Nissan 2004 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2004 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Nissan Annual Report 2003 55

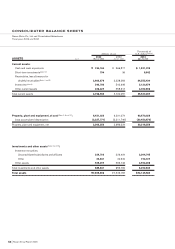

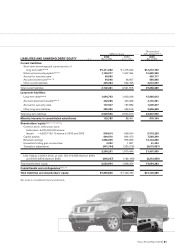

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Nissan Motor Co., Ltd. and Consolidated Subsidiaries

Fiscal year 2003 (Year ended March 31, 2004)

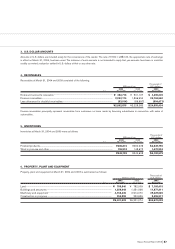

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Presentation

Nissan Motor Co., Ltd. (the “Company”) and its domestic subsidiaries

maintain their books of account in conformity with the financial

accounting standards of Japan, and its foreign subsidiaries maintain

their books of account in conformity with those of their countries of

domicile.

The accompanying consolidated financial statements have been

prepared in accordance with accounting principles generally accepted

in Japan, which are different in certain respects as to the application

and disclosure requirements of International Financial Reporting

Standards, and have been compiled from the consolidated financial

statements prepared by the Company as required by the Securities

and Exchange Law of Japan.

Certain amounts in the prior years’ financial statements have been

reclassified to conform to the current year’s presentation.

(b) Principles of consolidation and accounting for investments

in unconsolidated subsidiaries and affiliates

The accompanying consolidated financial statements include the

accounts of the Company and any significant companies controlled

directly or indirectly by the Company. Companies over which the

Company exercises significant influence in terms of their operating

and financial policies have been included in the consolidated financial

statements on an equity basis. All significant intercompany balances

and transactions have been eliminated in consolidation.

The financial statements of the Company’s subsidiaries in certain

foreign countries including Mexico have been prepared based on

general price-level accounting. The related revaluation adjustments

made to reflect the effect of inflation in those countries in the accom-

panying consolidated financial statements have been charged or

credited to operations and are directly reflected in retained earnings.

Investments in subsidiaries and affiliates which are not consolidated

or accounted for by the equity method are carried at cost or less.

Where there has been a permanent decline in the value of such

investments, the Company has written down the investments.

Differences between the cost and the underlying net equity at fair

value of investments in consolidated subsidiaries and in companies

which are accounted for by the equity method have been amortized

by the straight-line method over periods not exceeding 20 years.

(c) Foreign currency translation

The balance sheet accounts of the foreign consolidated subsidiaries

are translated into yen at the rates of exchange in effect at the bal-

ance sheet date, except for the components of shareholders’ equity

which are translated at their historical exchange rates. Revenue and

expense accounts are translated at the average rate of exchange in

effect during the year. Translation adjustments are presented as a

component of shareholders’ equity and minority interests in its con-

solidated financial statements.

(d) Cash equivalents

All highly liquid investments with maturity of three months or less

when purchased are considered cash equivalents.

(e) Inventories

Inventories are stated principally at the lower of cost or market, cost

being determined principally by the first-in, first-out method. See

Note 2 (a).

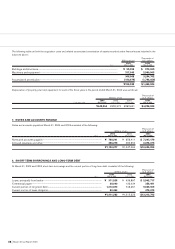

(f) Short-term investments and investment securities

Securities other than equity securities issued by subsidiaries and

affiliates are classified into three categories: trading, held-to-maturity

or other securities. Trading securities are carried at fair value and

held-to-maturity securities are carried at amortized cost. Marketable

securities classified as other securities are carried at fair value with

changes in unrealized holding gain or loss, net of the applicable

income taxes, included directly in shareholders’ equity. Non-

marketable securities classified as other securities are carried at cost.

Cost of securities sold is determined by the moving average method.

(g) Property, plant and equipment and depreciation

Depreciation of property, plant and equipment of the Company and

its consolidated subsidiaries is calculated principally by the straight-

line method based on the estimated useful lives and the residual

value determined by the Company. Significant renewals and addi-

tions are capitalized at cost. Maintenance and repairs are charged to

income.

(h) Leases

Noncancellable lease transactions that transfer substantially all risks

and rewards associated with the ownership of assets are accounted

for as finance leases. All other lease transactions are accounted for

as operating leases and relating payments are charged to income as

incurred. See Note 2(c).

(i) Retirement benefits

Accrued retirement benefits for employees have been provided

mainly at an amount calculated based on the retirement benefit

obligation and the fair value of the pension plan assets as of balance

sheet dates, as adjusted for unrecognized net retirement benefit

obligation at transition, unrecognized actuarial gain or loss, and

unrecognized prior service cost. The retirement benefit obligation is

attributed to each period by the straight-line method over the esti-

mated years of service of the eligible employees. The net retirement

benefit obligation at transition is being amortized principally over a

period of 15 years by the straight-line method.

Actuarial gain and loss are amortized in the year following the year

in which the gain or loss is recognized primarily by the straight-line

method over periods (principally 8 years through 18 years) which are

shorter than the average remaining years of service of the employees.

Certain foreign consolidated subsidiaries have adopted the corridor

approach for the amortization of actuarial gain and loss.

Prior service cost is being amortized as incurred by the straight-

line method over periods (principally 9 years through 15 years)

which are shorter than the average remaining years of service of the

employees.

See Note 9 for the method of accounting for the separation of the

substitutional portion of the benefit obligation from the corporate

portion of the benefit obligation under Welfare Pension Fund Plan.

See Note 2(b) for adoption of a new accounting standard by a

consolidated subsidiary in the United Kingdom.

(j) Income taxes

Deferred tax assets and liabilities have been recognized in the con-

solidated financial statements with respect to the differences

between financial reporting and the tax bases of the assets and lia-

bilities, and were measured using the enacted tax rates and laws

which will be in effect when the differences are expected to reverse.