Dollar Tree 2004 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2004 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

DOLLAR TREE STORES, INC. • 2004 ANNUAL REPORT 25

statement is a revision of SFAS No. 123, Accounting for

Stock-Based Compensation, and supersedes Accounting

Principles Board Opinion No. 25, Accounting for Stock

Issued to Employees. SFAS 123R requires all share-based

payments to employees, including grants of employee

stock options, to be recognized in the financial statements

based on their fair values. Under the provisions of this

statement, we must determine the appropriate fair value

model to be used for valuing share-based payments, the

amortization method for compensation cost and the

transition method to be used at the date of adoption. The

transition alternatives include retrospective and prospective

adoption methods. Under the retrospective method, prior

periods may be restated based on the amounts previously

recognized under SFAS No. 123 for purposes of pro

forma disclosures (see Note 1 to the consolidated financial

statements) either for all periods presented or as of the

beginning of the year of adoption.

The prospective method requires that compensation

expense be recognized beginning with the effective date,

based on the requirements of this statement, for all share-

based payments granted after the effective date, and based

on the requirements of SFAS No. 123, for all awards

granted to employees prior to the effective date of this

statement that remain unvested on the effective date.

The provisions of this statement are effective for

fiscal 2006 and we are currently evaluating the

requirements of this revision and have not determined

our method of adoption.

QUANTITATIVE AND QUALITATIVE

DISCLOSURES ABOUT MARKET RISK

We are exposed to various types of market risk in the

normal course of our business, including the impact of

interest rate changes and foreign currency rate

fluctuations. We may enter into interest rate swaps to

manage exposure to interest rate changes, and we may

employ other risk management strategies, including the

use of foreign currency forward contracts. We do not

enter into derivative instruments for any purpose other

than cash flow hedging purposes and we do not hold

derivative instruments for trading purposes.

Interest Rate Risk

We use variable-rate debt to finance certain of our

operations and capital improvements. These obligations

expose us to variability in interest payments due to

changes in interest rates. If interest rates increase, interest

expense increases. Conversely, if interest rates decrease,

interest expense also decreases. We believe it is beneficial

to limit the variability of our interest payments.

To meet this objective, we entered into derivative

instruments in the form of interest rate swaps to manage

fluctuations in cash flows resulting from changes in the

variable-interest rates on the obligations. The interest rate

swaps reduce the interest rate exposure on these variable-

rate obligations. Under the interest rate swap, we pay the

bank at a fixed-rate and receive variable-interest at a rate

approximating the variable-rate on the obligation, thereby

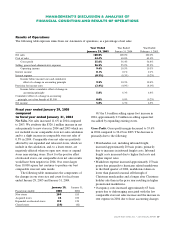

MANAGEMENT’S DISCUSSION & ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

creating the economic equivalent of a fixed-rate obligation. Under the $19.0 million interest rate swap, no payments are

made by parties under the swap for monthly periods in which the variable-interest rate is greater than the predetermined

knock-out rate.

The following table summarizes the financial terms of our interest rate swap agreements and the fair value of each

interest rate swap at January 29, 2005:

Hedging Receive Pay Knock-out Fair

Instrument Variable Fixed Rate Expiration Value

$19.0 million interest rate swap LIBOR 4.88% 7.75% 4/1/09 ($0.9 million)

$25.0 million interest rate swap LIBOR 5.43% N/A 3/12/06 ($0.6 million)

Hypothetically, a 1% change in interest rates results in approximately a $0.4 million change in the amount paid or

received under the terms of the interest rate swap agreements on an annual basis. Due to many factors, management is

not able to predict the changes in fair value of our interest rate swaps. The fair values are the estimated amounts we

would pay or receive to terminate the agreements as of the reporting date. These fair values are obtained from an outside

financial institution.