Blackberry 2009 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2009 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

54

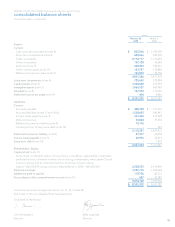

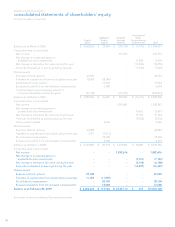

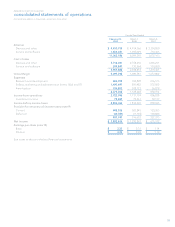

RESEARCH IN MOTION LIMITED

notes to the consolidated financial statements continued

In thousands of United States dollars, except share and per share data, and except as otherwise indicated

(i) Derivative financial instruments

The Company uses derivative financial instruments, including

forward contracts and options, to hedge certain foreign

currency exposures. The Company does not use derivative

financial instruments for speculative purposes.

The Company formally documents relationships between

hedging instruments and associated hedged items. This

documentation includes: identification of the specific foreign

currency asset, liability or forecasted transaction being

hedged; the nature of the risk being hedged; the hedge

objective; and the method of assessing hedge effectiveness.

Hedge effectiveness is formally assessed, both at hedge

inception and on an ongoing basis, to determine whether the

derivatives used in hedging transactions are highly effective

in offsetting changes in foreign currency denominated assets,

liabilities and anticipated cash flows of hedged items.

SFAS 133 Accounting for Derivative Instruments, as

amended by SFAS 137, 138 and 149, requires all derivative

instruments to be recognized at fair value on the consolidated

balance sheet and outlines the criteria to be met in order

to designate a derivative instrument as a hedge and the

methods for evaluating hedge effectiveness. The fair value

is calculated based on quoted market prices. For derivative

instruments designated as cash flow hedges as defined in

SFAS 133, the effective portion of changes in fair value are

recorded in other comprehensive income and subsequently

reclassified to earnings in the period in which the cash flows

from the associated hedged transaction affect earnings.

Ineffective portions of changes in fair value, if any, are

recorded in current earnings. If an anticipated transaction

is deemed no longer likely to occur, the corresponding

derivative instrument is de-designated as a hedge and gains

and losses are recognized in earnings at that time. Any future

changes in the fair value of the instrument are recognized in

current earnings.

For derivative instruments that do not meet the

requirements for hedge accounting under SFAS 133, changes

in fair value are recognized in current earnings and will

generally offset the changes in the U.S. dollar value of the

associated hedged asset or liability.

(j) Inventories

Raw materials are stated at the lower of cost and replacement

cost. Work in process and finished goods inventories are

stated at the lower of cost and net realizable value. Cost

includes the cost of materials plus direct labour applied to the

product and the applicable share of manufacturing overhead.

Cost is determined on a first-in-first-out basis.

products, software and services. The Company expects the

majority of trade receivables to continue to come from large

customers as it sells the majority of its devices and software

products and service relay access through network carriers

and resellers rather than directly.

The Company evaluates the collectability of its trade

receivables based upon a combination of factors on a

periodic basis. When the Company becomes aware of a

specific customer’s inability to meet its financial obligations

to the Company (such as in the case of bankruptcy filings or

material deterioration in the customer’s operating results or

financial position, and payment experiences), RIM records

a specific bad debt provision to reduce the customer’s

related trade receivable to its estimated net realizable value.

If circumstances related to specific customers change,

the Company’s estimates of the recoverability of trade

receivables balances could be further adjusted.

(h) Investments

The Company’s investments, other than cost method

investments of $2.5 million and equity method investments

of $2.7 million, consist of money market and other debt

securities, and are classified as available-for-sale for

accounting purposes. The Company does not exercise

significant influence with respect to any of these investments.

Investments with maturities of less than one year, as well

as any investments that management intends to hold for

less than one year, are classified as Short-term investments.

Investments with maturities of one year or more are classified

as Long-term investments.

Investments classified as available-for-sale under

Statement of Financial Accounting Standards (“SFAS”) 115

are carried at fair value determined under SFAS 157 Fair

Value Measurements. Changes in fair value are accounted for

through Accumulated other comprehensive income until such

investments mature or are sold.

The Company assesses declines in the value of individual

investments for impairment to determine whether the

decline is other-than-temporary. The Company makes this

assessment by considering available evidence, including

changes in general market conditions, specific industry

and individual company data, the length of time and the

extent to which the fair value has been less than cost, the

financial condition, the near-term prospects of the individual

investment and the Company’s intent and ability to hold the

investments. In the event that a decline in the fair value of an

investment occurs and the decline in value is considered to

be other-than-temporary, an impairment charge is recorded

and a new cost basis in the investment is established.