Nissan 2004 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2004 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Nissan Annual Report 2003

60

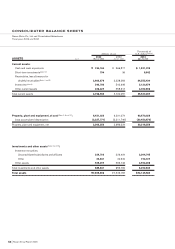

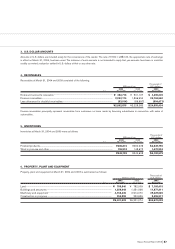

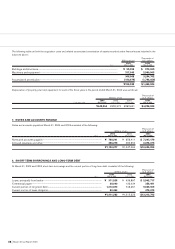

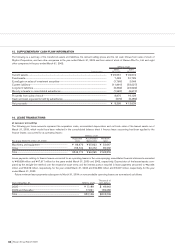

9. RETIREMENT BENEFIT PLANS

The Company and its domestic consolidated subsidiaries have defined benefit plans, i.e., welfare pension fund plans (WPFP), tax-qualified

pension plans and lump-sum payment plans, covering substantially all employees who are entitled to lump-sum or annuity payments, the

amounts of which are determined by reference to their basic rates of pay, length of service, and the conditions under which termination

occurs. Certain foreign consolidated subsidiaries have defined benefit and contribution plans.

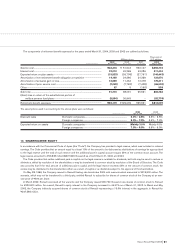

The following table sets forth the funded and accrued status of the plans, and the amounts recognized in the consolidated balance sheets

as of March 31, 2004 and 2003 for the Company’s and the consolidated subsidiaries’ defined benefit plans:

Thousands of

Millions of yen U.S. dollars

2003 2002 2003

As of Mar. 31, 2004 Mar. 31, 2003 Mar. 31, 2004

Retirement benefit obligation.................................................................................................. ¥(1,041,483) ¥(1,135,273) $(9,825,311)

Plan assets at fair value............................................................................................................ 377,169 359,922 3,558,198

Unfunded retirement benefit obligation................................................................................ (664,314) (775,351) (6,267,113)

Unrecognized net retirement benefit obligation at transition........................................... 131,666 179,611 1,242,132

Unrecognized actuarial gain or loss...................................................................................... 152,867 231,637 1,442,141

Unrecognized prior service cost ............................................................................................ (61,833) (69,134) (583,330)

Net retirement benefit obligation ........................................................................................... (441,614) (433,237) (4,166,170)

Prepaid pension cost................................................................................................................ 652 29 6,151

Accrued retirement benefits.................................................................................................... ¥ (442,266) ¥(433,266) $(4,172,321)

The substitutional portion of the benefits under the WPFP has been included in the amounts shown in the above table.

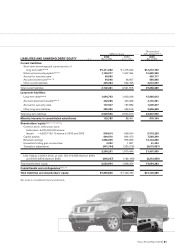

The Company received approval from the Minister of Health, Labor and Welfare (“MHLW”) in the year ended March 31, 2003 with respect

to its application for exemption from the obligation for benefits related to future employee services under the substitutional portion of the

WPFP. Certain domestic consolidated subsidiaries received the same approval from MHLW during the year ended March 31, 2004. In accor-

dance with the transitional provision stipulated in “Practical Guidelines for Accounting for Retirement Benefits,” the Company and the domes-

tic consolidated subsidiaries accounted for the separation of the substitutional portion of the benefit obligation from the corporate portion of

the benefit obligation under their WPFPs as of the dates of approval for their exemption assuming that the transfer to the Japanese govern-

ment of the substitutional portion of the benefit obligation and related pension plan assets had been completed as of those dates. As a result,

the Company recognized a loss of ¥30,945 million for the year ended March 31, 2003 and the domestic consolidated subsidiaries recog-

nized an aggregate gain of ¥3,669 million ($34,613 thousand) and an aggregate loss of ¥1,587 million ($14,972 thousand) for the year

ended March 31, 2004. The pension assets to be transferred were calculated at ¥35,770 million ($337,453 thousand) for the domestic con-

solidated subsidiaries at March 31, 2004 and ¥241,203 million for the Company at March 31, 2003.