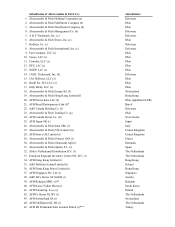

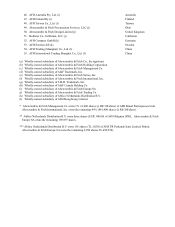

Abercrombie & Fitch 2013 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2013 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

|

|

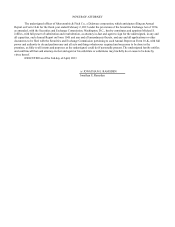

April 2, 2013

Board of Directors of

Abercrombie & Fitch Co.

6301 Fitch Path

New Albany, Ohio 43054

Dear Directors:

We are providing this letter to you for inclusion as an exhibit to your Form 10-K filing pursuant to Item 601 of Regulation S-K.

We have audited the consolidated financial statements included in the Company's Annual Report on Form 10-K for the year

ended February 2, 2013 and issued our report thereon dated April 2, 2013. Note 4 to the financial statements describes a

change in accounting principle from the retail inventory method to weighted average cost in accounting for inventory. It should

be understood that the preferability of one acceptable method of accounting over another for inventory accounting methods has

not been addressed in any authoritative accounting literature, and in expressing our concurrence below we have relied on

management's determination that this change in accounting principle is preferable. Based on our reading of management's

stated reasons and justification for this change in accounting principle in the Form 10-K, and our discussions with management

as to their judgment about the relevant business planning factors relating to the change, we concur with management that such

change represents, in the Company's circumstances, the adoption of a preferable accounting principle in conformity with

Accounting Standards Codification 250, Accounting Changes and Error Corrections.

Very truly yours,

/s/ PricewaterhouseCoopers LLP