Advance Auto Parts 2003 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2003 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

|

|

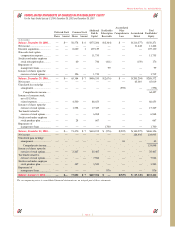

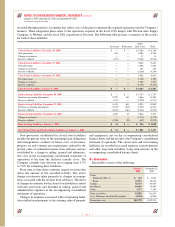

7—Inventories, Net

Inventories are stated at the lower of cost or market. Cost

was determined using the last-in, first-out (“LIFO”) method

for approximately 93% and 91% of inventories at January 3,

2004 and December 28, 2002, respectively, and the first-in,

first-out (“FIFO”) method for remaining inventories. The

remaining inventories consist of product cores, which consist

of the non-consumable portion of certain parts and batteries.

Core values are included as part of our merchandise costs

and are either passed on to the customer or returned to the

vendor. Additionally, these products are not subject to the

frequent cost changes like our other merchandise inventory,

therefore resulting in no material difference from applying

either the LIFO or FIFO valuation methods.

The Company capitalizes certain purchasing and ware-

housing costs into inventory. Purchasing and warehousing

costs included in inventory, at FIFO, at January 3, 2004

and December 28, 2002, were $75,349 and $69,160,

respectively. Inventories consist of the following:

January 3,

December 28,

2004

2002

Inventories at FIFO, net............................. $1,051,678 $ 988,856

Adjustments to state

inventories at LIFO................................ 62,103 59,947

Inventories at LIFO, net............................. $1,113,781 $1,048,803

Replacement cost approximated FIFO cost at January 3,

2004 and December 28, 2002.

Inventory quantities are tracked through a perpetual

inventory system. The Company uses a cycle counting

program in all distribution centers, Parts Delivered Quickly

(“PDQs”), Local Area Warehouses, or LAWs, and retail

stores to ensure the accuracy of the perpetual inventory

quantities of both merchandise and core inventory. The

Company establishes reserves for estimated shrink based on

historical accuracy and effectiveness of the cycle counting

program. The Company also establishes reserves for poten-

tially excess and obsolete inventories based on current

inventory levels of discontinued product and the historical

analysis of the liquidation of discontinued inventory below

cost. The nature of the Company’s inventory is such that the

risk of obsolescence is minimal and excess inventory has

historically been returned to the Company’s vendors for

credit. The Company provides reserves when less than

full credit is expected from a vendor or when liquidating

product will result in retail prices below recorded costs.

The Company’s reserves against inventory for these

matters were $16,011 and $16,289 at January 3, 2004 and

December 28, 2002, respectively.

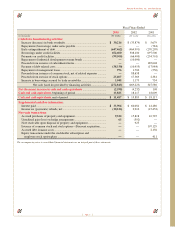

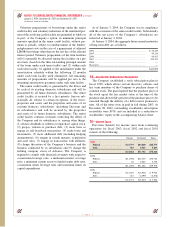

8—Property and Equipment

Property and equipment are stated at cost, less accu-

mulated depreciation and amortization. Expenditures for

maintenance and repairs are charged directly to expense

when incurred; major improvements are capitalized. When

items are sold or retired, the related cost and accumulated

depreciation are removed from the accounts, with any gain or

loss reflected in the consolidated statements of operations.

Depreciation of land improvements, buildings, furniture,

fixtures and equipment, and vehicles is provided over the

estimated useful lives, which range from 2 to 40 years, of

the respective assets using the straight-line method.

Amortization of building and leasehold improvements is

provided over the shorter of the original useful lives of the

respective assets or the term of the lease using the straight-

line method. Depreciation and amortization expense was

$100,737, $94,090 and $70,745 for the fiscal years ended

2003, 2002 and 2001, respectively.

Property and equipment consists of the following:

Original

January 3,

December 28,

Useful Lives

2004

2002

Land and land improvements

... 0–10 years $ 177,088 $ 178,513

Buildings

................................ 40 years 214,919 209,457

Building and leasehold

improvements

...................... 10–40 years 110,974 101,019

Furniture, fixtures

and equipment

..................... 3–12 years 553,759 505,044

Vehicles

.................................. 2–10 years 36,338 32,516

Other

...................................... 14,651 15,724

1,107,729 1,042,273

Less: Accumulated depreciation

and amortization

.................. (395,027) (313,841)

Property and equipment, net

.... $ 712,702 $ 728,432

The Company capitalized approximately $5,423, $2,888

and $19,699 incurred for the development of internal use

computer software during fiscal 2003, fiscal 2002 and fiscal

2001, respectively. These costs are included in the furniture,

fixtures and equipment category above and are depreciated

on the straight-line method over three to seven years.

9—Assets Held for Sale

The Company applies SFAS No. 144, “Accounting for

the Impairment or Disposal of Long-Lived Assets,” which

requires that long-lived assets and certain identifiable intan-

gible assets to be disposed of be reported at the lower of the

carrying amount or the fair market value less selling costs.

At January 3, 2004 and December 28, 2002, the Company’s

assets held for sale were $20,191 and $28,346, respectively,

primarily consisting of closed stores as a result of the

Discount integration and a closed distribution center.

Page 35

Advance Auto Parts, Inc. and Subsidiaries