Frontier Communications 2004 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2004 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

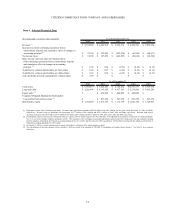

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

24

New Accounting Pronouncements

Goodwill and Other Intangibles

In July 2001, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards (SFAS)

No. 142, “Goodwill and Other Intangible Assets.” This statement requires that goodwill and other intangibles with indefinite

useful lives no longer be amortized to earnings, but instead be reviewed for impairment. We have no intangibles with

indefinite useful lives other than goodwill and trade name. The amortization of goodwill and trade name ceased upon

adoption of the statement on January 1, 2002. We were required to test for impairment of goodwill and other intangibles with

indefinite useful lives as of January 1, 2002 and at least annually thereafter. Any transitional impairment loss at January 1,

2002 was recognized as the cumulative effect of a change in accounting principle in our statement of operations. As a result

of our adoption of SFAS No. 142, we recognized a transitional impairment loss related to ELI of $39.8 million as a

cumulative effect of a change in accounting principle in our statement of operations in 2002. We annually examine the

carrying value of our goodwill and other intangibles with estimated useful lives to determine whether there are any

impairment losses and have determined for the year ended December 31, 2004 that there was no impairment.

SFAS No. 142 also requires that intangible assets with estimated useful lives be amortized over those lives and be reviewed

for impairment in accordance with SFAS No. 144, “Accounting for Impairment or Disposal of Long-Lived Assets.” We

reassess the useful life of our intangible assets with estimated useful lives annually. The impact of the adoption of SFAS No.

142 is discussed in Note 2 to Consolidated Financial Statements.

Accounting for Asset Retirement Obligations

In June 2001, the FASB issued SFAS No. 143, “Accounting for Asset Retirement Obligations.” SFAS No. 143 applies to

fiscal years beginning after June 15, 2002, and addresses financial accounting and reporting obligations associated with the

retirement of tangible long-lived assets and the associated asset retirement costs. We adopted SFAS No. 143 effective

January 1, 2003. The standard applies to legal obligations associated with the retirement of long-lived assets that result from

acquisition, construction, development or normal use of the assets and requires that a legal liability for an asset retirement

obligation be recognized when incurred, recorded at fair value and classified as a liability in the balance sheet. When the

liability is initially recorded, the entity will capitalize the cost and increase the carrying value of the related long-lived asset.

The liability is then accreted to its present value each period and the capitalized cost is depreciated over the estimated useful

life of the related asset. At the settlement date, the entity will settle the obligation for its recorded amount or recognize a gain

or loss upon settlement.

Depreciation expense for our wireline operations had historically included an additional provision for cost of removal.

Effective with the adoption of SFAS No. 143, on January 1, 2003, the Company ceased recognition of the cost of removal

provision in depreciation expense and eliminated the cumulative cost of removal included in accumulated depreciation, as the

Company has no legal obligation to remove certain long-lived assets. The cumulative effect of retroactively applying these

changes to periods prior to January 1, 2003, resulted in an after tax non-cash gain of approximately $65.8 million recognized

in 2003.

Long-Lived Assets

In October 2001, the FASB issued SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets.” This

statement establishes a single accounting model, based on the framework established in SFAS No. 121, for impairment of

long-lived assets held and used and for long-lived assets to be disposed of by sale, whether previously held and used or newly

acquired, and broadens the presentation of discontinued operations to include more disposal transactions. We adopted this

statement on January 1, 2002.

Debt Retirement

In April 2002, the FASB issued SFAS No. 145, “Rescission of FASB Statements No. 4, 44, and 64, Amendment of FASB

Statement No. 13, and Technical Corrections.” This statement eliminates the requirement that gains and losses from

extinguishment of debt be aggregated and, if material, classified as an extraordinary item, net of related income tax effect. The

statement requires gains and losses from extinguishment of debt to be classified as extraordinary items only if they meet the

criteria in Accounting Principles Board Opinion No. 30, “Reporting the Results of Operations – Reporting the Effects of Disposal

of a Segment of a Business, and Extraordinary, Unusual and Infrequently Occurring Events and Transactions” which provides