IBM 1998 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 1998 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

59

MANAGEMENT DISCUSSION International Business Machines Corporation and Subsidiary Companies

Poor’s upgraded its credit ratings for the company and its

rated subsidiaries’ senior long-term debt to A+ from A, and on

IBM’s preferred stock to A from A-. They also affirmed the

commercial paper rating at A-1.

Moody’s Investors Service rates the senior long-term debt of

the company and its rated subsidiaries as A1, the commercial

paper as Prime-1, and the company’s preferred stock as “a1.”

Fitch Investors Service rates the company and its rated sub-

sidiaries’ senior long-term debt as AA-, commercial paper as

F-1+, and preferred stock as A+.

Duff & Phelps rates the company and its rated subsidiaries’

senior long-term debt as A+, commercial paper as Duff 1, and

the company’s preferred stock as A.

Cash Flows

The company’s cash flows from operating, investing and financ-

ing activities, as prescribed by generally accepted accounting

principles and reflected in the Consolidated Statement of

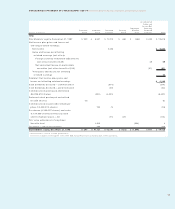

Cash Flows on page 68, are summarized in the following table:

(Dollars in millions) 1998 1997 1996

Net cash provided from

(used in):

Operating activities $««9,273 $«««8,865 $«10,275

Investing activities (6,131) (6,155) (5,723)

Financing activities (4,993) (3,090) (3,952)

Effect of exchange rate

changes on cash and

cash equivalents 120 (201) (172)

Net change in cash and

cash equivalents $«(1,731) $«««««(581) $÷÷÷428

WORKING CAPITAL

(Dollars in millions)

At December 31: 1998 1997

Current assets $«42,360 $«40,418

Current liabilities 36,827 33,507

Working capital $÷«5,533 $«««6,911

Current ratio 1.15:1 1.21:1

Current assets increased $1.9 billion, driven primarily by

increases in accounts receivable relative to strong year-end

global financing volumes and in prepaid expenses due to

increases in net deferred tax assets. The company ended 1998

with inventories of $5.2 billion, near last year’s levels which

were the lowest since 1983, due to continued focus on inven-

tory management process improvements, notably in the Per-

sonal Systems segment. These improvements have enabled

the company’s inventory turn rate to increase from 4.9 in 1997

to 5.3 in 1998.

Current liabilities increased $3.3 billion from year-end 1997

with increases of $0.7 billion in taxes payable, $0.7 billion in

short-term debt and $1.9 billion in other current liabilities

(increases in accounts payable ($1.0 billion), compensation

and benefits ($0.5 billion), and deferred income ($0.7 billion),

and a $0.3 billion decrease in other accrued expenses and

liabilities). The increase in taxes payable primarily reflects

improvements in the company’s operating results in certain

geographies. Short-term debt essentially increased to support

the growth of global financing assets. The increase in other

current liabilities was primarily attributable to the effect of cur-

rency rate translation ($1.0 billion) on non-U.S. balances, and

by considerable year-end business activity relative to deferred

income, mainly advanced billings for software.

Investments

The company’s investments for plant, rental machines and

other property were $6.5 billion for 1998, a decrease of $0.3 bil-

lion from 1997. The company continues to invest significantly

in its rapidly growing services business, principally in the

management of customers’ information technology, and in

manufacturing capacity for HDDs and microelectronics.

In addition to software development expenses included in

Research, development and engineering, the company capital-

ized $0.3 billion of software costs during both 1998 and 1997.

Amortization of capitalized software costs amounted to

$0.5 billion for 1998, a decrease of $0.5 billion from 1997. This

decrease in the level of costs amortized is a result of more

software spending being expensed in the period incurred, and

less being capitalized in relation to historical levels.

Investments and sundry assets were $23.5 billion at the end of

1998, an increase of $1.6 billion from 1997, primarily the result

of increases in prepaid pension assets and non-current cus-

tomer loan receivables. See note H, “Investments and Sundry

Assets,” on page 72 for additional information.

DEBT AND EQUITY

(Dollars in millions) 1998 1997

Non-global financing debt $÷«1,659 $«««3,102

Global financing debt 27,754 23,824

Total debt $«29,413 $«26,926

Stockholders’ equity $«19,433 $«19,816

Debt /capitalization 60.2% 57.6%

EBITDA/interest expense 8x 8x

Non-global financing:

Debt /capitalization 9.9% 16.1%

EBITDA/interest expense 15x 14x

Global financing debt /equity 6.5:1 6.5:1