IBM 1998 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 1998 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

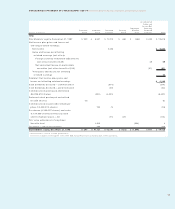

Total debt increased $2.5 billion from year-end 1997, driven by

an increase of $3.9 billion in debt to support the growth in

global financing assets, offset by a $1.4 billion decrease in

debt not related to the Global Financing segment.

Stockholders’ equity declined $0.4 billion to $19.4 billion at

December 31, 1998. The company’s ongoing stock repurchas-

ing program (see note O, “Stockholders’ Equity Activity,” on

pages 76 and 77) basically offset the $6.3 billion of net income

for the year.

Non-global financing earnings before interest and taxes plus

depreciation and amortization (EBITDA) to non-global financ-

ing interest expense, adjusted for future gross minimum rental

commitments, was 15x and 14x in 1998 and 1997, respectively.

While the company does not calculate EBITDA on a segment

basis, it is a useful indicator of the company’s ability to service

its debt.

Currency Rate Fluctuations

The company’s results are affected by changes in the relative

values of non-U.S. currencies to the U.S. dollar. At December 31,

1998, currency changes resulted in assets and liabilities

denominated in local currencies being translated into more dol-

lars. The currency rate changes also resulted in an unfavorable

impact on revenue of approximately 2 percent, 5 percent and

3 percent, respectively, in 1998, 1997 and 1996.

In high-inflation environments, translation adjustments are

reflected in period income, as required by SFAS 52, “Foreign

Currency Translation.” Generally, the company limits currency

risk in these countries by linking prices and contracts to U.S.

dollars, by financing operations locally and through foreign

currency hedge contracts.

The company uses a variety of financial hedging instruments

to limit specific currency risks related to global financing trans-

actions and the repatriation of dividends and royalties. Fur-

ther discussion on currency and hedging appears in note M,

“Financial Instruments,” on pages 74 and 75.

Market Risk

In the normal course of business, the financial position of the

company is routinely subjected to a variety of risks. In addition

to the market risk associated with interest rate and currency

movements on outstanding debt and non-U.S. dollar denomi-

nated assets and liabilities, other examples of risk include col-

lectibility of accounts receivable and recoverability of residual

values on leased assets.

The company regularly assesses these risks and has established

policies and business practices to protect against the adverse

effects of these and other potential exposures. As a result, the

company does not anticipate any material losses in these areas.

The company’s debt in support of the global financing busi-

ness and the geographic breadth of the company’s operations

contain an element of market risk from changes in interest and

currency rates. The company manages this risk, in part,

through the use of a variety of financial instruments including

derivatives, as explained in note M, “Financial Instruments,”

on pages 74 and 75.

For purposes of specific risk analysis, the company uses

sensitivity analysis to determine the impact that market risk

exposures may have on the fair values of the company’s debt

and other financial instruments.

The financial instruments included in the sensitivity analysis

consist of all of the company’s cash and cash equivalents,

marketable securities, long-term non-lease receivables,

investments, long-term and short-term debt and all derivative

financial instruments. Interest rate swaps, interest rate options,

foreign currency swaps, forward contracts and foreign cur-

rency option contracts constitute the company’s portfolio of

derivative financial instruments.

To perform sensitivity analysis, the company assesses the risk

of loss in fair values from the impact of hypothetical changes in

interest rates and foreign currency exchange rates on market

sensitive instruments. The market values for interest and foreign

currency exchange risk are computed based on the present

value of future cash flows as impacted by the changes in rates

attributable to the market risk being measured. The discount

rates used for the present value computations were selected

based on market interest and foreign currency exchange rates

in effect at December 31, 1998 and 1997. The differences in this

comparison are the hypothetical gains or losses associated

with each type of risk.

Information provided by the model used does not necessarily

represent the actual changes in fair value that the company

would incur under normal market conditions because, of

necessity, all variables other than the specific market risk fac-

tor are held constant. In addition, the model is constrained by

the fact that certain items are specifically excluded from the

analysis while the financial instruments relating to the financ-

ing or hedging of those items are included by definition.

Excluded items include leased assets, forecasted foreign cur-

rency cash flows, and the company’s net investment in foreign

operations. As a consequence, reported changes in the values

of some financial instruments impacting the results of the

sensitivity analysis are not matched with the offsetting

changes in the values of the items that those instruments are

designed to finance or hedge.

MANAGEMENT DISCUSSION International Business Machines Corporation and Subsidiary Companies

60