Entergy 2010 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2010 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

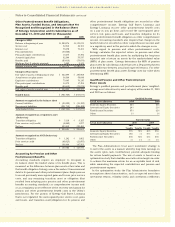

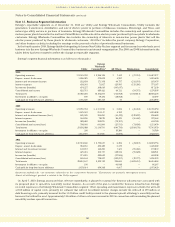

Notes to Consolidated Financial Statements continued

Qualified Pension Obligations, Plan Assets, Funded

Status, Amounts Recognized in the Balance Sheet

for Entergy Corporation and its Subsidiaries as of

December 31, 2010 and 2009 (in thousands):

2010 2009

Change in Projected Benefit Obligation (PBO)

Balance at beginning of year $ 3,837,744 $ 3,305,315

Service cost 104,956 89,646

Interest cost 231,206 218,172

Acturarial loss 293,189 385,221

Employee contributions 894 852

Benefits paid (166,771) (161,462)

Balance at end of year $ 4,301,218 $ 3,837,744

Change in Plan Assets

Fair value of assets at beginning of year $ 2,607,274 $ 2,078,252

Actual return on plan assets 320,517 557,642

Employer contributions 454,354 131,990

Employee contributions 894 852

Benefits paid (166,771) (161,462)

Fair value of assets at end of year $ 3,216,268 $ 2,607,274

Funded status $(1,084,950) $(1,230,470)

Amount recognized in the balance sheet

Non-current liabilities $ (1,084,950) $ (1,230,470)

Amount recognized as a regulatory asset

Prior service cost $ 12,979 $ 16,376

Net loss 1,350,616 1,183,824

$ 1,363,595 $ 1,200,200

Amount recognized as AOCI (before tax)

Prior service cost $ 2,855 $ 4,116

Net loss 297,093 297,507

$ 299,948 $ 301,623

Other Postretirement Benefits

Entergy also currently provides health care and life insurance

benefits for retired employees. Substantially all employees may

become eligible for these benefits if they reach retirement age

while still working for Entergy. Entergy uses a December 31

measurement date for its postretirement benefit plans.

Effective January 1, 1993, Entergy adopted an accounting

standard requiring a change from a cash method to an accrual

method of accounting for postretirement other than pensions.

At January 1, 1993, the actuarially determined accumulated

postretirement benefit obligation (APBO) earned by retirees

and active employees was estimated to be approximately

$241.4 million for Entergy (other than the former Entergy Gulf

States) and $128 million for the former Entergy Gulf States (now

split into Entergy Gulf States Louisiana and Entergy Texas). Such

obligations are being amortized over a 20-year period that began

in 1993. For the most part, the Registrant Subsidiaries recover

other postretirement benefit costs from customers and are

required to contribute other postretirement benefits collected in

rates to an external trust.

Entergy Arkansas, Entergy Mississippi, Entergy New Orleans,

and Entergy Texas have received regulatory approval to recover

other postretirement benefit costs through rates. Entergy

Arkansas began recovery in 1998, pursuant to an APSC order. This

order also allowed Entergy Arkansas to amortize a regulatory

asset (representing the difference between other postretirement

benefit costs and cash expenditures for other postretirement

benefits incurred for a five-year period that began January 1,

1993) over a 15-year period that began in January 1998.

The LPSC ordered Entergy Gulf States Louisiana and Entergy

Louisiana to continue the use of the pay-as-you-go method for

ratemaking purposes for postretirement benefits other than

pensions. However, the LPSC retains the flexibility to examine

individual companies’ accounting for other postretirement

benefits to determine if special exceptions to this order are

warranted.

Pursuant to regulatory directives, Entergy Arkansas, Entergy

Mississippi, Entergy New Orleans, Entergy Texas, and System

Energy contribute the other postretirement benefit costs

collected in rates into trusts. System Energy is funding, on behalf

of Entergy Operations, other postretirement benefits associated

with Grand Gulf.

Trust assets contributed by participating Registrant Sub-

sidiaries are in three bank-administered trusts, established

by Entergy Corporation and maintained by a trustee. Each

participating Registrant Subsidiary holds a beneficial interest

in the trusts’ assets. Use of these master trusts permits the

commingling of the trust assets for investment and administrative

purposes. Although assets are commingled, the trustee maintains

supporting records for the purpose of allocating the beneficial

interest in net earnings (losses) and the administrative expenses

of the investment accounts to the various participating plans and

participating Registrant Subsidiaries. Beneficial interest in an

investment account’s net income/ (loss) is comprised of interest

and dividends and realized and unrealized gains and losses and

expense. Beneficial interest from these investments is allocated

monthly to the plans and participating Registrant Subsidiary

based on its portion of net assets in the pooled accounts.

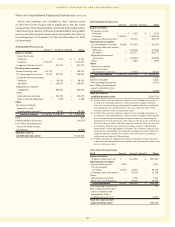

Components of Net Other Postretirement Benefit

Cost and Other Amounts Recognized as a Regulatory

Asset and/or AOCI

Entergy Corporation’s and its subsidiaries’ total 2010, 2009, and

2008 other postretirement benefit costs, including amounts

capitalized and amounts recognized as a regulatory asset and/or

other comprehensive income, included the following components

(in thousands):

2010 2009 2008

Other postretirement costs:

Service cost - benefits earned

during the period $ 52,313 $ 46,765 $ 47,198

Interest cost on APBO 76,078 75,265 71,295

Expected return on assets (26,213) (23,484) (28,109)

Amortization of transition obligation 3,728 3,732 3,827

Amortization of prior service credit (12,060) (16,096) (16,417)

Recognized net loss 17,270 18,970 15,565

Net other postretirement benefit cost $111,116 $105,152 $ 93,359

Other changes in plan assets and benefit

obligations recognized as a regulatory

asset and/or AOCI (before tax)

Arising this period:

Prior service credit for period $(50,548) $ – $ (5,422)

Net loss 82,189 24,983 59,291

Amounts reclassified from regulatory

asset and/or AOCI to net periodic

benefit cost in the current year:

Amortization of transition obligation (3,728) (3,732) (3,827)

Amortization of prior service credit 12,060 16,096 16,417

Amortization of net loss (17,270) (18,970) (15,565)

Total $ 22,703 $ 18,377 $ 50,894

Total recognized as net periodic

benefit cost, regulatory asset,

and/or AOCI (before tax) $133,819 $123,529 $144,253

Estimated amortization amounts from

regulatory asset and/or AOCI to net

periodic benefit cost in the following year

Transition obligation $ 3,183 $ 3,728 $ 3,729

Prior service credit $(14,070) $(12,060) $(17,519)

Net loss $ 21,192 $ 17,270 $ 19,018

94