BP 2009 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2009 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

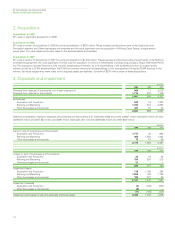

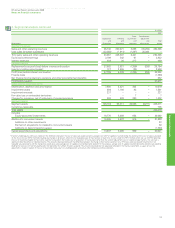

1. Significant accounting policies continued

Impairment of intangible assets and property, plant and equipment

The group assesses assets or groups of assets for impairment whenever

events or changes in circumstances indicate that the carrying value of an

asset may not be recoverable, for example, low prices or margins for an

extended period or, for oil and gas assets, significant downward revisions

of estimated volumes or increases in estimated future development

expenditure. If any such indication of impairment exists, the group makes

an estimate of the asset’s recoverable amount. Individual assets are

grouped for impairment assessment purposes at the lowest level at

which there are identifiable cash flows that are largely independent of the

cash flows of other groups of assets. An asset group’s recoverable

amount is the higher of its fair value less costs to sell and its value in use.

Where the carrying amount of an asset group exceeds its recoverable

amount, the asset group is considered impaired and is written down to

its recoverable amount. In assessing value in use, the estimated future

cash flows are adjusted for the risks specific to the asset group and are

discounted to their present value using a pre-tax discount rate that

reflects current market assessments of the time value of money.

An assessment is made at each reporting date as to whether

there is any indication that previously recognized impairment losses may

no longer exist or may have decreased. If such indication exists, the

recoverable amount is estimated. A previously recognized impairment

loss is reversed only if there has been a change in the estimates used to

determine the asset’s recoverable amount since the last impairment loss

was recognized. If that is the case, the carrying amount of the asset is

increased to its recoverable amount. That increased amount cannot

exceed the carrying amount that would have been determined, net of

depreciation, had no impairment loss been recognized for the asset in

prior years. Such reversal is recognized in profit or loss. After such a

reversal, the depreciation charge is adjusted in future periods to allocate

the asset’s revised carrying amount, less any residual value, on a

systematic basis over its remaining useful life.

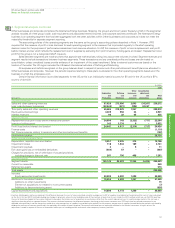

Financial assets

Financial assets are classified as loans and receivables; available-for-sale

financial assets; financial assets at fair value through profit or loss; or as

derivatives designated as hedging instruments in an effective hedge, as

appropriate. Financial assets include cash and cash equivalents, trade

receivables, other receivables, loans, other investments, and derivative

financial instruments. The group determines the classification of its

financial assets at initial recognition. Financial assets are recognized

initially at fair value, normally being the transaction price plus, in the case

of financial assets not at fair value through profit or loss, directly

attributable transaction costs.

The subsequent measurement of financial assets depends on

their classification, as follows:

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or

determinable payments that are not quoted in an active market. Such

assets are carried at amortized cost using the effective interest method if

the time value of money is significant. Gains and losses are recognized in

income when the loans and receivables are derecognized or impaired, as

well as through the amortization process. This category of financial

assets includes trade and other receivables.

Available-for-sale financial assets

Available-for-sale financial assets are those non-derivative financial assets

that are not classified as loans and receivables. After initial recognition,

available-for-sale financial assets are measured at fair value, with gains or

losses recognized within other comprehensive income. Accumulated

changes in fair value are recorded as a separate component of equity

until the investment is derecognized or impaired.

The fair value of quoted investments is determined by reference

to bid prices at the close of business on the balance sheet date. Where

there is no active market, fair value is determined using valuation

techniques. Where fair value cannot be reliably measured, assets are

carried at cost.

Financial assets at fair value through profit or loss

Derivatives, other than those designated as effective hedging

instruments, are classified as held for trading and are included in this

category. These assets are carried on the balance sheet at fair value with

gains or losses recognized in the income statement.

Derivatives designated as hedging instruments in an effective hedge

Such derivatives are carried on the balance sheet at fair value. The

treatment of gains and losses arising from revaluation is described

below in the accounting policy for derivative financial instruments and

hedging activities.

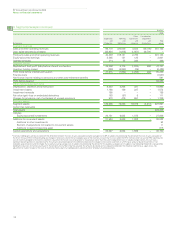

Impairment of financial assets

The group assesses at each balance sheet date whether a financial asset

or group of financial assets is impaired.

Loans and receivables

If there is objective evidence that an impairment loss on loans and

receivables carried at amortized cost has been incurred, the amount of

the loss is measured as the difference between the asset’s carrying

amount and the present value of estimated future cash flows discounted

at the financial asset’s original effective interest rate. The carrying amount

of the asset is reduced, with the amount of the loss recognized in the

income statement.

Available-for-sale financial assets

If an available-for-sale financial asset is impaired, the cumulative loss

previously recognized in equity is transferred to the income statement.

Any subsequent recovery in the fair value of the asset is recognized

within other comprehensive income.

If there is objective evidence that an impairment loss on an

unquoted equity instrument that is carried at cost has been incurred,

the amount of the loss is measured as the difference between the

asset’s carrying amount and the present value of estimated future

cash flows discounted at the current market rate of return for a similar

financial asset.

Inventories

Inventories, other than inventory held for trading purposes, are stated

at the lower of cost and net realizable value. Cost is determined by the

first-in first-out method and comprises direct purchase costs, cost of

production, transportation and manufacturing expenses. Net realizable

value is determined by reference to prices existing at the balance

sheet date.

Inventories held for trading purposes are stated at fair value less

costs to sell and any changes in net realizable value are recognized in the

income statement.

Supplies are valued at cost to the group mainly using the average

method or net realizable value, whichever is the lower.

119

Financial statements

BP Annual Report and Accounts 2009

Notes on financial statements