Dollar Tree 2004 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2004 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

32 DOLLAR TREE STORES, INC. • 2004 ANNUAL REPORT

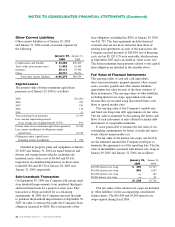

Cash and Cash Equivalents

Cash and cash equivalents at January 29, 2005 and

January 31, 2004 includes $75,885 and $54,081,

respectively, of investments in money market securities

and bank participation agreements which are valued at

cost, which approximates market. The underlying assets

of these short-term participation agreements are primarily

commercial notes. For purposes of the consolidated

statements of cash flows, the Company considers all

highly liquid debt instruments with original maturities

of three months or less to be cash equivalents.

Short-Term Investments

The Company’s short-term investments consist primarily

of government-sponsored municipal bonds and auction

rate securities. These investments are classified as

available for sale and are recorded at fair value. The

government-sponsored municipal bonds can be converted

into cash with one or seven day notice. The auction rate

securities have stated interest rates, which typically reset

to market prevailing rates every 35 days or less. The

securities underlying both the government-sponsored

municipal bonds and the auction rate securities have

longer legal maturity dates. Prior to the end of fiscal

2004, the Company classified a portion of these

investments in cash and cash equivalents due to their

liquidity. Prior period information was reclassified,

including the impact on cash flow from investing

activities, to conform to the current year presentation.

There was no impact on net income or cash flow from

operating activities as a result of the reclassification.

Merchandise Inventories

Merchandise inventories at the distribution centers are

stated at the lower of cost or market, determined on a

weighted average cost basis. Cost is assigned to store

inventories using the retail inventory method, determined

on a weighted average cost basis.

Costs directly associated with warehousing and

distribution are capitalized as merchandise inventories.

Total warehousing and distribution costs capitalized into

inventory amounted to $27,968 and $24,510 at January

29, 2005 and January 31, 2004, respectively.

Property, Plant and Equipment

Property, plant and equipment are stated at cost and

depreciated using the straight-line method over the

estimated useful lives of the respective assets as follows:

Buildings 39 years

Furniture, fixtures and equipment 3 to 15 years

Transportation vehicles 4 to 6 years

Leasehold improvements and assets held under capital

leases are amortized over the estimated useful lives of the

respective assets or the committed terms of the related

leases, whichever is shorter. Amortization is included in

“selling, general and administrative expenses”on the

accompanying consolidated statements of operations.

In the fourth quarter of 2004, the Company revised

its estimate of useful lives on certain store equipment and

distribution center assets. This change will increase net

income by approximately $3,700 in the first three

quarters of 2005 as compared to 2004.

Costs incurred related to software developed for

internal use are capitalized and amortized over three

years. Costs capitalized include those incurred in the

application development stage as defined in Statement

of Position 98-1, Accounting for the Costs of Computer

Software Developed or Obtained for Internal Use.

Impairment of Long-Lived Assets and

Long-Lived Assets to Be Disposed Of

The Company reviews its long-lived assets and certain

identifiable intangible assets for impairment whenever

events or changes in circumstances indicate that the

carrying amount of an asset may not be recoverable, in

accordance with Statement of Financial Accounting

Standards (SFAS) No. 144, Accounting for the Impairment

or Disposal of Long-Lived Assets. Recoverability of assets to

be held and used is measured by comparing the carrying

amount of an asset to future net undiscounted cash flows

expected to be generated by the asset. If such assets are

considered to be impaired, the impairment to be

recognized is measured by the amount by which the

carrying amount of the assets exceeds the fair value of the

assets based on discounted cash flows or other readily

available evidence of fair value, if any. Assets to be disposed

of are reported at the lower of the carrying amount or

fair value less costs to sell. In fiscal 2004 and 2003, the

Company recorded charges of $531 and $234, respectively,

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)