Berkshire Hathaway 1998 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 1998 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

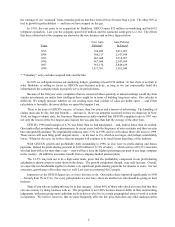

|

|

9

General Re

On December 21, we completed our $22 billion acquisition of General Re Corp. In addition to owning 100% of

General Reinsurance Corporation, the largest U.S. property-casualty reinsurer, the company also owns (including stock

it has an arrangement to buy) 82% of the oldest reinsurance company in the world, Cologne Re. The two companies

together reinsure all lines of insurance and operate in 124 countries.

For many decades, General Re’s name has stood for quality, integrity and professionalism in reinsurance — and

under Ron Ferguson’s leadership, this reputation has been burnished still more. Berkshire can add absolutely nothing

to the skills of General Re’s and Cologne Re’s managers. On the contrary, there is a lot that they can teach us.

Nevertheless, we believe that Berkshire’s ownership will benefit General Re in important ways and that its earnings

a decade from now will materially exceed those that would have been attainable absent the merger. We base this

optimism on the fact that we can offer General Re’s management a freedom to operate in whatever manner will best allow

the company to exploit its strengths.

Let’s look for a moment at the reinsurance business to understand why General Re could not on its own do what

it can under Berkshire. Most of the demand for reinsurance comes from primary insurers who want to escape the wide

swings in earnings that result from large and unusual losses. In effect, a reinsurer gets paid for absorbing the volatility

that the client insurer wants to shed.

Ironically, though, a publicly-held reinsurer gets graded by both its owners and those who evaluate its credit on the

smoothness of its own results. Wide swings in earnings hurt both credit ratings and p/e ratios, even when the business

that produces such swings has an expectancy of satisfactory profits over time. This market reality sometimes causes a

reinsurer to make costly moves, among them laying off a significant portion of the business it writes (in transactions that

are called “retrocessions”) or rejecting good business simply because it threatens to bring on too much volatility.

Berkshire, in contrast, happily accepts volatility, just as long as it carries with it the expectation of increased profits

over time. Furthermore, we are a Fort Knox of capital, and that means volatile earnings can’t impair our premier credit

ratings. Thus we have the perfect structure for writing — and retaining — reinsurance in virtually any amount. In fact,

we’ve used this strength over the past decade to build a powerful super-cat business.

What General Re gives us, however, is the distribution force, technical facilities and management that will allow

us to employ our structural strength in every facet of the industry. In particular, General Re and Cologne Re can now

accelerate their push into international markets, where the preponderance of industry growth will almost certainly occur.

As the merger proxy statement spelled out, Berkshire also brings tax and investment benefits to General Re. But the most

compelling reason for the merger is simply that General Re’s outstanding management can now do what it does best,

unfettered by the constraints that have limited its growth.

Berkshire is assuming responsibility for General Re’s investment portfolio, though not for Cologne Re’s. We will

not, however, be involved in General Re’s underwriting. We will simply ask the company to exercise the discipline of

the past while increasing the proportion of its business that is retained, expanding its product line, and widening its

geographical coverage — making these moves in recognition of Berkshire’s financial strength and tolerance for wide

swings in earnings. As we’ve long said, we prefer a lumpy 15% return to a smooth 12%.

Over time, Ron and his team will maximize General Re’s new potential. He and I have known each other fo r

many years, and each of our companies has initiated significant business that it has reinsured with the other. Indeed,

General Re played a key role in the resuscitation of GEICO from its near-death status in 1976.

Both Ron and Rich Santulli plan to be at the annual meeting, and I hope you get a chance to say hello to them.