Microsoft 2011 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2011 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

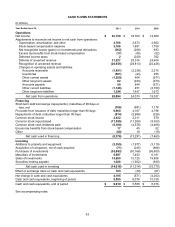

|

|

53

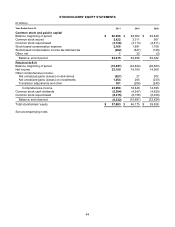

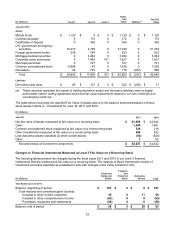

Less than 12 Months 12 Months or Greater Total Total

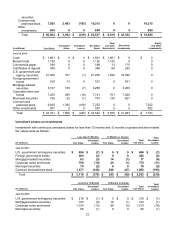

Common and preferred stock 2,102 (339) 190 (79) 2,292 (418)

Total $ 3,613 $ (360) $ 297 $ (85) $ 3,910 $ (445)

Unrealized losses from fixed-income securities are primarily attributable to changes in interest rates. Unrealized

losses from domestic and international equities are due to market price movements. Management does not

believe any remaining unrealized losses represent other-than-temporary impairments based on our evaluation of

available evidence as of June 30, 2011.

At June 30, 2011 and 2010, the recorded bases and estimated fair values of common and preferred stock and

other investments that are restricted for more than one year or are not publicly traded were $334 million and $216

million, respectively.

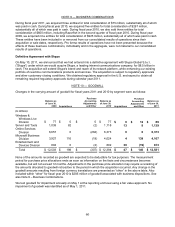

Debt Investment Maturities

(In millions) Cost Basis

Estimated

Fair Value

June 30, 2011

Due in one year or less $ 23,982 $ 24,053

Due after one year through five years 19,516 19,733

Due after five years through 10 years 2,516 2,637

Due after 10 years 2,811 2,945

Total $ 48,825 $ 49,368

NOTE 5 — DERIVATIVES

We use derivative instruments to manage risks related to foreign currencies, equity prices, interest rates, and

credit; to enhance investment returns; and to facilitate portfolio diversification. Our objectives for holding

derivatives include reducing, eliminating, and efficiently managing the economic impact of these exposures as

effectively as possible. Our derivative programs include strategies that both qualify and do not qualify for hedge

accounting treatment. All notional amounts presented below are measured in U.S. currency equivalents.

Foreign Currency

Certain forecasted transactions, assets, and liabilities are exposed to foreign currency risk. We monitor our

foreign currency exposures daily to maximize the economic effectiveness of our foreign currency hedge positions.

Option and forward contracts are used to hedge a portion of forecasted international revenue for up to three years

in the future and are designated as cash-flow hedging instruments. Principal currencies hedged include the euro,

Japanese yen, British pound, and Canadian dollar. As of June 30, 2011 and 2010, the total notional amounts of

these foreign exchange contracts sold were $10.6 billion and $9.3 billion, respectively. Foreign currency risks

related to certain non-U.S. dollar denominated securities are hedged using foreign exchange forward contracts

that are designated as fair-value hedging instruments. As of June 30, 2011 and 2010, the total notional amounts

of these foreign exchange contracts sold were $572 million and $523 million, respectively. Certain options and

forwards not designated as hedging instruments are also used to manage the variability in exchange rates on

accounts receivable, cash, and intercompany positions, and to manage other foreign currency exposures. As of

June 30, 2011, the total notional amounts of these foreign exchange contracts purchased and sold were $3.9

billion and $7.3 billion, respectively. As of June 30, 2010, the total notional amounts of these foreign exchange

contracts purchased and sold were $7.8 billion and $5.3 billion, respectively.

Equity

Securities held in our equity and other investments portfolio are subject to market price risk. Market price risk is

managed relative to broad-based global and domestic equity indices using certain convertible preferred

investments, options, futures, and swap contracts not designated as hedging instruments. From time to time, to

hedge our price risk, we may use and designate equity derivatives as hedging instruments, including puts, calls,

swaps, and forwards. As of June 30, 2011, the total notional amounts of designated and non-designated equity

contracts purchased and sold were $1.4 billion and $935 million, respectively. As of June 30, 2010, the total

notional amounts of designated and non-designated equity contracts purchased and sold were $918 million and

$472 million, respectively.