Microsoft 2011 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2011 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|

48

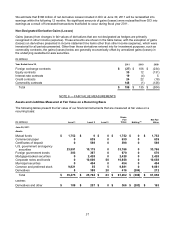

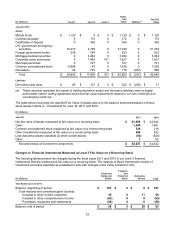

Our current financial liabilities have fair values that approximate their carrying values. Our long-term financial

liabilities consist of long-term debt which is recorded on the balance sheet at issuance price less unamortized

discount.

Financial Instruments

We consider all highly liquid interest-earning investments with a maturity of three months or less at the date of

purchase to be cash equivalents. The fair values of these investments approximate their carrying values. In

general, investments with original maturities of greater than three months and remaining maturities of less than

one year are classified as short-term investments. Investments with maturities beyond one year may be classified

as short-term based on their highly liquid nature and because such marketable securities represent the

investment of cash that is available for current operations. All cash equivalents and short-term investments are

classified as available-for-sale and realized gains and losses are recorded using the specific identification

method. Changes in market value, excluding other-than-temporary impairments, are reflected in OCI.

Equity and other investments classified as long-term include both debt and equity instruments. Debt and publicly-

traded equity securities are classified as available-for-sale and realized gains and losses are recorded using the

specific identification method. Changes in market value, excluding other-than-temporary impairments, are

reflected in OCI. Common and preferred stock and other investments that are restricted for more than one year or

are not publicly traded are recorded at cost or using the equity method.

We lend certain fixed-income and equity securities to increase investment returns. The loaned securities continue

to be carried as investments on our balance sheet. Cash and/or security interests are received as collateral for

the loan securities with the amount determined based upon the underlying security lent and the creditworthiness

of the borrower. Cash received is recorded as an asset with a corresponding liability.

Investments are considered to be impaired when a decline in fair value is judged to be other-than-temporary. Fair

value is calculated based on publicly available market information or other estimates determined by management.

We employ a systematic methodology on a quarterly basis that considers available quantitative and qualitative

evidence in evaluating potential impairment of our investments. If the cost of an investment exceeds its fair value,

we evaluate, among other factors, general market conditions, credit quality of debt instrument issuers, the

duration and extent to which the fair value is less than cost, and for equity securities, our intent and ability to hold,

or plans to sell, the investment. For fixed-income securities, we also evaluate whether we have plans to sell the

security or it is more likely than not that we will be required to sell the security before recovery. We also consider

specific adverse conditions related to the financial health of and business outlook for the investee, including

industry and sector performance, changes in technology, and operational and financing cash flow factors. Once a

decline in fair value is determined to be other-than-temporary, an impairment charge is recorded to other income

(expense) and a new cost basis in the investment is established.

Derivative instruments are recognized as either assets or liabilities and are measured at fair value. The

accounting for changes in the fair value of a derivative depends on the intended use of the derivative and the

resulting designation.

For a derivative instrument designated as a fair-value hedge, the gain (loss) is recognized in earnings in the

period of change together with the offsetting loss or gain on the hedged item attributed to the risk being hedged.

For options designated as fair-value hedges, changes in the time value are excluded from the assessment of

hedge effectiveness and are recognized in earnings.

For derivative instruments designated as cash-flow hedges, the effective portion of the derivative’s gain (loss) is

initially reported as a component of OCI and is subsequently recognized in earnings when the hedged exposure is

recognized in earnings. For options designated as cash-flow hedges, changes in the time value are excluded from

the assessment of hedge effectiveness and are recognized in earnings. Gains (losses) on derivatives

representing either hedge components excluded from the assessment of effectiveness or hedge ineffectiveness

are recognized in earnings.

For derivative instruments that are not designated as hedges, gains (losses) from changes in fair values are

primarily recognized in other income (expense). Other than those derivatives entered into for investment

purposes, such as commodity contracts, the gains (losses) are generally economically offset by unrealized gains

(losses) in the underlying available-for-sale securities, which are recorded as a component of OCI until the

securities are sold or other-than-temporarily impaired, at which time the amounts are moved from OCI into other

income (expense).