Neiman Marcus 2006 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2006 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

|

|

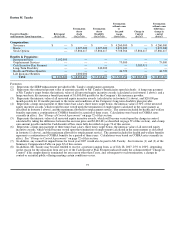

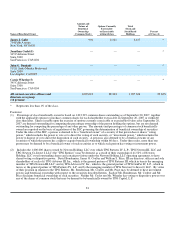

203 restricts "business combinations" between a corporation and "interested stockholders," generally defined as stockholders owning

15% or more of the voting stock of a corporation.

Management Stockholders' Agreement

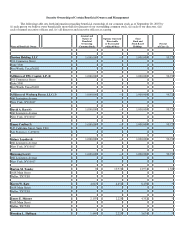

Subject to the Management Stockholders' Agreement, certain members of management, including Burton M. Tansky, Karen

W. Katz, James E. Skinner, Brendan L. Hoffman, and James J. Gold, along with 22 other members of management, elected to invest

in the Company by contributing cash or equity interests in NMG, or a combination of both, to the Company prior to the merger and

receiving equity interests in the Company in exchange therefor immediately after completion of the merger pursuant to rollover

agreements with NMG and the Company entered into prior to the effectiveness of the merger. The aggregate amount of this

investment was approximately $25.6 million. The Management Stockholders' Agreement creates certain rights and restrictions on

these equity interests, including transfer restrictions and tag-along, drag-along, put, call and registration rights in certain

circumstances.

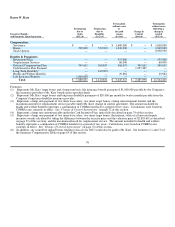

ITEM 14. PRINCIPAL ACCOUNTING FEES AND SERVICES

The Audit Committee has adopted policies and procedures for pre-approving all audit and permissible non-audit services

performed by our independent registered public accounting firm. Under these policies, the Audit Committee pre-approves the use of audit

and audit-related services following approval of the independent registered public accounting firm's audit plan. All services detailed in the

audit plan are considered pre-approved. If, during the course of the audit, the independent registered public accounting firm expects fees

to exceed the approved fee estimate between 10 percent and 15 percent, those fees must be pre-approved in advance by the Audit

Committee Chairman. If fees are expected to exceed the approved estimate by more than 15 percent, those fees must be approved in

advance by the Audit Committee.

Other non-audit services of less than $50,000 that are not restricted services may be pre-approved by both the chief financial

officer and the controller, provided those services will not impair the independence of the independent auditor. These services will be

considered approved by the Audit Committee, provided those projects are discussed with the Audit Committee at its next scheduled

meeting. Services between $50,000 and $100,000 in estimated fees must be pre-approved by the Chairman of the Audit Committee,

acting on behalf of the entire Audit Committee. Services of greater than $100,000 in estimated fees must be pre-approved by the Audit

Committee. All fee overruns will be discussed with the Audit Committee at the next scheduled meeting.

Principal Accounting Fees and Services

On March 19, 2007, we dismissed Deloitte & Touche LLP as our independent registered public accounting firm and appointed

Ernst & Young LLP in its place. In the discussion that follows, figures related to fiscal year 2007 reflect the combined billings of both

firms.

Audit Fees. The aggregate fees billed for the audits of the Company's annual financial statements for the fiscal years ended

July 28, 2007 and July 29, 2006 and for the reviews of the financial statements included in our Quarterly Reports on Form 10-Q were

$1,718,000 and $1,957,000, respectively.

Audit-Related Fees. The aggregate fees billed for audit-related services for the fiscal years ended July 28, 2007 and July 29,

2006 were $160,000 and $1,008,000, respectively. These fees related to accounting research and consultation and attestation services for

certain subsidiary companies for the fiscal years ended July 28, 2007 and July 29, 2006.

Tax Fees. The aggregate fees billed for tax services for the fiscal years ended July 28, 2007 and July 29, 2006 were $344,000

and $83,000, respectively. These fees related to tax compliance and planning for the fiscal years ended July 28, 2007 and July 29, 2006.

The Audit Committee has considered and concluded that the provision of permissible non-audit services is compatible with

maintaining our independent registered public accounting firm's independence.

84