Berkshire Hathaway 1998 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 1998 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

5

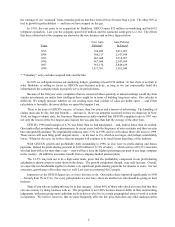

of 9,500 in hands-on employees, we have enlarged the staff at world headquarters from 12 to 12.8. (The .8 doesn’t refer

to me or Charlie: We have a new person in accounting, working four days a week.) Despite this alarming trend toward

corporate bloat, our after-tax overhead last year was about $3.5 million, or well under one basis point (.01 of 1%) of the

value of the assets we manage.

Taxes

One beneficiary of our increased size has been the U.S. Treasury. The federal income taxes that Berkshire and

General Re have paid, or will soon pay, in respect to 1998 earnings total $2.7 billion. That means we shouldered all of

the U.S. Government’s expenses for more than a half-day.

Follow that thought a little further: If only 625 other U.S. taxpayers had paid the Treasury as much as we and

General Re did last year, no one else — neither corporations nor 270 million citizens — would have had to pay federal

income taxes or any other kind of federal tax (for example, social security or estate taxes). Our shareholders can truly

say that they “gave at the office.”

Writing checks to the IRS that include strings of zeros does not bother Charlie or me. Berkshire as a corporation,

and we as individuals, have prospered in America as we would have in no other country. Indeed, if we lived in some

other part of the world and completely escaped taxes, I’m sure we wou ld be worse off financially (and in many other ways

as well). Overall, we feel extraordinarily lucky to have been dealt a hand in life that enables us to write large checks to

the government rather than one requiring the government to regularly write checks to us — say, because we are disabled

or unemployed.

Berkshire’ s tax situation is sometimes misunderstood. First, capital gains have no special attraction for us: A

corporation pays a 35% rate on taxable income, whether it comes from capital gains or from ordinary operations. This

means that Berkshire’s tax on a long-term capital gain is fully 75% higher than what an individual would pay on a n

identical gain.

Some people harbor another misconception, believing that we can exclude 70% of all dividends we receive from

our taxable income. Indeed, the 70% rate applies to most corporations and also applies to Berkshire in cases where we

hold stocks in non-insurance subsidiaries. However, almost all of our equity investments are owned by our insurance

companies, and in that case the exclusion is 59.5%. That still means a dollar of dividends is considerably more valuable

to us than a dollar of ordinary income, but not to the degree often assumed.

* * * * * * * * * * * *

Berkshire truly went all out for the Treasury last year. In connection with the General Re merger, we wrote a $30

million check to the government to pay an SEC fee tied to the new shares created by the deal. We understand that this

payment set an SEC record. Charlie and I are enormous admirers of what the Commission has accomplished for

American investors. We would rather, however, have found another way to show our admiration.

GEICO (1-800-847-7536)

Combine a great idea with a great manager and you’re certain to obtain a great result. That mix is alive and well

at GEICO. The idea is low-cost auto insurance, made possible by direct-to-customer marketing, and the manager is Tony

Nicely. Quite simply, there is no one in the business world who could run GEICO better than Tony does. His instincts

are unerring, his energy is boundless, and his execution is flawless. While maintaining underwriting discipline, Tony

is building an organization that is gaining market share at an accelerating rate.

This pace has been encouraged by our compensation policies. The direct writing of insurance — that is, without

there being an agent or broker between the insurer and its policyholder — involves a substantial front-end investment.

First-year business is therefore unprofitable in a major way. At GEICO, we do not wish this cost to deter our associates

from the aggressive pursuit of new business — which, as it renews, will deliver significant profits — so we leave it out

of our compensation formulas. What’s included then? We base 50% of our associates’ bonuses and profit sharing on