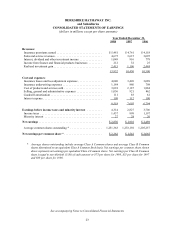

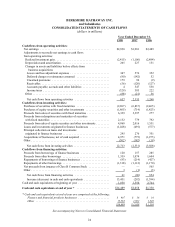

Berkshire Hathaway 1998 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 1998 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

14

has mushroomed. This lop-sided choice has a big downside for owners, however: Though options, if properly

structured, can be an appropriate, and even ideal, way to compensate and motivate top managers, they are more

often wildly capricious in their distribution of rewards, inefficient as motivators, and inordinately expensive for

shareholders.

Whatever the merits of options may be, their accounting treatment is outrageous. Think for a moment of that

$190 million we are going to spend for advertising at GEICO this year. Suppose that instead of paying cash for

our ads, we paid the media in ten-year, at-the-market Berkshire options. Would anyone then care to argue

that Berkshire had not borne a cost for advertising, or should not be charged this cost on its books?

Perhaps Bishop Berkeley — you may remember him as the philosopher who mused about trees falling in a

forest when no one was around — would believe that an expense unseen by an accountant does not exist. Charlie

and I, however, have trouble being philosophical about unrecorded costs. When we consider investing in an option-

issuing company, we make an appropriate downward adjustment to reported earnings, simply subtracting an amount

equal to what the company could have realized by publicly selling options of like quantity and structure. Similarly,

if we contemplate an acquisition, we include in our evaluation the cost of replacing any option plan. Then, if we

make a deal, we promptly take that cost out of hiding.

Readers who disagree with me about options will by this time be mentally quarreling with my equating the

cost of options issued to employees with those that might theoretically be sold and traded publicly. It is true, to

state one of these arguments, that employee options are sometimes forfeited — that lessens the damage done to

shareholders — whereas publicly-offered options would not be. It is true, also, that companies receive a tax

deduction when employee options are exercised; publicly-traded options deliver no such benefit. But there’s a n

offset to these points: Options issued to employees are often repriced, a transformation that makes them much more

costly than the public variety.

It’s sometimes argued that a non-transferable op tion given to an employee is less valuable to him than would

be a publicly-traded option that he could freely sell. That fact, however, does not reduce the cost of the non-

transferable option: Giving an employee a company car that can only be used for certain purposes diminishes its

value to the employee, but does not in the least diminish its cost to the employer.

The earning revisions that Charlie and I have made for options in recent years have frequently cut the

reported per-share figures by 5%, with 10% not all that uncommon. On occasion, the downward adjustment has

been so great that it has affected our portfolio decisions, causing us either to make a sale or to pass on a stock

purchase we might otherwise have made.

A few years ago we asked three questions in these pages to which we have not yet received an answer: “If

options aren’t a form of compensation, what are they? If compensation isn’t an expense, what is it? And, i f

expenses shouldn’t go into the calculation of earnings, where in the world should they go?”

Accounting — Part 2

The role that managements have played in stock-option accounting has hardly been benign: A distressing

number of both CEOs and auditors have in recent years bitterly fought FASB’s attempts to replace option fiction

with truth and virtually none have spoken out in support of FASB. Its opponents even enlisted Congress in the

fight, pushing the case that inflated figures were in the national interest.

Still, I believe that the behavior of managements has been even worse when it comes to restructurings and

merger accounting. Here, many managements purposefully work at manipulating numbers and deceiving investors.

And, as Michael Kinsley has said about Washington: “The scandal isn’t in what’s done that’s illegal but rather

in what’s legal.”

It was once relatively easy to tell the good guys in accounting from the bad: The late 1960's, for example,

brought on an orgy of what one charlatan dubbed “bold, imaginative accounting” (the practice of which,

incidentally, made him loved for a time by Wall Street because he never missed expectations). But most investors