Neiman Marcus 2006 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2006 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

|

|

The Retirement Plan is a funded, tax-qualified pension plan. Most non-union employees over age 21 who have completed

one year of service with 1,000 or more hours participate in the Retirement Plan, which pays benefits upon retirement or termination of

employment. The Retirement Plan is a "career-accumulation" plan, under which a participant earns each year a retirement annuity

equal to 1 percent of his or her compensation for the year up to the Social Security wage base and 1.5 percent of his or her

compensation for the year in excess of such wage base. Benefits under the Retirement Plan become fully vested after five years of

service with us.

The SERP is an unfunded, nonqualified plan under which benefits are paid from our general assets to supplement Retirement

Plan benefits and Social Security. Executive, administrative and professional employees (other than those employed as salespersons)

with an annual base salary at least equal to a minimum established by the Company ($160,000 as of July 28, 2007) are eligible to

participate. At normal retirement age (age 65), a participant with 25 or more years of service is entitled to payments under the SERP

sufficient to bring his or her combined annual benefit from the Retirement Plan and SERP, computed as a straight life annuity, up to

50 percent of the participant's highest consecutive 60 month average of annual pensionable earnings, less 60 percent of his or her

estimated annual primary Social Security benefit. If the participant has fewer than 25 years of service, the combined benefit is

proportionately reduced. Benefits under the SERP become fully vested after five years of service with us. The SERP is designed to

comply with the requirements of Section 409A of the Internal Revenue Code.

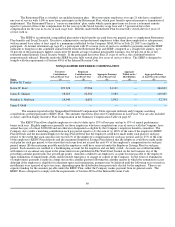

NONQUALIFIED DEFERRED COMPENSATION

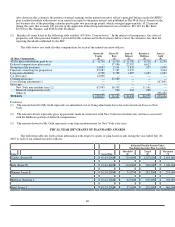

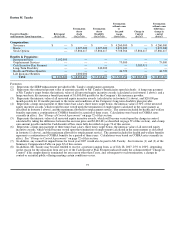

Name

Executive

Contributions

in Last Fiscal Year

($)

Registrant

Contributions in

Last Fiscal Year

($)

Aggregate Earnings

in Last Fiscal Year

($)

Aggregate

Withdrawals /

Distributions

($)

Aggregate Balance

at Last Fiscal Year-End

($)

Burton M. Tansky — — — — —

Karen W. Katz 223,678 37,986 24,101 — 360,631

James E. Skinner 58,283 22,392 7,082 — 109,067

Brendan L. Hoffman 14,949 6,625 1,993 — 32,794

James J. Gold — — — — —

The amounts reported in the Nonqualified Deferred Compensation Table represent deferrals and Company matching

contributions credited pursuant to KEDC Plan. The amounts reported as Executive Contributions in Last Fiscal Year are also included

as Salary and Non-Equity Incentive Plan Compensation in the Summary Compensation Table on page 65.

The KEDC Plan allows eligible employees to elect to defer up to 15% of base pay and up to 15% of annual performance

bonus each year. Eligible employees generally are those employees who have completed one year of service with the Company, have

annual base pay of at least $300,000 and are otherwise designated as eligible by the Company's employee benefits committee. The

Company also credits a matching contribution each pay period equal to (A) the sum of (i) 100% of the sum of the employee's KEDC

Plan deferrals and the maximum Employee Savings Plan deferral that the employee could have made under such plan for such pay

period, to the extent that such sum does not exceed 2% of the employee's compensation for such pay period, and (ii) 25% of the sum

of the employee's KEDC Plan deferrals and the maximum Employee Savings Plan deferral that the employee could have made under

such plan for such pay period, to the extent that such sum does not exceed the next 4% of the employee's compensation for such pay

period, minus (B) the maximum possible match the employee could have received under the Employee Savings Plan for such pay

period. Such amounts are credited to a bookkeeping account for the employee and are fully vested. Accounts are credited monthly

with interest at an annual rate equal to the prime interest rate published in The Wall Street Journal on the last business day of the

preceding calendar quarter plus two percentage points. Amounts credited to an employee's account become payable to the employee

upon termination of employment, death, unforeseeable emergency or change of control of the Company. In the event of termination

of employment, payment is made in a lump sum in the calendar quarter following the calendar quarter in which the termination occurs

although if the employee is eligible for retirement upon such termination, payment may be deferred until the following year or made in

installments over a period of up to ten years, depending upon the distribution form previously elected by the employee. There is no

separate funding for the amounts payable under the KEDC Plan, rather the Company makes payment from its general assets. The

KEDC Plan is designed to comply with the requirements of Section 409A of the Internal Revenue Code.

69