Electronic Arts 2016 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2016 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

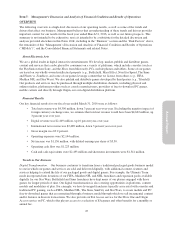

assets were realizable. While we reported U.S. pre-tax income in fiscal year 2015, because we reported U.S. pre-

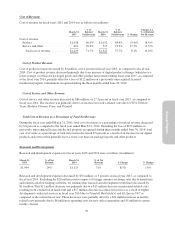

tax losses during the previous seven fiscal years, as well as in the second and third quarters of fiscal year 2016,

we continued to maintain the 100% valuation allowance through the third quarter of fiscal year 2016.

In the fourth quarter of fiscal year 2016, we realized significant U.S. pre-tax income for both the fourth quarter

and the fiscal year ended March 31, 2016. As of March 31, 2016, we had reported positive operating

performance in the U.S. for two consecutive fiscal years and had also reported a cumulative three-year U.S. pre-

tax profit. In addition, during the fourth quarter of fiscal year 2016, we completed our financial plan for fiscal

year 2017 and expect continued positive operating performance in the U.S. We also considered forecasts of

future taxable income and evaluated the utilization of tax credit carryforwards prior to their expiration. After

considering these factors, we determined that the positive evidence overcame any negative evidence and

concluded that it was more likely than not that the U.S. deferred tax assets were realizable. As a result, we

released the valuation allowance against all of the U.S. federal deferred tax assets and a portion of the U.S. state

deferred tax assets during the fourth quarter of fiscal year 2016. Accordingly, we recorded a $453 million income

tax benefit in fiscal year 2016 for the reversal of a significant portion of our deferred tax valuation allowance.

As of March 31, 2016, we maintained a valuation allowance of $114 million, primarily related to specific U.S.

state deferred tax assets and foreign capital loss carryovers, due to uncertainty about the future realization of

these assets. In determining the amount of deferred tax assets that are more likely than not to be realized, we

evaluated the potential to realize the assets through the utilization of tax loss and credit carrybacks, the reversal

of existing taxable temporary differences, future taxable income exclusive of the reversal of existing taxable

temporary differences, and certain tax planning strategies.

In the ordinary course of our business, there are many transactions and calculations where the tax law and

ultimate tax determination is uncertain. As part of the process of preparing our Consolidated Financial

Statements, we are required to estimate our income taxes in each jurisdiction in which we operate prior to the

completion and filing of tax returns for such periods. This process requires estimating both our geographic mix of

income and our uncertain tax positions in each jurisdiction where we operate. These estimates involve complex

issues and require us to make judgments about the likely application of the tax law to our situation, as well as

with respect to other matters, such as anticipating the positions that we will take on tax returns prior to our

actually preparing the returns and the outcomes of disputes with tax authorities. The ultimate resolution of these

issues may take extended periods of time due to examinations by tax authorities and statutes of limitations. In

addition, changes in our business, including acquisitions, changes in our international corporate structure,

changes in the geographic location of business functions or assets, changes in the geographic mix and amount of

income, as well as changes in our agreements with tax authorities, valuation allowances, applicable accounting

rules, applicable tax laws and regulations, rulings and interpretations thereof, developments in tax audit and other

matters, and variations in the estimated and actual level of annual pre-tax income can affect the overall effective

income tax rate.

Impact of Recently Issued Accounting Standards

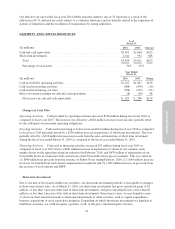

In April 2015, the FASB issued ASU 2015-05, Intangibles — Goodwill and Other — Internal-Use Software

(Topic 350-40). The amendments of this ASU will help entities evaluate the accounting for fees paid by a

customer in a cloud computing arrangement by providing guidance as to whether an arrangement includes the

sale or license of software. The requirements will be effective for annual periods (and interim periods within

those annual periods) beginning after December 15, 2015. The amendment may be adopted either prospectively

to all arrangements entered into or materially modified after the effective date or retrospectively. Early adoption

is permitted. We expect to adopt this new standard in the first quarter of fiscal year 2017. We do not expect the

adoption to have a material impact on our Consolidated Financial Statements.

In March 2016, the FASB issued ASU 2016-09, Compensation — Stock Compensation (Topic 718):

Improvements to Employee Share-Based Payment Accounting, related to simplifications of employee share-based

payment accounting. This pronouncement eliminates the APIC pool concept and requires that excess tax benefits

and tax deficiencies be recorded in the income statement when awards are settled. The pronouncement also

32