AT&T Wireless 2013 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2013 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

AT&T Inc. | 15

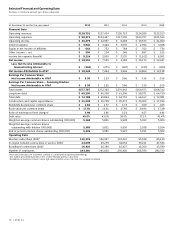

Wireless Metrics

Subscriber Additions As of December 31, 2013,

we served 110.4 million wireless subscribers, an increase

of 3.2% from 2012. Market maturity in traditional wireless

subscribers continues to limit the rate of growth in the

industry’s subscriber base, contributing to a 1.4% decrease

in our gross subscriber additions (gross additions) in

2013 and a decrease of 13.0% in 2012.

Net subscriber additions (net additions) in 2013 were lower

primarily due to losses in low-revenue reseller accounts.

Lower net additions in 2012, as compared to 2011, were

primarily attributable to lower net connected device and

reseller additions when compared to the prior year, which

reflected higher churn rates for customers not using such

devices (zero-revenue customers).

Average service revenue per user (ARPU) – Postpaid

increased 1.6% in 2013 and 1.9% in 2012, driven by

increases in data services ARPU of 16.9% in 2013 and

17.9% in 2012, reflecting greater use of smartphones

and data-centric devices by our subscribers.

The growth in postpaid data services ARPU in 2013 and

2012 was partially offset by a 5.0% decrease in postpaid

voice and other service ARPU in 2013 and a 3.7% decrease

in 2012. Voice and other service ARPU declined due to

lower access and airtime charges, triggered in part by

postpaid subscribers on our discount plans, and lower

roaming revenues.

ARPU – Total increased 0.9% in 2013, reflecting growth

in data services as more subscribers are using smartphones

and tablets and choosing medium- and higher-priced

usage-based data plans. Total ARPU decreased 1.6% in

2012, reflecting growth in connected device, tablet and

reseller subscribers, which have lower-priced data-only

plans compared with our postpaid smartphone plans.

We expect continued revenue growth from data services

as more subscribers use smartphones and data-centric

devices. While price changes may impact revenue and

service ARPU, going forward we expect to increase

equipment sales under our AT&T Next installment program.

Data services ARPU increased 15.1% in 2013 and 16.1% in

2012, reflecting increased smartphone and data-centric

device use. Voice, text and other service ARPU declined

5.5% in 2013 and 7.9% in 2012 due to voice access and

usage trends and a shift toward a greater percentage of

data-centric devices. We expect continued pressure on

voice, text and other service ARPU.

Churn The effective management of subscriber churn is

critical to our ability to maximize revenue growth and to

maintain and improve margins. While the postpaid churn

rate was lower in 2013, the total churn rate was up slightly

in 2013, reflecting increased competition, especially for

price-conscious customers. Total and postpaid churn were

subscribers) use smartphones, up from 69.6% (or

47.1million subscribers) a year earlier and 58.5%

(or 39.4million subscribers) two years ago. As is

common in the industry, most of our subscribers’ phones

are designed to work only with our wireless technology,

requiring subscribers who desire to move to a new carrier

with a different technology to purchase a new device.

Our postpaid subscribers also continued to add more

tablets, reflecting the popularity of our Mobile Share plan.

Our postpaid subscribers typically sign a two-year contract,

which includes discounted handsets and early termination

fees. About 90% of our postpaid smartphone subscribers

are on FamilyTalk® plans (family plans), Mobile Share plans

or business plans, which provide for service on multiple

devices at reduced rates, and such subscribers tend to have

higher retention and lower churn rates. During 2013, we

introduced additional programs that allow for the purchase

of handsets on installments and for reduced-price service

plans. We also offer data plans at different price levels

(usage-based data plans) to attract a wide variety of

subscribers and to differentiate us from our competitors.

Our postpaid subscribers on data plans increased 10.2%

year over year. A growing percentage of our postpaid

smartphone subscribers are on usage-based data plans,

with 72.6% (or 37.7 million subscribers) on these plans

as of December 31, 2013, up from 67.4% (or 31.7 million

subscribers) as of December 31, 2012, and 56.0%

(or 22.1million subscribers) as of December 31, 2011.

About 80% of subscribers on usage-based data plans have

chosen the medium- and higher-data plans. Such offerings

are intended to encourage existing subscribers to upgrade

their current services and/or add connected devices,

attract subscribers from other providers and minimize

subscriber churn.

As of December 31, 2013, approximately 77% of our

postpaid smartphone subscribers use a 4G-capable

device (i.e., a device that would operate on our HSPA+

or LTEnetwork), and more than 50% of our postpaid

smartphone subscribers use an LTE device. Due to

substantial increases in the demand for wireless service

in the United States, AT&T is facing significant spectrum

and capacity constraints on its wireless network in

certain markets. We expect such constraints to increase

and expand to additional markets in the coming years.

While we are continuing to invest significant capital in

expanding our network capacity, our capacity constraints

could affect the quality of existing data and voice services

and our ability to launch new, advanced wireless broadband

services, unless we are able to obtain more spectrum.

Any long-term spectrum solution will require that the

Federal Communications Commission (FCC) make new

or existing spectrum available to the wireless industry to

meet the expanding needs of our subscribers. We will

continue to attempt to address spectrum and capacity

constraints on a market-by-market basis.