Berkshire Hathaway 1998 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 1998 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

33

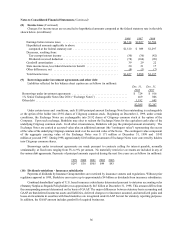

(6) Finance and financial products businesses (Continued)

Interest rate, currency and equity swaps are agreements between two parties to exchange, at particular intervals, payment

streams calculated on a specified notional amount. Interest rate, currency and equity options grant the purchaser the right,

but not the obligation, to either purchase from or sell to the writer a specified financial instrument under agreed terms.

Interest rate caps and floors require the writer to pay the purchaser at specified future dates the amount, if any, by which the

option’s underlying market interest rate exceeds the fixed cap or falls below the fixed floor, applied to a notional amount.

Futures contracts are commitments to either purchase or sell a financial instrument at a future date for a specified price

and are generally settled in cash. Forward-rate agreements are financial instruments that settle in cash at a specified future

date based on the differential between agreed interest rates applied to a notional amount. Foreign exchange contracts

generally involve the exchange of two currencies at agreed rates on a specified date; spot contracts usually require the

exchange to occur within two business days of the contract date.

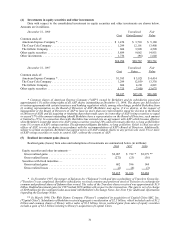

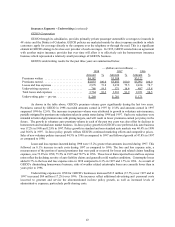

A summary of notional amounts of derivative contracts at December 31, 1998 is included in the table below. For

these transactions, the notional amount represents the principal volume, which is referenced by the counterparties in

computing payments to be exchanged, and are not indicative of the Company’s exposure to market or credit risk, future cash

requirements or receipts from such transactions.

December 31, 1998

(in millions)

Interest rate and currency swap agreements .................................. $514,935

Options written ....................................................... 88,245

Options purchased ..................................................... 90,826

Financial futures contracts:

Commitments to purchase .............................................. 26,041

Commitments to sell .................................................. 6,872

Forward - rate agreements ............................................... 24,579

Foreign exchange spot and forward contracts ................................ 14,794

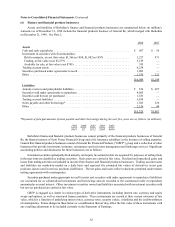

The table below discloses the net fair value or carrying amount at the reporting date for each class of derivative financial

contract held or issued by GRFP.

December 31, 1998

Asset Liability

(in millions)

Interest rate and foreign currency swaps ................................ $25,963 $25,445

Interest rate and foreign currency options ............................... 4,338 4,439

Gross fair value ................................................... 30,301 29,884

Adjustment for counterparty netting ................................... (24,067)(24,067)

Net fair value ..................................................... 6,234 5,817

Security receivables/payables ......................................... — 17

Trading account assets/liabilities ...................................... $ 6,234 $ 5,834

These derivative financial instruments involve, to varying degrees, elements of market, credit, and legal risks. Market

risk is the possibility that future changes in market conditions may make the derivative financial instrument less valuable.

Credit risk is defined as the possibility that a loss may occur from the failure of another party to perform in accordance with

the terms of the contract which exceeds the value of existing collateral, if any. The derivative’s risk of credit loss i s

generally a small fraction of notional value of the instrument and is represented by the fair value of the derivative financial

instrument. Legal risk arises from the uncertainty of the enforceability of the obligations of another party, including

contractual provisions intended to reduce credit exposure by providing for the offsetting or netting of mutual obligations.