AT&T Wireless 2013 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2013 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

|

|

Notes to Consolidated Financial Statements (continued)

Dollars in millions except per share amounts

62 | AT&T Inc.

future economic scenarios, to maximize long-term

investment return with an acceptable level of risk based

on our pension and postretirement obligations, and to

be broadly diversified across and within the capital

markets to insulate asset values against adverse

experience in any one market. Each asset class has

broadly diversified characteristics. Substantial biases

toward any particular investing style or type of security

are sought to be avoided by managing the aggregation

of all accounts with portfolio benchmarks. Asset and

benefit obligation forecasting studies are conducted

periodically, generally every two to three years, or when

significant changes have occurred in market conditions,

benefits, participant demographics or funded status.

Decisions regarding investment policy are made with

an understanding of the effect of asset allocation on

funded status, future contributions and projected

expenses. The current asset allocation policy and risk

level for the pension plan and VEBA assets is based

on a study completed and approved during 2013 and

is reflected in the table below.

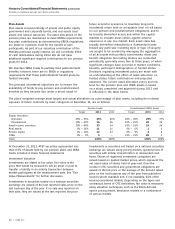

Plan Assets

Plan assets consist primarily of private and public equity,

government and corporate bonds, and real assets (real

estate and natural resources). The asset allocations of the

pension plans are maintained to meet ERISA requirements.

Any plan contributions, as determined by ERISA regulations,

are made to a pension trust for the benefit of plan

participants. As part of our voluntary contribution of the

Mobility preferred equity interest, we will contribute $560

of cash distributions during 2014. We do not have

additional significant required contributions to our pension

plans for 2014.

We maintain VEBA trusts to partially fund postretirement

benefits; however, there are no ERISA or regulatory

requirements that these postretirement benefit plans be

funded annually.

The principal investment objectives are to ensure the

availability of funds to pay pension and postretirement

benefits as they become due under a broad range of

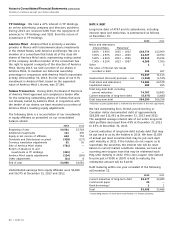

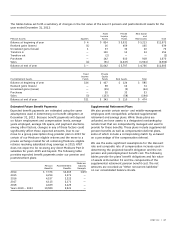

The plans’ weighted-average asset targets and actual allocations as a percentage of plan assets, including the notional

exposure of future contracts by asset categories at December 31, are as follows:

Pension Assets Postretirement (VEBA) Assets

Target 2013 2012 Target 2013 2012

Equity securities:

Domestic 25% – 35% 25% 26% 20% – 30% 25% 37%

International 10% – 20% 16 16 15% – 25% 20 33

Fixed income securities 30% – 40% 33 34 19% – 29% 24 24

Real assets 6% – 16% 11 11 0% – 6% 1 1

Private equity 4% – 14% 12 13 0% – 9% 4 4

Other 0% – 5% 3 — 21% – 31% 26 1

Total 100% 100% 100% 100%

Investments in securities not traded on a national securities

exchange are valued using pricing models, quoted prices of

securities with similar characteristics or discounted cash

flows. Shares of registered investment companies are

valued based on quoted market prices, which represent the

net asset value of shares held at year-end. Over-the-

counter (OTC) securities and government obligations are

valued at the bid price or the average of the bid and asked

price on the last business day of the year from published

sources where available and, if not available, from other

sources considered reliable. Depending on the types and

contractual terms of OTC derivatives, fair value is measured

using valuation techniques, such as the Black-Scholes

option pricing model, simulation models or a combination

of various models.

At December 31, 2013, AT&T securities represented less

than 0.5% of assets held by our pension plans and VEBA

trusts included in these financial statements.

Investment Valuation

Investments are stated at fair value. Fair value is the

price that would be received to sell an asset or paid to

transfer a liability in an orderly transaction between

market participants at the measurement date. See “Fair

Value Measurements” for further discussion.

Investments in securities traded on a national securities

exchange are valued at the last reported sales price on the

last business day of the year. If no sale was reported on

that date, they are valued at the last reported bid price.