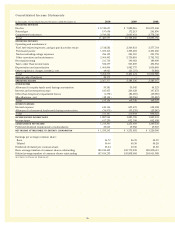

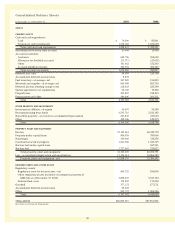

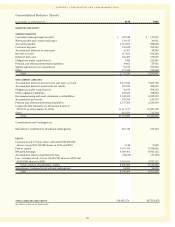

Entergy 2010 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2010 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

Management’s Financial Discussion and Analysis continued

Cost Sensitivity

The following chart reflects the sensitivity of qualified

pension cost to changes in certain actuarial assumptions

(dollars in thousands):

Impact on

Qualified

Impact on 2010 Projected

Change in Qualified Benefit

Actuarial Assumption Assumption Pension Cost Obligation

Increase/(Decrease)

Discount rate (0.25%) $13,682 $131,414

Rate of return on plan assets (0.25%) $ 7,634 –

Rate of increase in

compensation 0.25% $ 6,367 $ 30,374

The following chart reflects the sensitivity of postretirement

benefit cost to changes in certain actuarial assumptions (dollars

in thousands):

Impact on

Accumulated

Impact on 2010 Postretirement

Change in Postretirement Benefit

Actuarial Assumption Assumption Benefit Cost Obligation

Increase/(Decrease)

Health care cost trend 0.25% $6,500 $34,291

Discount rate (0.25%) $4,375 $40,557

Each fluctuation above assumes that the other components of

the calculation are held constant.

ACCOUNTING MECHANISMS

Effective December 31, 2006, accounting standards required an

employer to recognize in its balance sheet the funded status of

its benefit plans. Refer to Note 11 to the financial statements for a

further discussion of Entergy’s funded status.

In accordance with pension accounting standards, Entergy

utilizes a number of accounting mechanisms that reduce the

volatility of reported pension costs. Differences between actuarial

assumptions and actual plan results are deferred and are

amortized into expense only when the accumulated differences

exceed 10% of the greater of the projected benefit obligation

or the market-related value of plan assets. If necessary, the

excess is amortized over the average remaining service period of

active employees.

Entergy calculates the expected return on pension and other

postretirement benefit plan assets by multiplying the long-term

expected rate of return on assets by the market-related value

(MRV) of plan assets. Entergy determines the MRV of pension

plan assets by calculating a value that uses a 20-quarter phase-in

of the difference between actual and expected returns. For other

postretirement benefit plan assets Entergy uses fair value when

determining MRV.

COSTS AND FUNDING

In 2010, Entergy’s total qualified pension cost was $147.1 million.

Entergy anticipates 2011 qualified pension cost to be $154

million. Pension funding was $454 million for 2010. Entergy’s

contributions to the pension trust are currently estimated to

be approximately $368.8 million in 2011, although the required

pension contributions will not be known with more certainty until

the January 1, 2011 valuations are completed by April 1, 2011.

Minimum required funding calculations as determined under

Pension Protection Act guidance are performed annually as of

January 1 of each year and are based on measurements of the

assets and funding liabilities as measured at that date. Any

excess of the funding liability over the calculated fair market value

of assets results in a funding shortfall which, under the Pension

Protection Act, must be funded over a seven-year rolling period.

The Pension Protection Act also imposes certain plan limitations

if the funded percentage, which is based on a calculated fair

market values of assets divided by funding liabilities, does not

meet certain thresholds. For funding purposes, asset gains and

losses are smoothed in to the calculated fair market value of

assets and the funding liability is based upon a weighted average

24-month corporate bond rate published by the U.S. Treasury;

therefore, periodic changes in asset returns and interest rates

can affect funding shortfalls and future cash contributions.

Total postretirement health care and life insurance benefit costs

for Entergy in 2010 were $111.1 million, including $26.6 million

in savings due to the estimated effect of future Medicare Part D

subsidies. Entergy expects 2011 postretirement health care and

life insurance benefit costs to be $114.7 million. This includes a

projected $33 million in savings due to the estimated effect of

future Medicare Part D subsidies. Entergy contributed $75 million

to its postretirement plans in 2010. Entergy’s current estimate of

contributions to its other postretirement plans is approximately

$78 million in 2011.

FEDERAL HEALTHCARE LEGISLATION

The Patient Protection and Affordable Care Act (PPACA) became

federal law on March 23, 2010, and, on March 30, 2010, the Health

Care and Education Reconciliation Act of 2010 became federal law

and amended certain provisions of the PPACA. These new federal

laws change the law governing employer-sponsored group health

plans, like Entergy’s plans, and include, among other things, the

following significant provisions:

n A 40% excise tax on per capita medical benefit costs that

exceed certain thresholds;

n Change in coverage limits for dependants; and

n Elimination of lifetime caps.

The total impact of PPACA is not yet determinable because

technical guidance regarding application must still be issued.

Additionally, ongoing litigation and political discussions are

in progress regarding the constitutionality of and the potential

repeal of health care reform, although whether that occurs

and what parts of health care reform would be invalidated or

repealed is not yet known. Entergy will continue to monitor these

developments to determine the possible impact on Entergy as a

result of PPACA. Entergy is participating in the programs currently

provided for under PPACA, such as the early retiree reinsurance

program, which may provide for some limited reimbursements

of certain claims for early retirees aged 55 to 64 who are not yet

eligible for Medicare.

One provision of the new law that is effective in 2013 eliminates

the federal income tax deduction for prescription drug expenses

of Medicare beneficiaries for which the plan sponsor also receives

the retiree drug subsidy under Part D. Entergy receives subsidy

payments under the Medicare Part D plan and therefore in the

first quarter 2010 recorded a reduction to the deferred tax asset

related to the unfunded other postretirement benefit obligation.

The offset was recorded as a $16 million charge to income tax

expense or, for the Utility, including each Registrant Subsidiary,

as a regulatory asset.

52