IBM 1998 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 1998 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

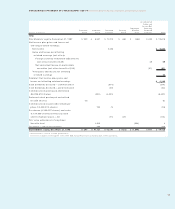

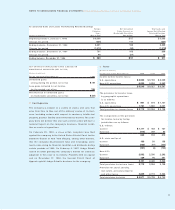

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS International Business Machines Corporation and Subsidiary Companies

71

BAccounting Changes

Standards Implemented

The company implemented new accounting standards in

1998, 1997 and 1996. None of these standards had a mater-

ial effect on the financial position or results of operations of

the company.

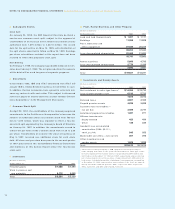

Beginning with the first quarter of 1998, the company adopted

SFAS 130, “Reporting Comprehensive Income,” which estab-

lished standards for reporting and displaying comprehensive

income and its components. The disclosures required by

SFAS 130 are presented in the Accumulated gains and losses

not affecting retained earnings section in the Consolidated

Statement of Stockholders’ Equity on pages 66 and 67 and in

note O, “Stockholders’ Equity Activity,” on pages 76 and 77.

Effective December 31, 1998, the company adopted SFAS 131,

“Disclosures About Segments of an Enterprise and Related

Information,” which establishes standards for reporting oper-

ating segments and disclosures about products and services,

geographic areas and major customers. See note Y, “Segment

Information,” on pages 84 through 89 for further information.

Effective December 31, 1998, the company adopted SFAS

132, “Employers’ Disclosures about Pensions and Other

Postretirement Benefits,” which established expanded disclo-

sures for defined benefit pension and postretirement benefit

plans. See note W, “Retirement Plans,” on pages 81 through 83

and note X, “Nonpension Postretirement Benefits” on pages 83

and 84 for the required disclosures.

On January 1, 1998, the company adopted the American

Institute of Certified Public Accountants Statement of Position

(SOP) 97-2, “Software Revenue Recognition.” This SOP pro-

vides guidance on revenue recognition for software transac-

tions. It requires deferral of some or all of the revenue related

to a specific contract depending on the existence of vendor-

specific objective evidence and the ability to allocate the total

fee to all elements within the contract. The portion of the fee

allocated to an element is recognized as revenue when all of

the revenue recognition criteria have been met for that element.

In December 1997, the company implemented SFAS 128,

“Earnings Per Share” (EPS). This standard prescribes the meth-

ods for calculating basic and diluted EPS and requires dual

presentation of these amounts on the face of the earnings

statement. No restatement of EPS, for either basic or diluted,

was required for amounts reported previously in the company’s

filings with the U.S. Securities and Exchange Commission.

Effective January 1, 1997, the company implemented SFAS 125,

“Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities.” This standard provides account-

ing and reporting standards for transfers and servicing of finan-

cial assets and extinguishments of liabilities. The company was

generally in compliance with this standard prior to adoption.

In 1996, the company adopted SOP 96-1, “Environmental

Remediation Liabilities.” This SOP provides guidance on the

recognition, measurement, display and disclosure of environ-

mental remediation liabilities. See note N, “Other Liabilities

and Environmental,” on page 76 for further information. The

company was generally in compliance with this standard prior

to adoption.

In 1996, the company implemented the disclosure-only provi-

sions of SFAS 123, “Accounting for Stock-Based Compensa-

tion.” See note V, “Stock-Based Compensation Plans,” on

pages 79 through 81 for further information.

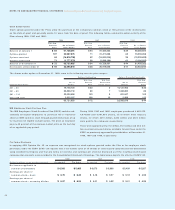

New Standards to be Implemented

In June 1998, the Financial Accounting Standards Board issued

SFAS 133, “Accounting for Derivative Instruments and Hedging

Activities.” This statement establishes accounting and report-

ing standards for derivative instruments. It requires an entity to

recognize all derivatives as either assets or liabilities in the

Statement of Financial Position and measure those instru-

ments at fair value. Additionally, the fair value adjustments will

impact either stockholders’ equity or net income depending

on whether the derivative instrument qualifies as a hedge and,

if so, the nature of the hedging activity. The company will

adopt this new standard as of January 1, 2000. Management

does not expect the adoption to have a material impact on the

company’s results of operations, however, the impact on the

company’s financial position is dependent upon the fair values

of the company’s derivatives and related financial instruments

at the date of adoption.

During 1998, the American Institute of Certified Public

Accountants issued SOP 98-1, “Accounting for the Costs of

Computer Software Developed or Obtained for Internal Use.”

The statement requires the capitalization of internal use com-

puter software costs if certain criteria are met. The capitalized

software costs will be amortized on a straight-line basis over

the useful life of the software. The company will adopt the

statement as of January 1, 1999. The adoption of the state-

ment is not expected to have a material impact on the com-

pany’s financial statements.