IBM 1998 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 1998 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

7

information technology services. With its huge current demand,

solid fundamentals underlying future demand and lack of a

dominant competitor, I/ T services has all the earmarks of

a classic growth business.

I believe that IBM is well positioned to win a dispropor-

tionate share of that growth. IBM Global Services has grown in

just eight years from a $4billion to a $24 billion business, with

better than 20 percent annual growth. And its market leader-

ship is increasing, because the 126,000 IBMers who work in

services can draw on all the technology and human assets of

IBM, including an R&D community with a strong record of

innovation (they just marked their sixth straight year of U.S.

patent leadership).

• The PC era is over.

This is not to say that PCs are going to die off, any more

than mainframes vanished when the IBM PC debuted in 1981.

Indeed, IBM’s own PC business was an important turnaround

story in 1998. But the PC’s reign as the driver of customer

buying decisions and the primary platform for application

development is over. In all those respects, it has been sup-

planted by the network.

You experience this every time you go online to buy a

book or trade stock. Where is the transaction executed? Where

is the data managed and stored? Where does the processing

take place? A teeny part is handled by your PC. Most of the

work is done behind the scenes, in the network, by bigger

computer systems.

Businesses deploying network applications have to handle an

exponential increase in the volume of interactions and trans-

actions, and they need to do something useful with the tidal

wave of information generated from those interactions. Both

needs are driving the rediscovery of enterprise computing – that

is, industrial-strength servers and the software that runs on them.

As the Net takes over much of the work previously per-

formed by PCs, we’re seeing another interesting development:

a proliferation of new personal computing devices – personal

digital assistants, Web-enabled TVs, screenphones, smart cards

and a host of products we have yet to imagine. One market

research firm predicts that sales of non-PC Internet devices will

surpass PCs within five years. This explosion of “information

appliances” will bring computing to millions of new users –

perhaps a billion people – faster and more affordably than the

PC could ever have taken us.

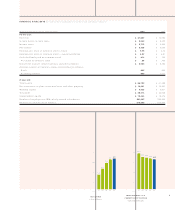

CAPITAL INVESTMENTS

($ in billions)

’94 ’95 ’96 ’97 ’98

3.1

4.7

5.9

6.8 6.5

NUMBER OF ACQUISITIONS

’94 ’95 ’96 ’97 ’98

3

10

18

12

15