixed or determinable; and (4) collection is reasonably assured. Revenues that are not recognized at the time of

sale because the foregoing conditions are not met are recognized when those conditions are subsequently met. When applicable, we reduce revenues for

estimated returns or certain other incentive programs where we have the ability to sufficiently estimate the effects of these items. Where an arrangement is

subject to acceptance criteria and the acceptance provisions are not perfunctory (for example, acceptance provisions that are long-term in nature or are not

included as standard terms of an arrangement), revenues are recognized upon the earlier of receipt of written customer acceptance or expiration of the acceptance

period.

Our hardware systems support offerings generally provide customers with software updates for the software components that are essential to the functionality of

our systems and storage products and can also include product repairs, maintenance services, and technical support services. Hardware systems support contracts

are entered into at the customer’s option and are recognized ratably over the contractual term of the arrangements.

Revenue Recognition for Multiple-Element Arrangements – Hardware Systems Products and Hardware Systems Related Services (Nonsoftware Arrangements)

In the third quarter of fiscal 2010, we early adopted the provisions of Accounting Standards Update No. 2009-13, Revenue Recognition (Topic 605)

Multiple-Deliverable Revenue Arrangements (ASU 2009-13) and Accounting Standards Update 2009-14, Software (Topic 985)—Certain Revenue Arrangements

that Include Software Elements (ASU 2009-14). ASU 2009-13 amended existing accounting guidance for revenue recognition for multiple-element

arrangements. To the extent a deliverable within a multiple-element arrangement is not accounted for pursuant to other accounting standards, including ASC

985-605, Software-Revenue Recognition, ASU 2009-13 establishes a selling price hierarchy that allows for the use of an estimated selling price (ESP) to

determine the allocation of arrangement consideration to a deliverable in a multiple element arrangement where neither VSOE nor third-party evidence (TPE) is

available for that deliverable. ASU 2009-14 modifies the scope of ASC 985-605 to exclude tangible products containing software components and nonsoftware

components that function together to deliver the product’s essential functionality. In addition, ASU 2009-14 provides guidance on how a vendor should allocate

arrangement consideration to nonsoftware and software deliverables in an arrangement where the vendor sells tangible products containing software components

that are essential in delivering the tangible product’s functionality.

As a result of our early adoption of ASU 2009-13 and ASU 2009-14, we applied the provisions of these accounting standards updates as of the beginning of

fiscal 2010. The impact of our adoption of ASU 2009-13 and ASU 2009-14 was not material to our results of operations for fiscal 2010.

We enter into arrangements with customers that purchase both nonsoftware related products and services from us at the same time, or within close proximity of

one another (referred to as nonsoftware multiple-element arrangements). Each element within a nonsoftware multiple-element arrangement is accounted for as a

separate unit of accounting provided the following criteria are met: the delivered products or services have value to the customer on a standalone basis; and for an

arrangement that includes a general right of return relative to the delivered products or services, delivery or performance of the undelivered product or service is

considered probable and is substantially controlled by us. We consider a deliverable to have standalone value if the product or service is sold separately by us or

another vendor or could be resold by the customer. Further, our revenue arrangements generally do not include a general right of return relative to the delivered

products. Where the aforementioned criteria for a separate unit of accounting are not met, the deliverable is combined with the undelivered element(s) and treated

as a single unit of accounting for the purposes of allocation of the

93

Source: ORACLE CORP, 10-K, July 01, 2010 Powered by Morningstar® Document Research℠