Advance Auto Parts 2003 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2003 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

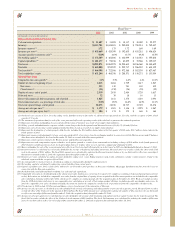

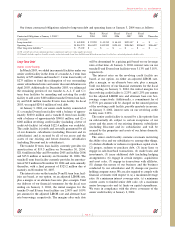

Seasonality

Our business is somewhat seasonal in nature, with the

highest sales occurring in the spring and summer months. In

addition, our business can be affected by weather condi-

tions. While unusually heavy precipitation tends to soften

sales as elective maintenance is deferred during such periods,

extremely hot or cold weather tends to enhance sales by

causing automotive parts to fail.

Recent Accounting Pronouncements

In April 2002, the FASB issued SFAS No. 145, “Rescission

of FASB Statements No. 4, 44 and 64, Amendment of FASB

Statement No. 13 and Technical Corrections.” As a result of

rescinding FASB Statement No. 4, “Reporting Gains Losses

from Extinguishment of Debt,” gains and losses from extin-

guishment of debt should be classified as extraordinary

items only if they meet the criteria in APB Opinion No. 30,

“Reporting the Results of Operations—Reporting the Effects

of Disposal of a Segment of a Business, and Extraordinary,

Unusual and Infrequently Occurring Events and Transactions.”

This statement also amends FASB Statement No. 13,

“Accounting for Leases,” to eliminate an inconsistency

between the required accounting for sale-leaseback trans-

actions and the required accounting for certain lease

modifications that have economic effects that are similar to

sale-leaseback transactions. Additional amendments include

changes to other existing authoritative pronouncements to

make various technical corrections, clarify meanings or

describe their applicability under changed conditions. We

adopted SFAS No. 145 during the first quarter of fiscal

2003. For the fiscal years ended 2003, 2002 and 2001, we

recorded losses on the extinguishment of debt of $47.3 mil-

lion, $16.8 million and $6.1 million, respectively and

appropriately reclassified such amounts.

In September 2002 (as subsequently updated in Novem-

ber 2003), the FASB released EITF Issue No. 02-16,

“Accounting by a Customer (Including a Reseller) for

Certain Consideration Received from a Vendor.” This EITF

addresses how a reseller should account for consideration

received from a vendor since EITF Issue No. 01-9,

“Accounting for Consideration Given by a Vendor to a

Customer (including a Reseller of the Vendor’s Products),”

only addresses the accounting treatment from the vendor’s

perspective. The consensus is that cash received from a

vendor is presumed to be a reduction of the vendor’s prod-

ucts or services and should, therefore, be characterized as

a reduction in the cost of sales when recognized in the

customer’s income statement, unless a reimbursement of

costs is incurred by the customer to sell the vendor’s products,

in which case the cash consideration should be characterized

as a reduction of that cost when recognized in the customer’s

income statement. Additionally, any rebate or refund should

also be recognized as a reduction of the cost of sales based

on a systematic and rational allocation. The release is effec-

tive for fiscal periods beginning after December 15, 2002.

Our current accounting policy for vendor incentives meets

the requirements of this EITF and therefore the adoption of

this release during the first quarter of fiscal 2003 had no

impact on our financial position or results of operations.

In November 2002, the FASB issued Interpretation,

or FIN, No. 45, “Guarantor’s Accounting and Disclosure

Requirements for Guarantees, Including Indirect Guar-

antees of Indebtedness of Others.” FIN No. 45 sets forth

expanded disclosure requirements in the financial statements

about a guarantor’s obligations under certain guarantees

that it has issued. It also clarifies that, under certain circum-

stances, a guarantor is required to recognize a liability

for the fair value of the obligation at the inception of the

guarantee. Certain types of guarantees, such as product

warranties, guarantees accounted for as derivatives, and

guarantees related to parent-subsidiary relationships are

excluded from the liability recognition provisions of

FIN No. 45, however, they are subject to the disclosure

requirements. The initial liability recognition provisions are

applicable on a prospective basis to guarantees issued or

modified after December 31, 2002. The disclosure require-

ments of Interpretation No. 45 are effective for financial

statements for interim or annual periods ending after

December 15, 2002. We have no guarantees of third-party

indebtedness and therefore the adoption of FIN No. 45

during the first quarter of fiscal 2003 had no impact on our

financial position or results of operations. Additionally, we

have complied with the disclosure aspect of FIN No. 45 as

it relates to warranties.

In January 2003, the FASB issued Interpretation No. 46,

“Consolidation of Variable Interest Entities,” an interpreta-

tion of Accounting Research Bulletin No. 51, “Consolidated

Financial Statements.” Interpretation No. 46 prescribes how

to identify variable interest entities and how an enterprise

assesses its interests in a variable interest entity to decide

whether to consolidate that entity. This interpretation

requires existing unconsolidated variable interest entities to

be consolidated by their primary beneficiaries if the entities

do not effectively disperse risks among parties involved.

Interpretation No. 46 is effective immediately for variable

interest entities created after January 31, 2003, and to

variable interest entities in which an enterprise obtains an

interest after that date. The interpretation applies in the first

fiscal year or interim period beginning after June 15, 2003,

to variable interest entities in which an enterprise holds a

variable interest that it acquired before February 1, 2003.

We do not have interests in variable interest entities; there-

fore, the adoption of Interpretation No. 46 had no impact on

our financial position or results of operations.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (continued)

Page 20