Entergy 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

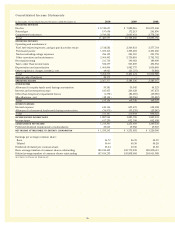

Management’s Financial Discussion and Analysis continued

Entergy Wholesale Commodities to deliver MWh of energy to its

counterparties, make capacity available to them, or both. The

following is a summary as of December 31, 2010 of the amount of

Entergy Wholesale Commodities’ nuclear power plants’ planned

energy output that is sold forward under physical or financial

contracts:

Entergy Wholesale Commodities 2011 2012 2013 2014 2015

Percent of planned generation

sold forward:

Unit-contingent 79% 59% 34% 14% 12%

Unit-contingent with

guarantee of availability(1) 17% 14% 6% 3% 3%

Firm LD 3% 24% 0% 8% 0%

Offsetting positions (3%) (10%) 0% 0% 0%

Total energy sold forward 96% 87% 40% 25% 15%

Planned generation (TWh)(4) 41 41 40 41 41

Average revenue under

contract per MWh(2)(3) $53 $49 $47 $51 $51

(1) A sale of power on a unit-contingent basis coupled with a guarantee of

availability provides for the payment to the power purchaser of contract

damages, if incurred, in the event the seller fails to deliver power as a

result of the failure of the specified generation unit to generate power at

or above a specified availability threshold. All of Entergy’s outstanding

guarantees of availability provide for dollar limits on Entergy’s maximum

liability under such guarantees.

(2) The Vermont Yankee acquisition included a 10-year PPA under which the

former owners will buy most of the power produced by the plant, which

is through the expiration in 2012 of the current operating license for the

plant. The PPA includes an adjustment clause under which the prices

specified in the PPA will be adjusted downward monthly, beginning in

November 2005, if power market prices drop below PPA prices, which has

not happened thus far.

(3) Average revenue under contract may fluctuate due to positive or negative

basis differences, option premiums, costs to convert firm LD to unit-

contingent, and other risk management costs. Also, average revenue under

contract excludes payments owed under the value sharing agreement

with NYPA.

(4) Assumes license renewal for plants whose current licenses expire within

five years. License renewal applications are in process for four units, as

follows (with current license expirations in parentheses): Vermont Yankee

(March 2012), Pilgrim (June 2012), Indian Point 2 (September 2013), and

Indian Point 3 (December 2015).

Entergy estimates that a $10 per MWh change in the annual

average energy price in the markets in which the Entergy

Wholesale Commodities nuclear business sells power, based

on December 31, 2010 market conditions, planned generation

volume, and hedged position, would have a corresponding effect

on pre-tax net income of $17 million in 2011. Entergy estimates

that, based on December 31, 2009 market conditions, planned

generation volume, and hedged position, a $10 per MWh change in

the annual average energy price would have had a corresponding

effect on pre-tax net income of $53 million in 2010.

Entergy’s purchase of the FitzPatrick and Indian Point 3 plants

from NYPA included value sharing agreements with NYPA. In

October 2007, NYPA and the subsidiaries that own the FitzPatrick

and Indian Point 3 plants amended and restated the value

sharing agreements to clarify and amend certain provisions of

the original terms. Under the amended value sharing agreements,

the Entergy subsidiaries agreed to make annual payments to

NYPA based on the generation output of the Indian Point 3 and

FitzPatrick plants from January 2007 through December 2014.

Entergy subsidiaries will pay NYPA $6.59 per MWh for power

sold from Indian Point 3, up to an annual cap of $48 million, and

$3.91 per MWh for power sold from FitzPatrick, up to an annual

cap of $24 million. The annual payment for each year’s output

is due by January 15 of the following year. Entergy will record

the liability for payments to NYPA as power is generated and

sold by Indian Point 3 and FitzPatrick. In 2010, 2009, and 2008,

Entergy Wholesale Commodities recorded a $72 million liability

for generation during each of those years. An amount equal to

the liability was recorded each year to the plant asset account

as contingent purchase price consideration for the plants. This

amount will be depreciated over the expected remaining useful

life of the plants.

Some of the agreements to sell the power produced by Entergy

Wholesale Commodities’ power plants contain provisions that

require an Entergy subsidiary to provide collateral to secure

its obligations under the agreements. The Entergy subsidiary

is required to provide collateral based upon the difference

between the current market and contracted power prices in

the regions where Entergy Wholesale Commodities sells power.

The primary form of collateral to satisfy these requirements is

an Entergy Corporation guaranty. Cash and letters of credit are

also acceptable forms of collateral. At December 31, 2010, based

on power prices at that time, Entergy had credit exposure of

$14 million under the guarantees in place supporting Entergy

Nuclear Power Marketing (a subsidiary in the Entergy Wholesale

Commodities segment) transactions, $20 million of guarantees

that support letters of credit, and $5 million of posted cash

collateral to the ISOs. As of December 31, 2010, the credit

exposure associated with Entergy Wholesale Commodities

assurance requirements would increase by $123 million for a

$1 per MMBtu increase in gas prices in both the short-and long-

term markets. In the event of a decrease in Entergy Corporation’s

credit rating to below investment grade, based on power prices

as of December 31, 2010, Entergy would have been required to

provide approximately $78 million of additional cash or letters of

credit under some of the agreements.

As of December 31, 2010, the counterparties or their guarantors

for 99.7% of the planned energy output under contract for Entergy

Wholesale Commodities nuclear plants through 2015 have public

investment grade credit ratings and 0.3% is with load-serving

entities without public credit ratings.

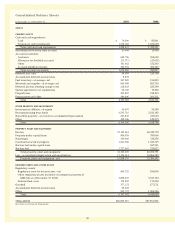

In addition to selling the power produced by its plants, Entergy

Wholesale Commodities sells unforced capacity to load-serving

distribution companies in order for those companies to meet

requirements placed on them by the ISO in their area. Following is

a summary as of December 31, 2010 of the amount of the Entergy

Wholesale Commodities nuclear plants’ installed capacity that is

sold forward, and the blended amount of the Entergy Wholesale

Commodities nuclear plants’ planned generation output and

installed capacity that is sold forward:

Entergy Wholesale Commodities 2011 2012 2013 2014 2015

Percent of capacity sold forward:

Bundled capacity and

energy contracts 25% 18% 16% 16% 16%

Capacity contracts 37% 29% 26% 10% 0%

Total capacity sold forward 62% 47% 42% 26% 16%

Planned net MW in operation 4,998 4,998 4,998 4,998 4,998

Average revenue under contract

per kW per month $2.6 $3.0 $3.1 $3.5 $ –

(applies to capacity contracts only)

Blended capacity and

energy recap (based on revenues)

% of planned generation

and capacity sold forward 96% 87% 40% 26% 15%

Average revenue under

contract per MWh $54 $51 $50 $53 $52

48