CarMax 2009 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2009 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

23

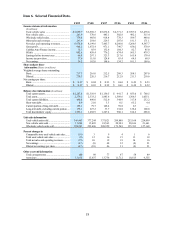

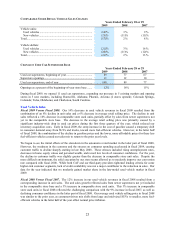

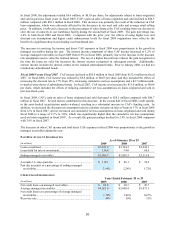

COMPARABLE STORE RETAIL VEHICLE SALES CHANGES

Years Ended February 28 or 29

2009 2008 2007

Vehicle units:

Used vehicles ......................................................................... (16)% 3 % 9 %

New vehicles.......................................................................... (25)% (11)% (11)%

Total........................................................................................... (17)% 2 % 8 %

Vehicle dollars:

Used vehicles ......................................................................... (21)% 3 % 16 %

New vehicles.......................................................................... (26)% (11)% (12)%

Total........................................................................................... (21)% 2 % 13 %

CHANGE IN USED CAR SUPERSTORE BASE

Years Ended February 28 or 29

2009 2008 2007

Used car superstores, beginning of year .................................... 89 77 67

Superstore openings................................................................... 11 12 10

Used car superstores, end of year .............................................. 100 89 77

Openings as a percent of the beginning-of-year store base ....... 12% 16% 15%

During fiscal 2009, we opened 11 used car superstores, expanding our presence in 5 existing markets and opening

stores in 5 new markets, including Huntsville, Alabama; Phoenix, Arizona (2 stores opened); Colorado Springs,

Colorado; Tulsa, Oklahoma; and Charleston, South Carolina.

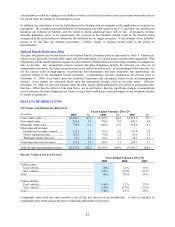

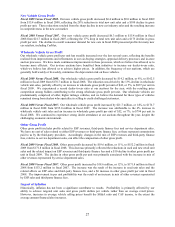

Used Vehicle Sales

Fiscal 2009 Versus Fiscal 2008. Our 14% decrease in used vehicle revenues in fiscal 2009 resulted from the

combination of an 8% decline in unit sales and a 6% decrease in average retail selling price. The decline in unit

sales reflected a 16% decrease in comparable store used units, partially offset by sales from newer superstores not

yet in the comparable store base. The decrease in the average retail selling price was primarily caused by a

significant industry-wide drop in used car prices during the first three quarters of the year, which reduced our

inventory acquisition costs. Early in fiscal 2009, the steep increase in the cost of gasoline caused a temporary shift

in consumer demand away from SUVs and trucks, toward more fuel-efficient vehicles. However, in the latter half

of fiscal 2009, the combination of the decline in gasoline prices and the lower, more affordable prices for these less

fuel-efficient vehicles caused our sales mix to return to the prior year levels.

We began to see the initial effects of the slowdown in the automotive retail market in the latter part of fiscal 2008.

However, the weakness in the economy and the stresses on consumer spending accelerated in fiscal 2009, causing

customer traffic to decline sharply starting in late May 2008. These stresses included rising unemployment rates,

decreases in home equity values and personal wealth, and record low levels of consumer confidence. For the year,

the decline in customer traffic was slightly greater than the decrease in comparable store unit sales. Despite the

more difficult environment, the solid execution by our store teams allowed us to modestly improve our conversion

rate compared with fiscal 2008. While both CAF and our third-party providers tightened lending criteria for some

higher-risk customer segments, lack of credit availability was not a major contributor to the reduction in sales. Our

data for the year indicated that we modestly gained market share in the late-model used vehicle market in fiscal

2009.

Fiscal 2008 Versus Fiscal 2007. The 12% increase in our used vehicle revenues in fiscal 2008 resulted from a

corresponding increase in unit sales. The unit sales growth reflected sales from newer superstores not yet included

in the comparable store base and a 3% increase in comparable store used units. This 3% increase in comparable

store used units in fiscal 2008 reflected the challenging comparison with the 9% increase in fiscal 2007, as well as

declining consumer confidence in the latter part of fiscal 2008. Our average used vehicle selling price in fiscal 2008

was similar to the prior year, as consumer-driven mix shifts from large and mid-sized SUVs to smaller, more fuel-

efficient vehicles in the latter half of the year offset normal price inflation.