BP 2009 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2009 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

BP Annual Report and Accounts 2009

Notes on financial statements

24. Financial instruments and financial risk factors continued

148

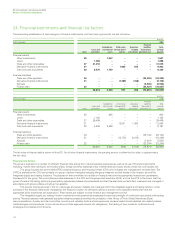

Some mitigation of credit exposure is achieved by: netting arrangements; credit support agreements which require the counterparty to provide

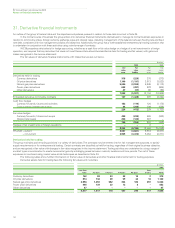

collateral or other credit risk mitigation; and credit insurance and other risk transfer instruments.

For the contracts comprising derivative financial instruments in an asset position at 31 December 2009, it is estimated that over 80% (2008

over 80%) of the unmitigated credit exposure is to counterparties of investment grade credit quality.

Trade and other receivables of the group are analysed in the table below. By comparing the BP credit ratings to the equivalent external credit

ratings, it is estimated that approximately 55-60% (2008 approximately 60-65%) of the unmitigated trade receivables portfolio exposure is of

investment grade credit quality. With respect to the trade and other receivables that are neither impaired nor past due, there are no indications as of

the reporting date that the debtors will not meet their payment obligations.

The group does not typically renegotiate the terms of trade receivables; however, if a renegotiation does take place, the outstanding balance is

included in the analysis based on the original payment terms. There were no significant renegotiated balances outstanding at 31 December 2009 or

31 December 2008.

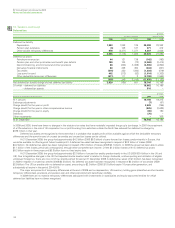

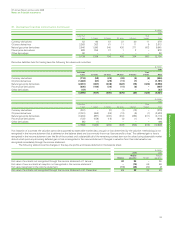

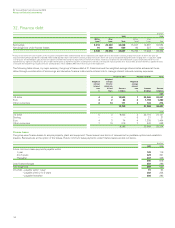

$ million

Trade and other receivables at 31 December 2009 2008

Neither impaired nor past due 29,426 25,838

Impaired (net of valuation allowance) 91 73

Not impaired and past due in the following periods

within 30 days 808 1,323

31 to 60 days 151 489

61 to 90 days 76 596

over 90 days 464 1,170

31,016 29,489

The movement in the valuation allowance for trade receivables is set out below.

$ million

Trade and other receivables at 31 December 2009 2008

At 1 January 391 406

Exchange adjustments 12 (32)

Charge for the year 157 191

Utilization (130) (174)

At 31 December 430 391

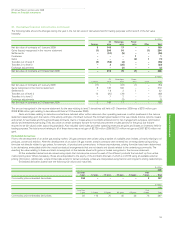

(c) Liquidity risk

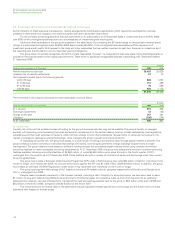

Liquidity risk is the risk that suitable sources of funding for the group’s business activities may not be available. The group’s liquidity is managed

centrally with operating units forecasting their cash and currency requirements to the central treasury function. Unless restricted by local regulations,

subsidiaries pool their cash surpluses to treasury, which will then arrange to fund other subsidiaries’ requirements, or invest any net surplus in the

market or arrange for necessary external borrowings, while managing the group’s overall net currency positions.

In managing its liquidity risk, the group has access to a wide range of funding at competitive rates through capital markets and banks. The

group’s treasury function centrally co-ordinates relationships with banks, borrowing requirements, foreign exchange requirements and cash

management. The group believes it has access to sufficient funding through the commercial paper markets and by using undrawn committed

borrowing facilities to meet foreseeable borrowing requirements. At 31 December 2009, the group had substantial amounts of undrawn borrowing

facilities available, including committed facilities of $4,950 million, of which $4,550 million are in place through to the fourth quarter of 2011,

unchanged from the position as at 31 December 2008. These facilities are with a number of international banks and borrowings under them would

be at pre-agreed rates.

The group has in place a European Debt Issuance Programme (DIP) under which the group may raise $20 billion of debt for maturities of one

month or longer. At 31 December 2009, the amount drawn down against the DIP was $11,403 million (2008 $10,334 million). In addition, the group

has in place an unlimited US Shelf Registration under which it may raise debt with maturities of one month or longer.

The group has long-term debt ratings of Aa1 (stable outlook) and AA (stable outlook), assigned respectively by Moody’s and Standard and

Poor’s, unchanged from 2008.

Despite recent increased uncertainty in the financial markets, including a lack of liquidity for some borrowers, we have been able to issue

$11 billion of long-term debt during 2009 and issue short-term commercial paper at competitive rates, as and when required. As an additional

precautionary measure, we have increased and maintained the cash and cash equivalents held by the group to $8.3 billion at the end of 2009 and

$8.2 billion at the end of 2008, compared with $3.6 billion at the end of 2007.

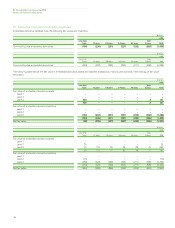

The amounts shown for finance debt in the table below include expected interest payments on borrowings and the future minimum lease

payments with respect to finance leases.