Motorola 2013 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2013 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

78

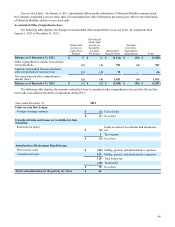

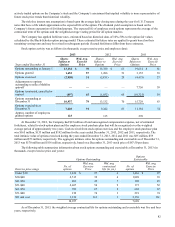

The status of the Company’s plans are as follows:

U.S. Pension Benefit

Plans Non U.S. Pension

Benefit Plans

Postretirement

Health Care Benefits

Plan

2013 2012 2013 2012 2013 2012

Change in benefit obligation:

Benefit obligation at January 1 $ 8,288 $ 6,986 $ 1,787 $ 1,588 $ 322 $ 450

Service cost — — 12 10 2 3

Interest cost 352 349 70 75 11 16

Plan amendments —————(151)

Actuarial loss (gain) (1,012) 1,277 95 103 (37) 24

Foreign exchange valuation adjustment ——3048——

Employee contributions — — 2 2 — —

Benefit payments (311)(324)(41)(39)(20)(20)

Benefit obligation at December 31 7,317 8,288 1,955 1,787 278 322

Change in plan assets:

Fair value at January 1 5,426 4,747 1,362 1,219 155 155

Return on plan assets 806 660 199 111 22 20

Company contributions 150 340 32 31 — —

Employee contributions — — 2 2 — —

Foreign exchange valuation adjustment ——1438——

Benefit payments from plan assets (311)(321)(41)(39)(16)(20)

Fair value at December 31 6,071 5,426 1,568 1,362 161 155

Funded status of the plan (1,246)(2,862)(387)(425)(117)(167)

Unrecognized net loss 2,732 4,313 492 520 143 206

Unrecognized prior service benefit — — (44)(51)(92)(135)

Prepaid (accrued) pension cost $ 1,486 $ 1,451 $ 61 $ 44 $ (66) $ (96)

Components of prepaid (accrued) pension cost:

Non-current benefit liability $(1,246) $ (2,862) $ (387) $ (425) $ (117) $ (167)

Deferred income taxes 1,002 1,592 33 41 19 26

Accumulated other comprehensive loss 1,730 2,721 415 428 32 45

Prepaid (accrued) pension cost $ 1,486 $ 1,451 $ 61 $ 44 $ (66) $ (96)

The benefit obligation and plan assets for the Company's plans are measured as of December 31, 2013. The Company

utilizes a five-year, market-related asset value method of recognizing asset related gains and losses.

Prior to 2013, unrecognized gains and losses were amortized over periods ranging from three to thirteen years. At the

close of fiscal 2012, the Company determined that the majority of the Company's plan participants in its Regular and United

Kingdom pension plans were no longer actively employed by the Company due to significant employee exits as a result of the

Company's recent divestitures. Under relevant accounting rules, when almost all of the plan participants are considered

inactive, the amortization period for certain unrecognized losses changes from the average remaining service period to the

average remaining lifetime of the participant. As such, beginning in 2013, and depending on the specific plan, the Company

began amortizing gains and losses over periods ranging from five to twenty-eight years. Prior service costs are being amortized

over periods ranging from ten to twelve years. Benefits under all pension plans are valued based on the projected unit credit

cost method.

The net periodic cost for 2014 will include amortization of the unrecognized net loss and prior service costs for the U.S.

Pension Benefit Plans and Non U.S. Pension Benefit Plans, currently included in Accumulated other comprehensive loss, of

$91 million and $5 million, respectively. It is estimated that the 2014 net periodic expense for the Postretirement Health Care

Benefits Plan will include amortization of a net credit of $31 million, comprised of the unrecognized prior service gain and

unrecognized actuarial loss, currently included in Accumulated other comprehensive loss.