Berkshire Hathaway 1998 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 1998 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

|

|

57

2. In line with Berkshire's owner-orientation, most of our directors have a major portion of their net

worth invested in the company. We eat our own cooking.

Charlie's family has 90% or more of its net worth in Berkshire shares; my wife, Susie, and I have

more than 99%. In addition, many of my relatives — my sisters and cousins, for example — keep

a huge portion of their net worth in Berkshire stock.

Charlie and I feel totally comfortable with this eggs-in-one-basket situation because Berkshire itself

owns a wide variety of truly extraordinary businesses. Indeed, we believe that Berkshire is close

to being unique in the quality and diversity of the businesses in which it owns either a controlling

interest or a minority interest of significance.

Charlie and I cannot promise you results. But we can guarantee that your financial fortunes will

move in lockstep with ours for whatever period of time you elect to be our partner. We have no

interest in large salaries or options or other means of gaining an "edge" over you. We want to make

money only when our partners do and in exactly the same proportion. Moreover, when I do

something dumb, I want you to be able to derive some solace from the fact that my financial

suffering is proportional to yours.

3. Our long-term economic goal (subject to some qualifications mentioned later) is to maximize

Berkshire's average annual rate of gain in intrinsic business value on a per-share basis. We do not

measure the economic significance or performance of Berkshire by its size; we measure by per-share

progress. We are certain that the rate of per-share progress will diminish in the future — a greatly

enlarged capital base will see to that. But we will be disappointed if our rate does not exceed that

of the average large American corporation.

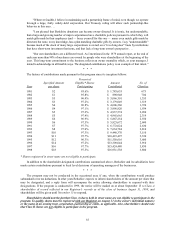

Since that was written at yearend 1983, our intrinsic value (a topic I'll discuss a bit later) has

increased at an annual rate of more than 25%, a pace that has definitely surprised both Charlie and

me. Nevertheless the principle just stated remains valid: Operating with large amounts of capital

as we do today, we cannot come close to performing as well as we once did with much smaller

sums. The best rate of gain in intrinsic value we can even hope for is an average of 15% per annum,

and we may well fall far short of that target. Indeed, we think very few large businesses have a

chance of compounding intrinsic value at 15% per annum over an extended period of time. So it

may be that we will end up meeting our stated goal — being above average — with gains that fall

significantly short of 15%.

4. Our preference would be to reach our goal by directly owning a diversified group of businesses that

generate cash and consistently earn above-average returns on capital. Our second choice is to own

parts of similar businesses, attained primarily through purchases of marketable common stocks by

our insurance subsidiaries. The price and availability of businesses and the need for insurance

capital determine any given year's capital allocation.

As has usually been the case, it is easier today to buy small pieces of outstanding businesses via the

stock market than to buy similar businesses in their entirety on a negotiated basis. Nevertheless, we

continue to prefer the 100% purchase, and in some years we get lucky: In the last three years in

fact, we made seven acquisitions. Though there will be dry years also, we expect to make a number

of acquisitions in the decades to come, and our hope is that they will be large. If these purchases

approach the quality of those we have made in the past, Berkshire will be well served.

The challenge for us is to generate ideas as rapidly as we generate cash. In this respect, a depressed

stock market is likely to present us with significant advantages. For one thing, it tends to reduce the

prices at which entire companies become available for purchase. Second, a depressed market makes

it easier for our insurance companies to buy small pieces of wonderful businesses — including

additional pieces of businesses we already own — at attractive prices. And third, some of those same

wonderful businesses, such as Coca-Cola, are consistent buyers of their own shares, which means

that they, and we, gain from the cheaper prices at which they can buy.