Frontier Communications 2004 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2004 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

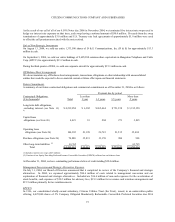

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

25

guidance for distinguishing transactions that are part of an entity’s recurring operations from those that are unusual or infrequent

or that meet the criteria for classification as an extraordinary item. We adopted SFAS No. 145 in the second quarter of 2002.

During the year ended December 31, 2004 and 2003, we recognized $66.5 million and $10.9 million, respectively, of losses from

the early retirement of debt. During the year ended December 31, 2002, we recognized $5.6 million of gains from early debt

retirement. In addition, for the year ended December 31, 2002, we recognized a $12.8 million loss due to a tender offer

related to certain debt securities. These gains/losses were recorded in other income (loss), net.

Exit or Disposal Activities

In June 2002, the FASB issued SFAS No. 146, “Accounting for Costs Associated with Exit or Disposal Activities,” which

nullified Emerging Issues Task Force (EITF) Issue No. 94-3, “Liability Recognition for Certain Employee Termination

Benefits and Other Costs to Exit an Activity.” SFAS No. 146 requires that a liability for a cost associated with an exit or

disposal activity be recognized when the liability is incurred, rather than on the date of commitment to an exit plan. This

Statement is effective for exit or disposal activities that are initiated after December 31, 2002. We adopted SFAS No. 146 on

January 1, 2003. The adoption of SFAS No. 146 did not have any material impact on our financial position or results of

operations.

Guarantees

In November 2002, the FASB issued FASB Interpretation No. 45 (“FIN 45”), “Guarantor’s Accounting and Disclosure

Requirements for Guarantees, Including Guarantees of Indebtedness of Others.” FIN 45 requires that a guarantor be required

to recognize, at the inception of a guarantee, a liability for the fair value of the obligation assumed under the guarantee. FIN

45 also requires additional disclosures by a guarantor in its interim and annual financial statements about the obligations

associated with the guarantee. The provisions of FIN 45 are effective for guarantees issued or modified after December 31,

2002, and the disclosure requirements were effective for financial statements for periods ending after December 15, 2002.

We adopted FIN 45 on January 1, 2003. The adoption of FIN 45 did not have any material impact on our financial position

or results of operations.

Stock-Based Compensation

In December 2002, the FASB issued SFAS No. 148, “Accounting for Stock-Based Compensation – Transition and

Disclosure, an amendment of FASB Statement No. 123, “Accounting for Stock-Based Compensation.” SFAS No. 148

provides alternative methods of transition for a voluntary change to the fair value based method of accounting for stock-based

compensation and amends the disclosure requirements of SFAS No. 123 to require prominent disclosures in both annual and

interim financial statements. This statement is effective for fiscal years ending after December 15, 2002. We have adopted

the expanded disclosure requirements of SFAS No. 148.

In December 2004, the FASB issued SFAS No. 123 (revised 2004), “Share-Based Payment,” (“SFAS No. 123R”). SFAS No.

123R requires that stock-based employee compensation be recorded as a charge to earnings for interim or annual periods

beginning after June 15, 2005. Accordingly, we will adopt SFAS No. 123R commencing July 1, 2005 (third quarter) and expect

to recognize approximately $3.0 million of expense for the last six months of 2005.

Derivative Instruments and Hedging

In April 2003, the FASB issued SFAS No. 149, “Amendment of Statement 133 on Derivative Instruments and Hedging,”

which clarifies financial accounting and reporting for derivative instruments including derivative instruments embedded in

other contracts. This Statement is effective for contracts entered into or modified after June 30, 2003. We adopted SFAS No.

149 on July 1, 2003. The adoption of SFAS No. 149 did not have any material impact on our financial position or results of

operations.

Financial Instruments with Characteristics of Both Liabilities and Equity

In May 2003, the FASB issued SFAS No. 150, “Accounting for Certain Financial Instruments with Characteristics of Both

Liabilities and Equity.” SFAS No. 150 establishes standards for the classification and measurement of certain financial

instruments with characteristics of both liabilities and equity. Generally, SFAS No. 150 is effective for financial instruments

entered into or modified after May 31, 2003 and is otherwise effective at the beginning of the first interim period beginning

after June 15, 2003. We adopted the provisions of SFAS No. 150 on July 1, 2003. The adoption of SFAS No. 150 did not

have any material impact on our financial position or results of operations.