Frontier Communications 2004 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2004 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

|

|

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

Notes to Consolidated Financial Statements

F-38

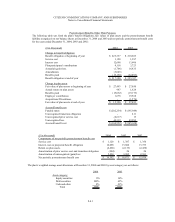

The expected long-term rate of return on plan assets is based on an asset allocation assumption of 30% to 45% in fixed

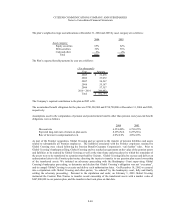

income securities and 55% to 70% in equity securities. We review our asset allocation at least annually and make

changes when considered appropriate. In 2004, we did not change our expected long-term rate of return from the

8.25% used in 2003. Our pension plan assets are valued at actual market value as of the measurement date. The

measurement date used to determine pension and other postretirement benefit measures for the pension plan and the

postretirement benefit plan is December 31.

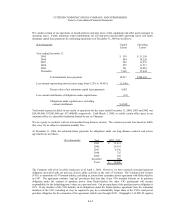

Accounting standards require that Citizens record an additional minimum pension liability when the plan’s

“accumulated benefit obligation” exceeds the fair market value of plan assets at the pension plan measurement (balance

sheet) date. In the fourth quarter of 2003, due to strong performance in the equity markets during 2003, partially offset

by a decrease in the year-end discount rate, the Company recorded a reduction to its minimum pension liability in the

amount of $34,935,000 with a corresponding credit to shareholders’ equity of $21,562,000, net of taxes of $13,373,000.

In the fourth quarter of 2004, mainly due to a decrease in the year-end discount rate, the Company recorded an

additional minimum pension liability in the amount of $17,372,000 with a corresponding charge to shareholders’ equity

of $10,727,000, net of taxes of $6,645,000. These adjustments did not impact our earnings or cash flows for either year.

If discount rates and the equity markets performance decline, the Company would be required to increase its minimum

pension liabilities and record additional charges to shareholder’s equity in the future.

Actual results that differ from our assumptions are added or subtracted to our balance of unrecognized actuarial gains

and losses. For example, if the year-end discount rate used to value the plan’s projected benefit obligation decreases

from the prior year-end, then the plan’s actuarial loss will increase. If the discount rate increases from the prior year-end

then the plan’s actuarial loss will decrease. Similarly, the difference generated from the plan’s actual asset performance

as compared to expected performance would be included in the balance of unrecognized gains and losses.

The impact of the balance of accumulated actuarial gains and losses are recognized in the computation of pension cost

only to the extent this balance exceeds 10% of the greater of the plan’s projected benefit obligation or market value of

plan assets. If this occurs, that portion of gain or loss that is in excess of 10% is amortized over the estimated future

service period of plan participants as a component of pension cost. The level of amortization is affected each year by

the change in actuarial gains and losses and could potentially be eliminated if the gain/loss activity reduces the net

accumulated gain/loss balance to a level below the 10% threshold.

Effective February 1, 2003, the pension plan was frozen for all non-union plan participants. The vested benefit earned

through that date is protected by law and will be available upon retirement. No additional benefit accruals for service

will occur after February 1, 2003 for those participants.