Frontier Communications 2004 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2004 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

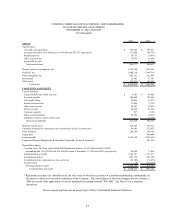

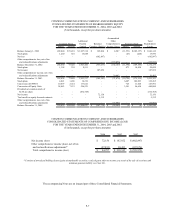

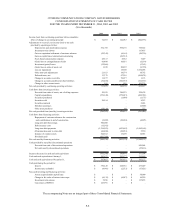

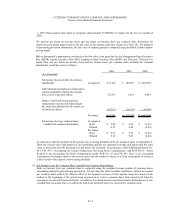

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

Notes to Consolidated Financial Statements

F-10

assets and liabilities, including property, plant and equipment, goodwill and other identifiable intangibles. On

January 1, 2002, we adopted Statement of Financial Accounting Standards (SFAS) No. 142, “Goodwill and

Other Intangible Assets,” which applies to all goodwill and other intangible assets recognized in the statement of

financial position at that date, regardless of when the assets were initially recognized. This statement requires

that goodwill and other intangibles with indefinite useful lives no longer be amortized to earnings, but instead be

tested for impairment, at least annually. In performing this test, the Company first compares the carrying

amount of its reporting units to their respective fair values. If the carrying amount of any reporting unit exceeds

its fair value, the Company is required to perform step two of the impairment test by comparing the implied fair

value of the reporting unit’s goodwill with its carrying amount. The amortization of goodwill and other

intangibles with indefinite useful lives ceased upon adoption of the statement on January 1, 2002. We annually

(during the fourth quarter) examine the carrying value of our goodwill and trade name to determine whether

there are any impairment losses and have determined for the year ended December 31, 2004 that there was no

impairment (see Notes 2 and 7). All remaining intangibles at December 31, 2004 are associated with the ILEC

segment, which is the reporting unit.

SFAS No. 142 also requires that intangible assets with estimated useful lives be amortized over those lives and be

reviewed for impairment in accordance with SFAS No. 144, “Accounting for Impairment or Disposal of Long-

Lived Assets” to determine whether any changes to these lives are required. We periodically reassess the useful life

of our intangible assets with estimated useful lives to determine whether any changes to those lives are required.

(g) Impairment of Long-Lived Assets and Long-Lived Assets to Be Disposed Of:

We adopted SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets” as of January 1,

2002. In accordance with SFAS No. 144, we review long-lived assets to be held and used and long-lived assets to

be disposed of, including intangible assets with estimated useful lives, for impairment whenever events or changes

in circumstances indicate that the carrying amount of such assets may not be recoverable. Recoverability of assets

to be held and used is measured by comparing the carrying amount of the asset to the future undiscounted net cash

flows expected to be generated by the asset. Recoverability of assets held for sale is measured by comparing the

carrying amount of the assets to their estimated fair market value. If any assets are considered to be impaired, the

impairment is measured by the amount by which the carrying amount of the assets exceeds the estimated fair value

(see Note 5).

(h) Derivative Instruments and Hedging Activities:

We account for derivative instruments and hedging activities in accordance with SFAS No. 133, “Accounting for

Derivative Instruments and Hedging Activities”, as amended. SFAS No. 133, as amended, requires that all

derivative instruments, such as interest rate swaps, be recognized in the financial statements and measured at fair

value regardless of the purpose or intent of holding them.

On the date the derivative contract is entered into, we designate the derivative as either a fair value or cash flow

hedge. A hedge of the fair value of a recognized asset or liability or of an unrecognized firm commitment is a

fair value hedge. A hedge of a forecasted transaction or the variability of cash flows to be received or paid

related to a recognized asset or liability is a cash flow hedge. We formally document all relationships between

hedging instruments and hedged items, as well as its risk-management objective and strategy for undertaking the

hedge transaction. This process includes linking all derivatives that are designated as fair-value or cash flow

hedges to specific assets and liabilities on the balance sheet or to specific firm commitments or forecasted

transactions.

We also formally assess, both at the hedge’s inception and on an ongoing basis, whether the derivatives that are

used in hedging transactions are highly effective in offsetting changes in fair values or cash flows of hedged

items. If it is determined that a derivative is not highly effective as a hedge or that it has ceased to be a highly

effective hedge, we would discontinue hedge accounting prospectively.

All derivatives are recognized on the balance sheet at their fair value. Changes in the fair value of derivative

financial instruments are either recognized in income or stockholders’ equity (as a component of other

comprehensive income), depending on whether the derivative is being used to hedge changes in fair value or

cash flows.