CarMax 2009 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2009 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

53

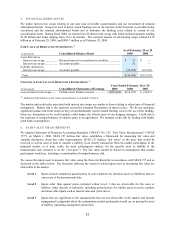

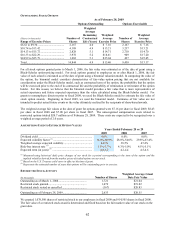

Our fair value processes include controls that are designed to ensure that fair values are appropriate. Such controls

include model validation, review of key model inputs, analysis of period-over-period fluctuations and reviews by

senior management.

Valuation Methodologies

Money market securities. Money market securities are cash equivalents, which are included in either cash and cash

equivalents or other assets, and consist of highly liquid investments with original maturities of three months or less.

We use quoted market prices for identical assets to measure fair value. Therefore, all money market securities are

classified as Level 1.

Retained interest in securitized receivables. We retain an interest in the auto loan receivables that we securitize,

including interest-only strip receivables, various reserve accounts, required excess receivables and retained

subordinated bonds. Excluding the retained subordinated bonds, we estimate the fair value of the retained interest

using internal valuation models. These models include a combination of market inputs and our own assumptions as

described in Note 4. As the valuation models include significant unobservable inputs, we classified the retained

interest as Level 3.

For the retained subordinated bonds, we base our valuation on observable market prices for similar assets when

available. Otherwise, our valuations are based on input from independent third parties and internal valuation

models, as described in Note 4. As the key assumption used in the valuation is currently based on unobservable

inputs, we classified the retained subordinated bonds as Level 3.

Financial derivatives. Financial derivatives are included in either prepaid expenses and other current assets or

accounts payable. As part of our risk management strategy, we utilize interest rate swaps relating to our auto loan

receivable securitizations and our investment in retained subordinated bonds. Swaps are used to better match

funding costs to the interest on the fixed-rate receivables being securitized and the retained subordinated bonds and

to minimize the funding costs related to certain of our securitization trusts. Our derivatives are not exchange-traded

and are over-the-counter customized derivative instruments. All of our derivative exposures are with highly rated

bank counterparties.

We measure derivative fair values assuming that the unit of account is an individual derivative instrument and that

derivatives are sold or transferred on a stand-alone basis. We estimate the fair value of our derivatives using quotes

determined by the swap counterparties. We validate these quotes using our own internal model. Both our internal

model and quotes received from bank counterparties project future cash flows and discount the future amounts to a

present value using market-based expectations for interest rates and the contractual terms of the derivative

instruments. Because model inputs can typically be observed in the liquid market and the models do not require

significant judgment, these derivatives are classified as Level 2.

Our derivative fair value measurements consider assumptions about counterparty and our own nonperformance risk.

We monitor counterparty and our own nonperformance risk and, in the event that we determine that a party is

unlikely to perform under terms of the contract, we would adjust the derivative fair value to reflect the

nonperformance risk.