Dollar Tree 2004 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2004 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

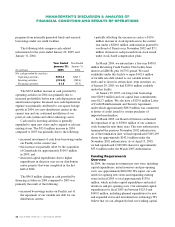

DOLLAR TREE STORES, INC. • 2004 ANNUAL REPORT 21

requirements and planned capital expenditures for the next few years from net cash provided by operations and

borrowings under our existing credit facilities.

The following tables summarize our material contractual obligations, including both on- and off-balance sheet

arrangements, and our commitments (in millions):

Contractual Obligations Total 2005 2006 2007 2008 2009 Thereafter

Lease Financing

Operating lease obligations $ 914.9 $216.9 $188.6 $156.3 $119.2 $ 83.6 $150.3

Capital lease obligations (primarily sale-leaseback) 13.7 13.1 0.3 0.2 0.1 0.0 —

Long-term Borrowings

Revolving credit facility 250.0 — — — — 250.0 —

Revenue bond financing 19.0 19.0 — — — — —

Total obligations $1,197.6 $249.0 $188.9 $156.5 $119.3 $333.6 $150.3

Expiring Expiring Expiring Expiring Expiring

Commitments Total in 2005 in 2006 in 2007 in 2008 in 2009 Thereafter

Letters of credit and surety bonds $ 129.0 $129.0 $ — $ — $ — $ — $ —

Freight contracts 35.5 25.5 10.0 — — — —

Technology assets 5.8 5.8 — — — — —

Total commitments $ 170.3

$160.3 $ 10.0

$— $—

$— $—

Lease Financing

Operating Lease Obligations. Our operating lease

obligations are primarily for payments under noncancel-

able store leases. The commitment includes amounts for

leases that were signed prior to January 29, 2005 for

stores that were not yet open on January 29, 2005.

Capital Lease Obligations (primarily sale-leaseback).

In September 1999, we sold certain retail store leasehold

improvements to an unrelated third party and leased

them back for seven years. As a result of the transaction,

we received net cash of $20.9 million and an $8.1 million

11.0% note receivable, which matures in October 2005.

In 2004, we exercised the right to repurchase the leasehold

improvements at October 31, 2005. In order to exercise

this right, our lease obligation related to these improve-

ments increased by $0.2 million. The total amount of the

lease obligation at January 29, 2005 was $11.7 million.

The obligation and the note receivable will both be

satisfied at the buyout date of October 31, 2005.

Long-Term Borrowings

Revolving Credit Facility. In March 2004, we entered

into a five-year Revolving Credit Facility (the Facility).

The Facility provides for a $450.0 million line of credit,

including up to $50.0 million in available letters of credit,

bearing interest at LIBOR, plus 0.475%. The Facility,

among other things, requires the maintenance of certain

specified financial ratios, restricts the payment of certain

distributions and prohibits the incurrence of certain new

indebtedness. We used availability under this Facility to

repay the $142.6 million of variable-rate debt and to

purchase short-term investments. As of January 29, 2005,

we had $250.0 million outstanding on this Facility.

Revenue Bond Financing. In May 1998, we entered

into an agreement with the Mississippi Business Finance

Corporation under which it issued $19.0 million of

variable-rate demand revenue bonds. We borrowed the

proceeds from the bonds to finance the acquisition,

construction and installation of land, buildings, machinery

and equipment for our distribution facility in Olive

Branch, Mississippi. At January 29, 2005, the balance

outstanding on the bonds was $19.0 million. We begin

repayment of the principal amount of the bonds in June

2006, with a portion maturing each June 1 until the final

portion matures in June 2018. The bonds do not have a

prepayment penalty as long as the interest rate remains

variable. The bonds contain a demand provision and,

therefore, outstanding amounts are classified as current

liabilities. We pay interest monthly based on a variable

interest rate, which was 2.57% at January 29, 2005. The

bonds are secured by a $19.3 million letter of credit

issued by one of our existing lending banks. The letter

MANAGEMENT’S DISCUSSION & ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS