Berkshire Hathaway 1998 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 1998 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

7

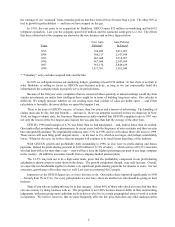

selling insurance to all comers. Furthermore, in 40 states we can offer a special discount — usually 8% — to our

shareholders. So give us a call and check us out.

* * * * * * * * * * * *

You may think that one commercial in this section is enough. But I have another to present, this one directed at

managers of publicly-owned companies.

At Berkshire we feel that telling outstanding CEOs, such as Tony, how to run their companies would be the height

of foolishness. Most of our managers wouldn’t work for us if they got a lot of backseat driving. (Generally, they don’t

have to work for anyone, since 75% or so are independently wealthy.) Besides, they are the Mark McGwires of the

business world and need no advice from us as to how to hold the bat or when to swing.

Nevertheless, Berkshire’s ownership may make even the best of managers more effective. First, we eliminate all

of the ritualistic and nonproductive activities that normally go with the job of CEO. Our managers are totally in charge

of their personal schedules. Second, we give each a simple mission: Just run your business as if: 1) you own 100% of

it; 2) it is the only asset in the world that you and your family have or will ever have; and 3) you can’t sell or merge it

for at least a century. As a corollary, we tell them they should not let any of their decisions be affected even slightly by

accounting considerations. We want our managers to think about what counts, not how it will be counted.

Very few CEOs of public companies operate under a similar mandate, mainly because they have owners who focus

on short-term prospects and reported earnings. Berkshire, however, has a shareholder base — which it will have for

decades to come — that has the longest investment horizon to be found in the public-company universe. Indeed, a

majority of our shares are held by investors who expect to die still holding them. We can therefore ask our CEOs to

manage for maximum long-term value, rather than for next quarter’s earnings. We certainly don’t ignore the current

results of our businesses — in most cases, they are of great importance — but we never want them to be achieved at the

expense of our building ever-greater competitive strengths.

I believe the GEICO story demonstrates the benefits of Berkshire’s approach. Charlie and I haven’t taught Tony

a thing — and never will — but we have created an environment that allows him to apply all of his talents to what’s

important. He does not have to devote his time or energy to board meetings, press interviews, presentations by investment

bankers or talks with financial analysts. Furthermore, he need never spend a moment thinking about financing, credit

ratings or “Street” expectations for earnings per share. Because of our ownership structure, he also knows that this

operational framework will endure for decades to come. In this environment of freedom, both Tony and his company

can convert their almost limitless potential into matching achievements.

If you are running a large, profitable business that will thrive in a GEICO-like environment, check our acquisition

criteria on page 21 and give me a call. I promise a fast answer and will mention your inquiry to no one except

Charlie.

Executive Jet Aviation (1-800-848-6436)

To understand the huge potential at Executive Jet Aviation (EJA), you need some understanding of its business,

which is selling fractional shares of jets and operating the fleet for its many owners. Rich Santulli, CEO of EJA, created

the fractional ownership industry in 1986, by visualizing an important new way of using planes. Then he combined guts

and talent to turn his idea into a major business.

In a fractional ownership plan, you purchase a portion — say /8th — of any of a wide variety of jets that EJA

1

offers. That purchase entitles you to 100 hours of flying time annually. (“Dead-head” hours don’t count against your

allotment, and you are also allowed to average your hours over five years.) In addition, you pay both a monthly

management fee and a fee for hours actually flown.

Then, on a few hours notice, EJA makes your plane, or another at least as good, available to you at your choice of

the 5500 airports in the U.S. In effect, calling up your plane is like phoning for a taxi.